What Are Stock Appreciation Rights?

A stock appreciation rights (SARs), similar to employee stock options, is a method of giving bonuses to employees in the form of shares instead of cash. Employees benefit from SARs when the share prices increase in the future. Depending on the stock appreciation rights scheme, the employee either gets shares or cash equal to the net amount due to the increase in the share price.

It is important to note that SARs typically have a specific period of validity. The rights are worthless after expiry. Therefore, SARs holders must exercise their rights within the period of validity to gain value out of the employee stock appreciation rights. Moreover, these rights can only be exercised after a certain time frame, known as a vesting period.

- Employee stock appreciation rights are like stock options, a way to give bonuses to staff in the form of shares rather than cash.

- The elements of stock appreciation rights are grant date, exercise price, vesting date, and expiration date.

- Stock appreciation rights follow a process from the top down. The Board of Directors approves the SARs, and after defining the elements of SARs, they pay the participants.

- SARs help incentivize the employees without giving up equity and instigates company loyalty. However, SARs also has some flaws, such as a lack of cash infusion, which requires an approval process.

Stock Appreciation Rights Explained

Stock appreciation rights are a form of reward where the employee (holder) can benefit from the profits arising from the appreciation of the company’s share price. These rights are bestowed upon employees for a certain period after which the SARs expire.

The gains from the appreciation of price can be converted either into cash or by gaining additional shares for the net amount. This factor entirely depends on the plan or scheme the company has designed.

Depending on the employer’s plan, SARs can be a stand-alone plan where they are independent instruments and not in conjunction or a combination of any other stock options. Otherwise, the holder can treat them as tandem stock appreciation rights where non-qualified stock options give the holder the authority to exercise it as an option or a SAR.

It is part of the compensation to the employees as an incentive or bonus based on their performance during the service period, SARs. However, the incentive amount will depend on the exercise of rights by the employees because the incentive amount will be the difference between the market price on the exercise date and the grant date.

In this option, an employee does not have to own the assets, but the company has to arrange funds for financing stock appreciation rights. Moreover, this benefits the employers because they do not have to issue additional shares, which may change the share price.

Elements

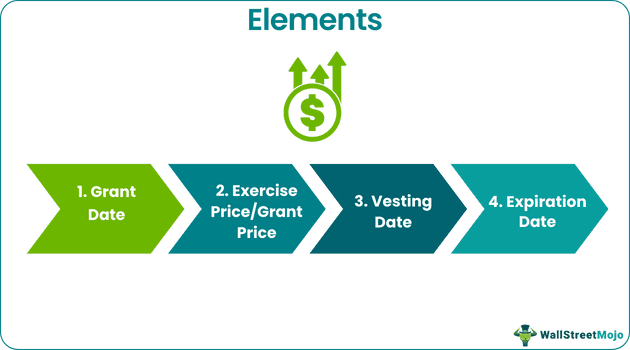

There are some key dates and terms to understand before discussing for SARs. They are as listed below:

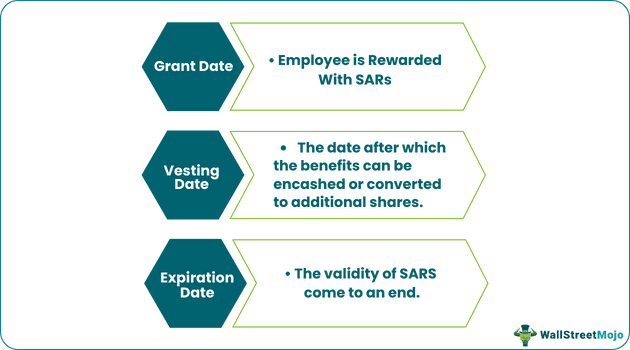

- Grant Date: – The processes of stock appreciation rights start only after this date. On the grant date, employees get their stock appreciation rights.

- Exercise Price/Grant Price: Exercise price is the stock’s market price on the grant date. This price determines the worth of the stock.

- Vesting date: – This is when employees can exercise their stock appreciation right.

- Expiration Date: – This is the last day employees can exercise their stock appreciation right.

Process

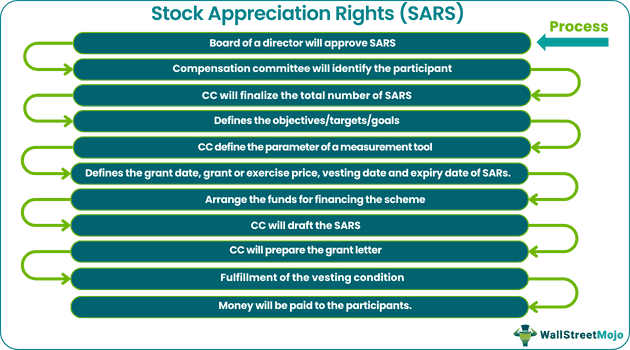

Below is the process of stock appreciation rights (SARs):

- Approving SARs: The board of directors will authorize stock appreciation rights in board meetings and appoint a compensation committee (CC) to decide and oversee the scheme.

- CC will identify the eligible participant: The compensation committee (CC) will identify the participants eligible for this scheme.

- CC will finalize the total number of SARs: CC will finalize the total number of SARs to be offered to these participants and the ratio of rights to be distributed.

- Define Objectives/Targets/Goals: The next step is to define these participants’ objectives, targets, and goals as per their vesting conditions.

- CC defines the parameter of a measurement tool: After defining the goals, the compensation committee will also determine the parameters to evaluate participants’ performance.

- Dates: Next step is to define the grant date, grant or exercise price, vesting date, and expiry date of SARs.

- Arranging the funds: Funds are arranged for the scheme by issuing bonds, debentures, or making other investments. Insufficient funds will lead to the company’s inability to pay for the scheme.

- CC will draft the SAR: The compensation committee will prepare the stock appreciation after defining the above factors. That is, all terms and conditions such as grant date, grant price, vesting period, expiry date, vesting conditions, performance goals, evaluation parameters, or any other conditions related to the scheme.

- CC will prepare the grant Letter: The compensation committee will then prepare the grant letter by which participants will enter into this scheme.

- Wait for the end of the vesting period: All the above things must be done by the compensation committee at the initial stage of the stock appreciation right. After completing all the requirements, participants will wait for the end of the vesting period.

- Evaluating the performance of participants: Once the vesting period ends, the compensation committee will evaluate the participants’ performance and decide whether the participants have fulfilled the vesting conditions.

- Money will be paid to the participants: After fulfilling the vesting conditions, as and when participants exercise the rights during the exercise period defined by CC, they will receive the money.

Calculation Example

Let us understand the concept of SARs better with the help of an example.

ABC Inc. has declared stock appreciation rights to its employees for which conditions are as below:

- Grant Date: January 1, 2015

- Grant Price/Exercise Price: $100

- Number of Shares: 100

- Service Period: 3 years

- Vesting Date: January 1, 2018

- Expiry Date: December 31, 2019

Let us assume one of the employees exercises his right as of January 1, 2018, and the share market price as of that date is $200. This implies that they will earn $10,000 against their SARs.

- (Market Price of share – Exercise Price) * No of Shares

- = ($200 – $100) *100

- = $ 10,000

Employees can earn this amount generated in the form of cash or shares. If the right is settled in the form of shares, the market price will determine the number of shares, which is as follows:

Net Money Value of Shares = $10,000

Market Price of Shares = $200

- Number of shares received = $10,000/ $200

- = 50 shares

Participants can exercise the rights anytime during the vesting period, i.e., between the vesting and expiry date. However, the unexercised rights can be subject to market price fluctuation.

Advantages

Let us briefly discuss the advantages of SARs:

- It is a method to incentivize the employees without giving up equity.

- It acts as a company retention plan so employees can stay in an organization for an extended period.

- It exhibits lesser compliance than employee stock option plans or employee stock purchase plan.

- This scheme exhibits more flexibility compared to other options.

Disadvantages

The disadvantages of SARs are as follows:

- There is no cash infusion when an employee buys this option/stock.

- This option requires approval by the board of directors and shareholders.

- The company requires funds to finance SARs, which are being exercised by the employees, which may lead to the company’s liquidity issues.

Frequently Asked Questions (FAQs)

How do Stock Appreciation Rights (SARs) work?

Employees with stock appreciation rights (SARs) are entitled to cash payments equal to the growth of their shares of company stock that are traded on a public exchange market.

Are stock appreciation rights taxable?

When you receive stock appreciation rights, there are no tax repercussions at the federal level. However, you must record compensation income at the time of exercise based on the fair market value of the vested amount.

When should you exercise stock appreciation rights?

Employees can typically exercise SARs once they have vested or become eligible. However, similar to a vesting schedule for 401(k) plans, this vesting period can differ from company to firm.

What is the biggest drawback of SARs?

The drawback of SARs is that it is a high-risk form of employee compensation. The chances of, SARs expiring worthless are high if the company’s stock does not appreciate.

Recommended Articles

This has been a guide to Stock Appreciation Rights. Here we discuss its elements, processes, example, advantages, and disadvantages. You can learn more about accounting from the following articles –