What Is Accounting Profit?

Accounting profit is the net income available after reducing direct costs and expenses from the total revenue calculated following the generally accepted accounting principles (GAAP).

Explicit cost is identifiable and measurable and includes Material cost, Labor cost, Production & overhead cost, transportation cost, sales and marketing cost, etc. Implicit costs are not considered as the same is not incurred and notional. These are the reported profits of the business (i.e.) as per the financial statements. It is also called book profits.

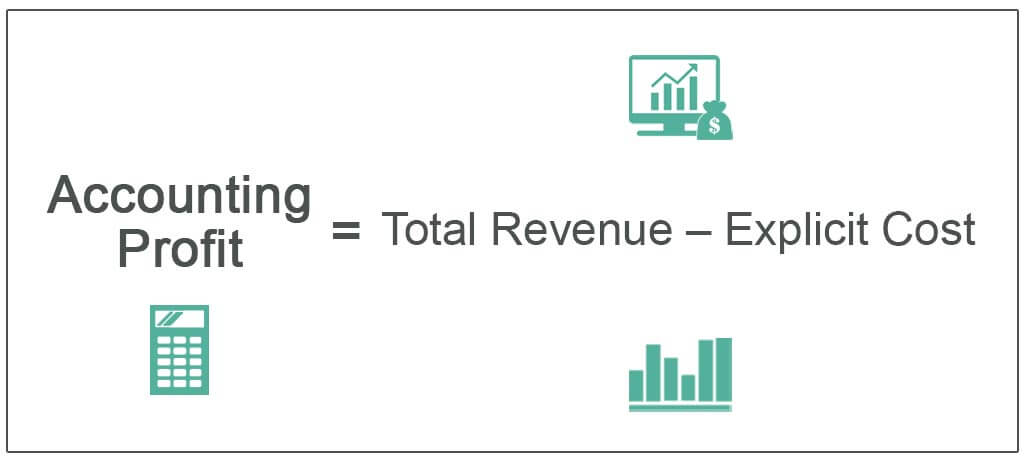

Accounting Profit Formula

Below is the formula-

Accounting Profit = Total Revenue – Explicit Cost

Accounting Profit vs Economic Profit Explained in Video

Example of Accounting Profit

Example #1

OZ Corp manufactures shirts. Its annual turnover is $1,000,000. Its direct Expenses are Raw Materials – $700,000, Labor cost – $100,000, Production Expenses – $50,000 and Depreciation – $50,000.

Accounting Profit Formula = Total Revenue – Explicit Cost

- = $1,000,000 – ($700,000+$100,000+$50,000+$50,000)

- = $1,000,000 – $900,000

- = $100,000

Example #2

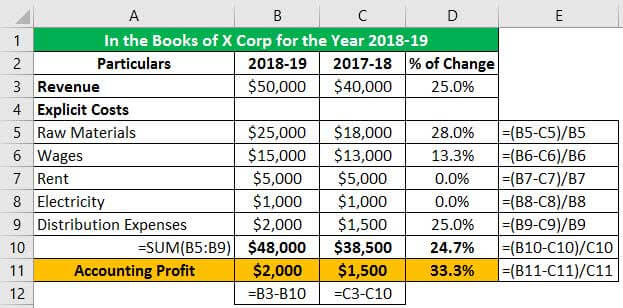

X Corp has prepared its financial statements for the year 2018-19. The details of revenue and profit are given below.

In the above-presented case, the calculated accounting profit for the year has improved in FY 18-19 over FY 17-18 by a $500 (i.e.) 33.3% increase over PY. The revenue has increased by $10,000 (i.e.) 25% over PY. It shows the book profits generated by the business for a particular period. It acts as a check to evaluate the performance and efficiency of the business. Business calls relating to further investment, profitability, market position, etc., can be analyzed with the help of such profits.

Accounting Profit Vs. Cash Profit

Cash profits indicate the profits in terms of real cash inflows and outflows. Accounting profit is the theoretical one, whereas cash profit is the real profit of the business. It is considered to be a better measure of economic viability.

Example

ABC Inc. prepares its financial statements for the year 2018-19, as per the accounting approach and cash flow approach to analyze its performance.

In the cash flow approach, the profit is more as it does not consider non-cash expenditure, and it reflects the real profits of the business.

Advantages

- It has the advantage over cash profits as it can be made favorable for the business as it can be legally manipulated.

- It reflects the financial position and performance of the business.

- It can be used as an indicator to compare across business and industry.

- It helps in decision-making regarding business expansion, investments, performance, etc.

- Investors and other stakeholders will be interested in the business if the business is profitable.

- It is considered an essential element in measuring the repayment capacity of the business.

Disadvantages

- It is a book profit that varies from cash profits (i.e.). It is not the real profit as profit does not indicate the real cash inflow.

- Accounting Profit includes transactions of extraordinary and exceptional items.

- It cannot be used as a proper comparison across the business as various methodologies are used in depreciation & amortization, Impairment, provisions, accruals, and valuation.

- Different laws for taxation in various countries and different ways of presenting the financial statements (i.e.) as per IFRS, US GAAP, etc.;

- It can be easily manipulated as window dressing can be done to present the books of accounts.

- Profit cannot be considered the proper benchmark for comparison as other indicators like Revenue, gross margin, financial ratios, cash flow position, etc., need to be considered.

Limitation

- It measures the performance for a single period, so it is possible to manipulate the results favorable to the business/ management based on the year-end targets, and huge discounts are provided to improve the top line.

- Non-cash expenditure like depreciation, amortization, etc., reduces the accounting profit but does not impact the cash flows.

- ROI (i.e.) opportunity cost of capital employed is not considered in the calculation of accounting profits.

Conclusion

Accounting profit represents the business’s profit, including all the revenue and expenses allowable. This profit can be derived from the financial statements of the business. It is useful for management to assess the performance of the business. It acts as a major indicator to compare business performance across the industry.

Recommended Articles

This article has been a guide to accounting profit and its Definition. Here we discuss the formula to calculate accounting profit, examples, advantages, and disadvantages. You can learn more about accounting from the following articles –