Trade Line Meaning

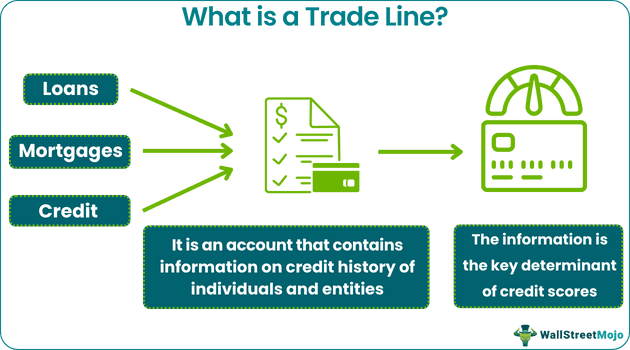

A trade line is information listed in a credit report regarding the activities in an account that can impact one’s credit score. Account balance, payment history, and account status are just a few examples of what a trade line encompasses (e.g., current, past due or charged-off).

A “furnisher” is a company that supplies data about consumers to a consumer reporting agency which they then include in consumer reports. The credit score algorithm calculates a consumer’s three-digit credit score using the information. They need a regular check for errors as un-rectified errors may negatively affect credit scores.

- A trade line is a collection of data on individual credit. Consumer reporting agencies regularly use it to generate credit scores for an individual.

- It contains details such as the partial account number of the individual, credit history, payment history (whether the individual has paid them or yet to pay them), loan sanctioned, the opening and closure of the same, etc.

- Unfavorable remarks or mistakes may have a negative effect on credit scores. This may result in missed chances pertaining to credit, such as denying a loan for the person or them having an undesirable credit utilization rate.

Trade Line Explained

Trade lines contain details of the record of the individual’s credit activities. It is established when a user has had their credit application approved. Lenders require a credit score on an application for credit as part of the approval procedure. It contain data used by credit scoring models, such as those developed by FICO or VantageScore. An individual’s three-digit credit score is created using their trade line by the credit score algorithm.

The five elements that determine the FICO score are:

- Payments made in the past (history).

- The debt that is due.

- Credit history length.

- New credit.

- Credit mix.

They includes the information below:

- Name and address of the lender.

- Type of account.

- Partial Account number.

- Current balances

- Date of opening of account.

- The date of closure of the account (if applicable).

- Date of the most recent credit activity by the individual.

- The minimum monthly payment, interest rate, frequency of payments, last payment date, etc.

- The credit limit or the sanctioned amount, outstanding balance, and past-due amount as applicable.

- Individual’s name either as the account owner or an authorized user.

- History of payments.

- Status of the Account etc

Trade lines come in two forms: revolving and installment. Revolving credit lines include credit cards and home equity lines of credit. A credit limit (or line of credit) is given to the user of this form of account, and they are free to utilize any amount of credit up to the specified limit. Depending on the terms of the arrangement, users may be able to pay off their balance each month or carry the balance and pay interest. Installment trade lines include loans for personal use, student loans, and mortgages. In addition, users can take out lump sum loans with this form of account. Individuals typically make monthly payments with a fixed interest rate for the duration of the loan.

The Hargreaves Lansdown provides access to a range of investment products and services for UK investors.

Removal of Trade lines

A trade line could be deleted from a credit report for various reasons. First, it will be removed from credit reports after approximately two months if the individual is an authorized user and has been terminated from the account. Creation of a fraudulent account can also lead to erasure of the trade line. Upon recognizing the fraud, removing the fraudulent account will boost credit scores. It is important to check for mistakes and rectify them, as mistakes can negatively impact credit scores. Each credit line will have a separate trade line reflected on the credit report. Therefore, negative remarks or errors can adversely impact credit scores. This can lead to missing credit-based opportunities, such as being ineligible for a loan or having an undesirable credit utilization ratio. Hence, regular checks on credit reports are essential.

Examples

Check out these examples to get a better idea:

Example #1

Dave wants to apply for a mortgage. The details in the mortgage trade line that will endure scrutiny include his payment history and if he has taken any previous loans. If he had previously obtained a loan, the details such as the sanctioned amount, the interest rate, and payments made and their duration would also be checked. The loan application will be sanctioned if they are satisfactory and justify his credit score.

Example #2

CPN (Credit Privacy Numbers) trade lines can be beneficial for those looking for positive enhancement of their credit scores. This article describes how it can help one make their credit report look good.

Trade Lines for Business

Business trade lines include the business’s details to pay creditors, suppliers, and service providers. Any company or organization must be an established legal entity to apply for a business trade line. The owner shall keep separate bank accounts and email and mailing addresses. With its aid, a company can build the credibility necessary with banks and other capital lenders. In addition, multiple favorable trade credit lines in a company’s name on a business credit report demonstrate that it has a reliable payment history toward creditors.

Moreover, commercial lenders analyze the trade line history of business credit to decide whether to grant a loan or capital. They also check the interest rates and payback periods of capital along with this information. Businesses with strong trade credit are more eligible for loans with lower interest rates and more favorable payment conditions than those with weak trade credit histories.

Disclosure: This article contains affiliate links. If you sign up through these links, we may earn a small commission at no extra cost to you.

Frequently Asked Questions (FAQs)

1. What are trade lines of credit?

An account present in a credit report is the “trade line.” Each separate account is a different trade line. Lenders and other financial institutions provide credit reporting agencies with trade-line data. The agencies calculate the credit scores for consumers are using the same.

2. What is a trade line on a mortgage?

A mortgage trade line contains details of the account name of the creditor, a partial account number, and the customer’s payment status. For example, it includes details such as whether a customer is making regular, late, or no payments. Additionally, it will display the account’s outstanding debt.

3. How to open trade lines?

It is automatically open when after the initiation of a new line of credit. Instances include signing up for a new credit card, purchasing from that card, and paying debts. A new history is established for every credit history.

4. How long does a trade line last?

It depends on the circumstances. Each reporting agency will choose how long to keep the trade line after the closure of an active account, which is typically ten years. However, trade lines for closed accounts with a poor history are typically taken off the report after seven years.

Recommended Articles

This has been a guide to Trade Line and its Explanation. Here we have explain it in detail, its removal, along with business examples. You may also find some useful articles here: