What is Break-Even Point In Accounting?

Break-Even Point in Accounting refers to the point or activity level at which the volume of sales or revenue exactly equals total expenses. In other words, the breakeven point is the level of activity at which there is neither a profit nor loss and the total cost and revenue of the business are equal.

It is that level of business activity where the sales are just enough to meet the total cost, which includes both Fixed and Variable Costs. Also, the Breakeven point acts as an essential level for a business to attain before making a profit. The accounting break-even point can be computed in different ways.

- Breakeven point refers to the stage or level of activity at which the sales or revenue precisely matches total expenses.

- It is the point in a company’s operations where sales are barely enough to cover all fixed and variable costs.

- Additionally, before a business can profit, it must reach the breakeven point. There are various methods for calculating the accounting breakeven point.

- To calculate this method of accounting, the company needs to know the fixed costs, variable costs, and selling price per unit.

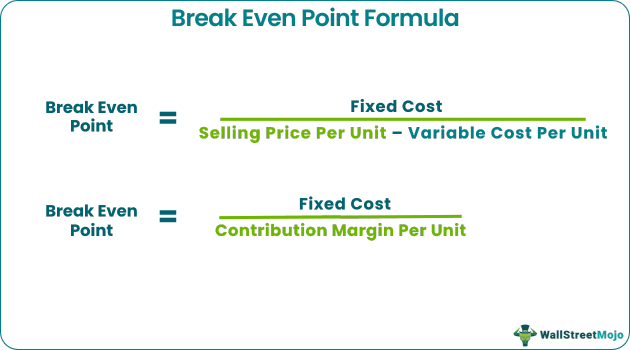

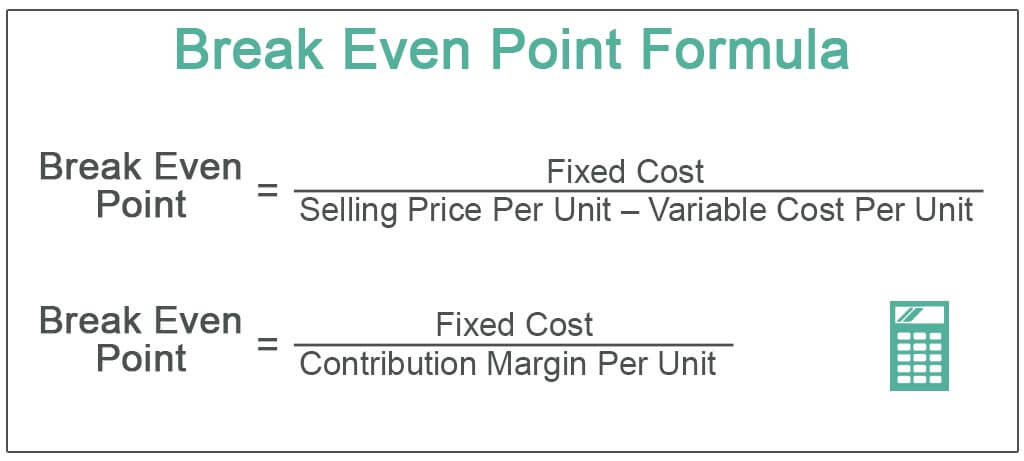

Formula

Another formula to calculate Break-Even Point in Accounting

Break Even Point Explained in Video

Importance of Break-Even Point in Accounting

- To understand the importance behind the Break-Even Point in Accounting, it is of paramount importance to understand the classification of Costs. Accounting automation software makes it easier to monitor these costs continuously. Cost is classified as either Fixed Cost or Variable Cost.

- Fixed cost is independent of the level of sales and is of a fixed nature. Some of the popular examples include Rent, Insurance, etc.

- Variable Cost is directly linked to the level of sales. Examples include commissions etc.

Segregation of cost into “Variable Cost” and “Fixed Cost” and their relationship with Sales and Profit is vital in undertaking the Break-even point Analysis. First, by segregating the cost into Fixed and Variable, a business can ascertain the sunk cost in nature (Fixed Cost) and not be directly impacted by sales. Secondly, once a business can verify the proportion of Variable Costs to its Sales, it can implement strategies that can result in Cost Efficiency, resulting in better cost management and more profits.

Breakeven Point Analysis helps businesses understand its Cost Structure vis a vis their Sales Revenue and how the same gets affected as Revenue changes. It helps them determine the breakeven point for different sales volumes and cost structures. With this information, the management can better understand the overall performance and decide what units it should sell to break even or reach a certain profit level.

Calculation Example

Let’s understand the Break-Even Analysis in Accounting with the help of an example:

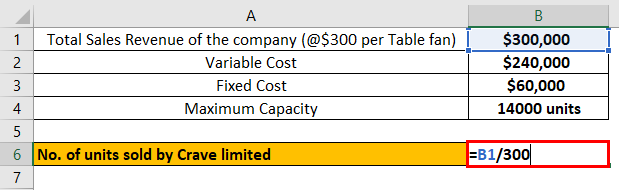

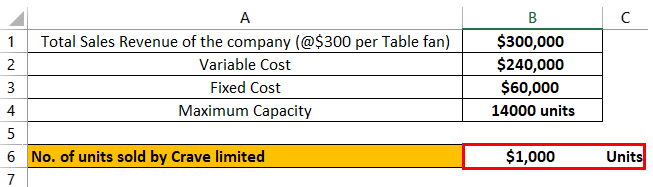

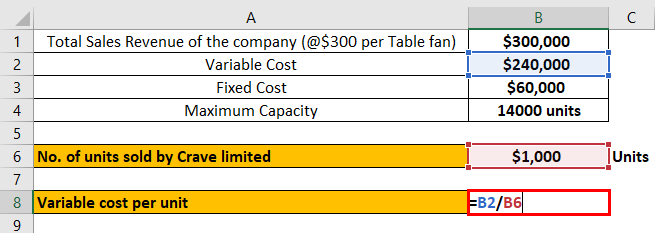

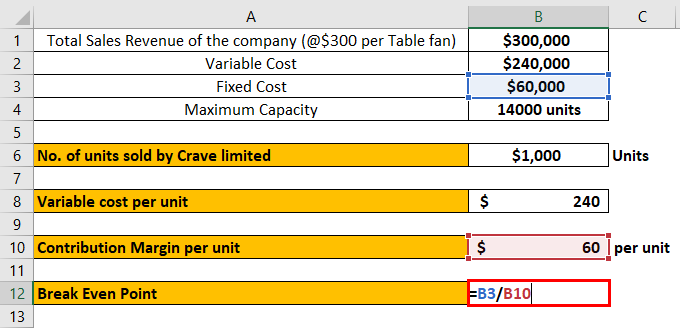

Crave Limited has recently entered into the business of making Table fans. The company’s management is interested in knowing the breakeven point at which there will be no profit/loss. Below are the details about the cost incurred:

| Total Sales Revenue of the Company (@ $300 per table fan) | $300,000 |

| Variable Cost | $240,000 |

| Fixed Cost | $60,000 |

| Maximum Capacity | $14000 units |

So, first will find out the No. of units sold by Crave limited:

No. of units sold by Crave limited will be:

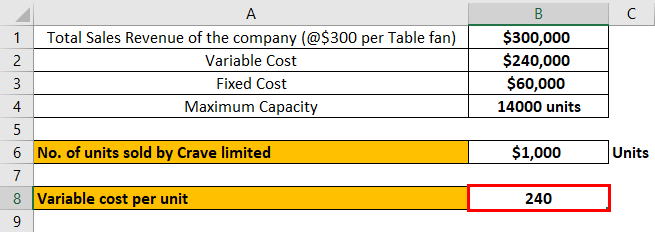

Now, we need to Calculate Variable Cost per Unit

Variable cost per unit will be:

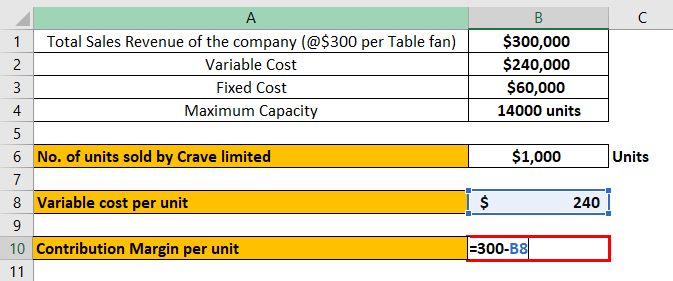

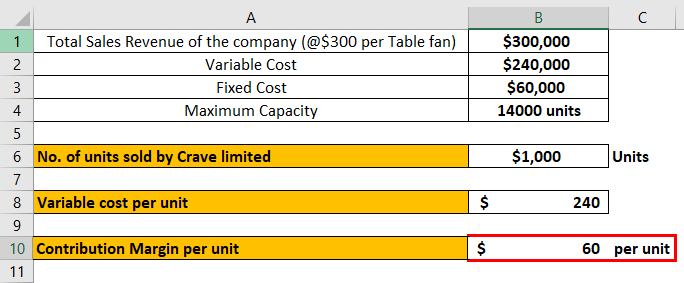

We need to find the Contribution per unit, i.e., = Selling price per unit- variable cost per unit.

Contribution Margin per unit will be:

Now, at last, we will find the Break-Even Point by using its formula = (Fixed Cost/Contribution Margin per unit)

The Break-Even Point formula will be:

Thus Crave limited need to sell 1000 units of electric Table fans to break even at the current cost structure. At this break-even point of 1000 units, Crave Limited will succeed in meeting both its Fixed and Variable expenses of the business. Below the breakeven point of 1000 units, Crave Limited will make losses on a net basis if the same cost structure exists.

Here it is essential to understand that the Fixed Cost (in this case $60000) is constant and doesn’t vary with the level of Sales Revenue generated by Crave Limited. Thus once Crave Limited succeeds in making Break-Even Point, all Sales over and above that level will lead to profits as the excess of sales over Variable Cost will be a positive value since Fixed Cost has already been fully absorbed by Crave Limited on attaining the Breakeven Sales Level.

Advantages

- One of the most critical and primary benefits of Break-Even Point in accounting is its simplicity of calculation and helping the business determine the number of units to be sold to breakeven, i.e., no profit, no loss.

- It helps understand the cost structure, i.e., the proportion of Fixed Costs and Variable Costs. Since Fixed Cost doesn’t change easily, it helps business owners to take measures to control the Variable cost without focusing on the total cost.

- It is vital in forecasting, long-term planning, growth, and business stability.

Disadvantages

- The biggest shortcoming of the Break-Even Point in accounting analysis is the assumption, which holds that fixed cost remains constant and Variable cost varies proportionately with the level of sales, which may not be the case in the real-world scenario.

- It assumes costs are either fixed or variable; however, some expenses are semi-fixed in reality. Example Telephone expenses comprise a fixed monthly charge and a variable charge based on the number of calls made.

Conclusion

It is difficult for any business to decide its expected sales volume level accurately. Such decisions are usually based on past estimates and market research regarding the demand for products offered by the business. On the other hand, Business Cost, especially the Fixed Cost of a business, is fixed in nature, which can’t be recovered by the business and is sunk in nature. BEP Formula in accounting helps bridge this gap by enabling businesses to determine how much quantity they need to sell to break even, i.e., no profit, no loss. It is an important management accounting concept that is continuously used by businesses in not only determining the Breakeven Sales level but also in optimize its cost. Once a business can know its breakeven point, it can either reduce the amount of its fixed cost or increase its contribution margin, which may be achieved by selling a more significant proportion of high contribution margin products.

Frequently Asked Questions (FAQs)

What two sorts of breakeven points are there?

There are two approaches to determining a firm’s breakeven point (B.E.P.). It can be calculated in terms of physical units, such as output volume, or estimated in times of monetary value, such as sales value.

Can the breakeven point be negative?

No, it cannot be negative; therefore, if the breakeven point is negative, the company generates revenue without incurring any costs, which is impossible.

When does the breakeven point decrease?

The breakeven point can decrease when there is a decrease in fixed costs, variable costs per unit, or an increase in the selling price per unit. Therefore, reducing costs or increasing prices can also affect demand and sales volume; hence it is essential to consider the impact of these changes on the total profitability of the business.

Recommended Articles

This has been a guide to what Break-Even Point in Accounting is. Here we discuss the formula to calculate the breakeven point in accounting, including the advantages & disadvantages. Here are the other articles in accounting that you may like –