Part of our Financial Statement Analysis guide

Book Profit Meaning

Book profits refer to the profit earned by the business entity from its operations and activities. They are calculated by deducting all the business expenses incurred within a financial year from all the sales revenue and other income generated from selling goods & services within that same financial year.

The profits made on investments that have not been realized yet become book profits. That means when, for example, the current value of securities becomes higher than the actual cost paid, and the securities are yet not sold but still owned by the holder, then such profits are termed as book profits.

Book Profit Explained

Book profit, in short, is the leftover money after the entity pays off all its expenses, as shown in the profit and loss statement. In other words, it refers to money earned by an entity during a financial year by selling products and services deducted from all the expenses incurred during the same financial year. The calculation of book profit is simple and can be expressed as below:

Book Profit = Revenues – Expenses

Book profit is the profit as shown in the profit and loss account of the entity and is considered to be the actual profits because it is considered all cash and non-cash transactions. Like revenue generated through sales made on credit and charging annual depreciation, no actual cash transaction is just book entries.

Cash profit is the surplus that companies generate through actual cash flows. It is calculated by subtracting all the cash outflows (including all paid expenses like salary, rent, bills, etc.) from the cash inflows (including cash sales). Cash profit can also be calculated using book profits by adding back all the non-cash expenses (like depreciation debited in Profit and loss account and subtracting the non-cash revenues (like credit sales).

Cash Profit = Book Profit + Non-Cash Expenses – Non Cash Revenues

Or Book Profit = Cash Profit – Non-Cash Expenses + Non-Cash Revenues

Calculation Examples

Let us consider the following examples to understand what is book profit and how to calculate it:

Example 1

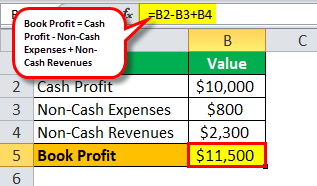

As calculated by Mr. Solo, the owner of a sole proprietorship firm, the Cash Profit amounted to $10,000 in the previous year based on actual recipes and payments. Mr. Solo charges an annual depreciation of $800 on its assets. The credit sales (not included in cash profit) made amounted to $2300. Mr. Solo wants to find Book Profits.

Solution:

= $ (10000 – 800 + 2300) = $11500

Example 2

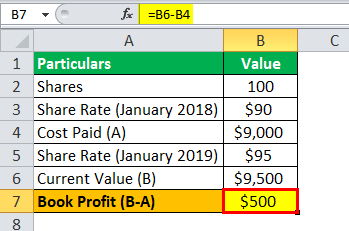

Mr. John bought 100 shares of ABC Ltd at $90 per share a year ago in January 2018. The stock during January 2019 is trading for $95. John, a long-term investor, is expecting the stock prices to rise further in the future and, hence, decided to remain invested.

Solution:

Hence John did not sell the stocks and calculate the profits earned during the one-year interval as follows:-

Cost Paid = 100 shares * $90 per share = $9000

Current Value = 100 shares * $95 per share = $9500

Book Profit (B – A) = $(9500 – 9000) = $500

There is a possibility that this profit might erase if the prices go down. E.g., during 2019, due to poor economic growth and high market volatility, the prices decreased to $88 per share, thus erasing all the profits and creating a loss of $2 per share.

Note: Generally, such profits on financial instruments are not taxed until they are actually sold, and profit or loss is realized.

Book Profit Vs Net Profit

Book profit and net profit sound similar, but they differ widely in terms of their application and impact on a business. The table below shows the differences between the two:

| Category | Book Profit | Net Profit |

|---|---|---|

| Meaning | It is the profit earned by a company before the salary or earning of partners is debited. | It is the revenue recorded after the expenses are deducted and liabilities are subtracted from the total profit earned. |

| Tax Implications | It is not calculated before the tax liabilities are considered. | It is the figure obtained after the tax liabilities are deducted. |

| Origin | It is computed per the Income Tax Act. | It is computed per the Books of Accounts maintained by a company. |

| Uses | It is mostly used for tax purposes. | It is mostly used to determine financial ratios. |

| Track | Not a concern for analysts or stakeholders | Tracked by analysts or stakeholders for making investment decisions. |

Special Cases

In various countries, business entities’ calculation of book value is for taxation purposes. Accordingly, companies treat book value as taxable income, and a specific rate applies to the book value to calculate the amount of taxes payable.

We are discussing the two major scenarios where the use of such profits is for taxation purposes:-

#1 – MAT for Companies in India

MAT or Minimum Alternative Tax applied to companies that pay dividends to their shareholders but do not pay taxes under normal Income tax provisions due to various exemptions and deductions allowed.

We calculate MAT using book profits. Here, it arrives after useful additions or deductions made to net profit, as shown in the profit and loss statement. The MAT book profit calculation uses the formula below:

Book Profit = (Net Profit + Additions) – Deductions

#2 – Partnership Firm

In this case, it simply signifies the computation of the profits before the partner’s remuneration. In other words, companies calculate it by adding back the salary and commissions paid to the partners (if debited in the P&L account) into the net profit as per the profit and loss account.

Book Profit = Net Profit + Partner’s Remuneration

Recommended Articles

This has been a guide to Book Profit & its Meaning. Here we explain the concept with a few calculation examples, vs net profit and some special cases. You may learn more about accounting from the following articles –