Tender Windows for Employees: What They Are and How They Work

Table of Contents

Introduction

Let us say that an individual has been vesting their shares for many years. The organization is growing, talk of an initial public offering or IPO is getting louder, and then an email lands: a program called tender window is going to start for employees. What is this program, and how does it actually work for people who have daily responsibilities within the organizations and a life outside the cap table?

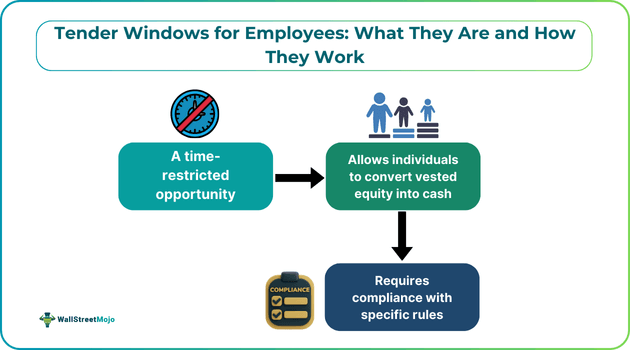

Think of a tender window for employees as a way to offload holdings. In other words, it is a time-bound opportunity to convert a portion of the vested equity into cash while adhering to the rules set by the company. The headline isn’t “free money.” Rather, it is choices: how much to sell, whether to exercise first, and how those choices interact with taxes, lock-ups, and resale rules that will be applicable even after the IPO.

What A Tender Window Is (And Isn’t)

At private companies, a tender window for employees is a company-organized program that allows employees to sell a limited portion of their vested shares or options to approved buyers at a pre-agreed price. Typically, it is tied to a financing round and runs for a short period (often a couple of weeks). The company sets caps (for example, up to 10 to 20% of vested holdings), applies eligibility rules concerning tenure, performance, and good standing, and nets out fees or withholdings before the proceeds are wired. If you want the corporate-finance baseline for comparison with your internal program, check out WallStreetMojo’s overview of a tender offer.

A tender window for employees is not a promise with regard to ongoing liquidity. It is a window, with specific terms and a hard stop. Consider it a discrete decision: review the cap, the price, the fees/withholding, and the timeline, and decide if those specifics can help you fulfill your goals. Before you compare caps and pricing, refresh the bigger decision, i.e., when to act; a plain-English overview of when to exercise your private stock options lays out the timing trade-offs (AMT, holding periods, and tenders) in one place.

How These Programs Usually Run

Here’s the usual flow, minus legalese and acronyms:

- Announcement & Docs. You’ll get a summary email, frequently asked questions or FAQs, and a portal link. Make sure to read the fine print on caps, pricing method (often a discount to a recent preferred round), fees/withholding, eligible instruments (options vs. already-exercised shares), and timelines.

- Eligibility Check. HR or the plan administrator confirms what you can offload. Some programs only allow already-exercised shares; others allow exercise-and-sell in one go.

- Your decision. You choose how much to participate, up to the cap. Note that personal factors are crucial here: Do you want to diversify, cover a big purchase, minimize risk before a lock-up, or simply test the process with a small amount?

- Settlement. After the window closes and buyers are matched, proceeds hit your account. Expect netting of any fees or tax withholding. Keep copies of the confirmations for tax time.

If you’re new to equity compensation and want a quick taxonomy to share with family or a financial planner, Wall Street Mojo’s article on stock options is a friendly, high-level refresher.

Where Taxes, Lock-ups, And Resale Rules Fit

A tender window for employees doesn’t happen in a vacuum. Three guardrails shape the real-world experience:

#1 - ISO/NSO Tax Treatment

In the case of ISOs, exercising doesn’t create regular income tax, but the spread, i.e., fair market value minus strike, can count as an AMT adjustment in the year you exercise. If you sell too soon (prior to meeting holding periods), the sale becomes a disqualifying disposition, and some of your gain may be considered ordinary income. The IRS lays out statutory-option rules and holding periods in Publication 525, and the AMT mechanics in the Form 6251 instructions. For NSOs, ordinary income is typically recognized at exercise on the spread, and your employer may withhold at source.

#2 - Lock-Up Periods Around IPOs.

Even if your company goes public, insiders (including employees) usually cannot offload their holdings immediately. Lock-up agreements commonly restrict sales for about 180 days after the IPO. You might see staggered releases, but the point is the same: manage supply and stabilize trading early on. If you are not sure what a lock-up period means, you may take a look at Wall Street Mojo’s article on ‘lock-up period’.

#3 - Rule 144 And Restricted/Control Securities.

Post-IPO, the holders of restricted or control securities may have to comply with Rule 144 to resell, which includes conditions, such as holding periods (for restricted shares), public information availability, manner of sale, and volume limits for affiliates.

The Practical Point: Tenders can bring forward liquidity before the IPO and reduce exposure through lock-ups at the cost of potential fees, discounts to recent round prices, and a different tax character than a long-term post-IPO sale.

When Participating Can Make Sense (And When To Pass)

Use clear questions instead of a giant spreadsheet to stress-test your choice:

Do you need liquidity without taking on debt?]

If a tender lets you sell a small portion and cover a near-term financial requirement (moving, childcare, a home down payment), that’s a concrete benefit. Just sanity-check the cap, fees, and any employer withholding to ensure that you’re comparing the net proceeds instead of a headline price.

How concentrated is your net worth?

If salary, benefits, and a large portion of your paper wealth are based on a single private company, participating can be a simple diversification move. Taking a measured slice can be helpful in keeping you calm through different scenarios, for example, lock-ups, pricing swings, and quiet periods.

Would exercising ISOs today create AMT strain?

If you’re considering exercise-and-tender, remember the AMT adjustment with regard to ISOs. It’s sensible to talk with a tax professional or take the help of a reputable calculator to project the cash impact, utilizing the IRS references above (Publication 525 for statutory options and the Form 6251 instructions for AMT).

Are the tender terms favorable enough?

Focus on the following four lines in the documents:

- Cap: What percentage of vested holdings can you sell?

Price: Is it a discount to the last preferred round? If yes, then how much?

Fees/Withholding: What’s netted out before the proceeds hit your account? - Settlement Timing: When do you actually receive cash?

Do resale rules change your timeline?

If you skip the tender planning to carry out the sale soon once the IPO is over, check if you’re an affiliate and whether your shares are restricted. These factors determine which Rule 144 conditions apply, including holding periods and volume limits.

A Practical, No-Math Walkthrough You Can Reuse

Here’s a simple framework to carry out the assessment of your next tender window:

- Write Your Goal In One sentence.

Examples: Reduce exposure by selling 10 to 15% and cover taxes along with a year of living expenses - List The Knowns And Unknowns

The knowns include Cap percentage, tender price, fees, and window dates. On the other hand, the unknowns include potential AMT, your affiliate status, and expected lock-up length following IPO. - Map Three Paths.

- Participate up to the cap (sell a small portion now).

Skip and revisit at IPO (accept lock-up and Rule 144 timing). - Exercise-and-hold (only if long-term tax treatment is your priority and you can handle the cash/AMT implications).

- Participate up to the cap (sell a small portion now).

- Pressure-Test With “Life Happens” Scenarios.

Ask a series of questions: What if the IPO slips a year? What if the next 409A revision moves higher or lower? What if you change jobs? You don’t need a Monte Carlo; just sanity-check whether you’d regret passing on today’s certainty.

5. Confirm The Operational Steps.

If you opt in, you must know how to accept the offer in the portal. Confirm bank details and track tax forms. If you pass, set a reminder to review the grant status, lock-up language, and Rule 144 basics ahead of an initial public offering.

Wrap-Up

Employee tender windows aren’t magic, and they’re not a trap. Rather, they’re structured, time-limited chances to turn part of your paper value into actual cash while adhering to the terms the company defines. If you read the documents carefully, check how your options are taxed, and understand the lock-up and resale rules that are still applicable. Doing so, you’ll know whether participating supports your goals. Once you make a decision, document your reasoning and move on with a clear head.