What Is Bond Refunding?

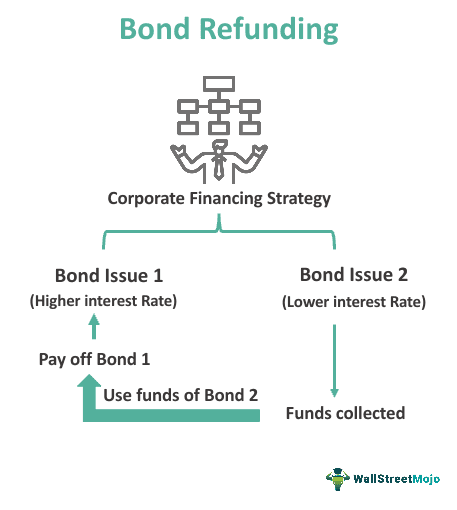

Bond refunding can be defined as a corporate financial planning activity undertaken to lower financing costs by retiring or repaying old outstanding bonds issued previously with high-interest rates with the help of proceeds collected from new debts, usually with lower interest rates.

Market interest rates keep changing, and to avail the benefit of lower interest cost funds, corporates usually undertake this task. Usually, already issued bonds are repaid or retired at maturity or even before maturity (if allowed as per bond agreement) with the proceeds of newly issued bonds with a lower interest rate.

Key Takeaways

- Bond refunding is a strategic corporate financial approach aimed at curbing financing expenses. This strategy involves retiring or redeeming existing high-interest-rate bonds that were issued earlier.

- By harnessing funds generated from new loans, typically featuring lower interest rates, businesses seek to optimize their financial position.

- Bond refunding entails proactively issuing new bonds to replace previously issued ones. This maneuver allows organizations to enhance their financial standing by transitioning to bonds with more favorable terms.

- This strategic substitution of bonds, known as bond refunding, empowers businesses to optimize their debt structure.

Bond Refunding Explained

Bond Refunding can be defined as a capital restructuring activity undertaken by any corporation to lower its borrowing cost.

Bond refunding is a corporate action whereby funds procured from investors are repaid to them with the help of newly issued bonds, i.e., the company repays old bondholders with the money received from new bondholders. It is regulated by the agreement of the bond, which may restrict the holder from repaying the bond until a certain period or date. It is a practice to attract initial investors who wish to lock their funds for a certain period at a desired rate of return.

A bond may be sold before maturity to lower the cost of finance. It may also be refunded due to the increase in the bond issuer’s credit rating, which will help the bond issuer procure funds at lower interest rates. Bonds may also be refunded to lower the restrictions applicable to them. Sometimes refunding bonds offset refunding fees and other transaction charges instead of continuing to repay interest.

Bond Refunding Process

Interest rates vary during a given time frame depending upon certain factors like inflation, opportunity cost, etc. Suppose the interest rate on a bond decreases from the interest rate at which the bonds are purchased. In that case, the bond owner may pay off the bond before its maturity and refinance it at the lower interest rate prevailing in the market. Funds obtained from the reissue of the bonds at a lower rate are used to settle dues from the old bondholders.

Refunding is not so easy. It occurs only with callable bonds. Callable bonds have the clause to get redeemed before their maturity period. Under these bonds, holders have to face the risk of bonds being called up by the owner before the maturity period due to a decline in interest rates.

When Does It Occur?

This process is frequently practiced in the market where the interest rate has fallen as the existing debt is likely to be paid with the cheaper debts from the current market. This was a common practice by bond issuers.

Therefore, a clause known as the call protection clause was inserted in the bond agreement to protect the bondholders from premature redemption. This call protection clause indicates the lock-in period of the bond, which has fixed time limits before which the bond cannot be called up. Suppose the interest rate falls too low during the lock-in period, which calls for redemption of bonds at such time. In that case, the owners can issue new bonds in the interim period. The sale proceeds of interim bonds will be used to buy treasury securities, which need to be deposited in the escrow account.

Interest earned on the escrow account will help to pay-out interest on already issued high-interest rates bonds. When the lock-in period expires, these treasuries are sold, and the deposited funds in the escrow account are utilized to pay bond liabilities. Money is repaid to all bondholders as per their entitlement.

Example

Let us understand the concept with the help of an example.

Walmart Inc. issued $200 million in bonds on 15/06/2018 with an interest cost of 10%. Still, with market conditions and increased credit rating, Walmart is getting lower rate debts, so it decided to call back previous bonds costing 10% and replace them with new $200 million bonds with 5% interest cost.

Accordingly, Walmart Inc., on 01/12/2019, issued new bonds and, at the same time, called back old bonds with a 10% cost. The funds coming from new bonds were utilized towards the payment of old bonds and thus causing a saving of $10 million(5% of $200M).

Advantages

Just as every financial process has its own advantages and disadvantages, so does this process. Let us try to identify the advantages first.

- It helps the issuer to obtain, replace, and utilize lower-cost funds in place of pre-existing high-interest bonds already issued.

- It helps the company in capital restructuring and maintaining an adequate debt-equity ratio;

- Regular repayment of a bond on time will lead to an increase in the credit rating of the company, which in turn will attract more investors and thereby funds;

- This may be helpful to avail of certain income tax benefits as provided by income tax governing agencies.

Disadvantages

Given below are some disadvantages that are equally important for understanding purpose.

- As this activity is undertaken to reduce finance costs, bondholders may feel discomfort in exercising this option as the interest rate payable on already issued bonds was higher than on bonds currently available in the market.

- Undertaking bond refunding involves transaction costs also. Various legal and commercial compliances need to be fulfilled by companies that need to be completed before undertaking bond refunding. Also, there are certain other transaction costs like brokerage, taxes, commission, etc.

- Frequent bond refunding by any corporation may lead to an adverse impact on the image of the company as the investor will form an opinion about a company that funds will not be kept invested for their desired period and may be refunded earlier, which may cause difficulty in fund procurement.

Therefore it is always necessary to identify both the benefits and limitations of any financial process in order to use it in the organization and achieve best results through informed decisions.

Bond Refunding Vs Bond Refinancing

Both the above concepts refer to the process of replacing the existing bonds with new ones. However, let us identify the points of differences between them.

- Bond refunding is the process of reissuing new bonds in place of existing bonds, while bond refinancing is a different concept. Unlike bond refunding, it does not refund the money to the investor.

- Bond refinancing is the restructuring of bonds instead of the repayment of money to the investors. It is very helpful for a business to reduce funding costs as, under it, the organization can take advantage of the new interest scheme and, at the same time, keep old bodies intact. Refinancing is risky for the bond owner as the returns are not as attractive as the complete repayment of funds in case of bond refunding.

- The former takes advantage of the low interest rates and good condition of the financial market but the latter takes advantage of good financial condition of the issuer.

- The former helps the issuer to control and save cost whereas the latter helps in debt restructuring along with cost control.

- The former leads to new or fresh issue of bonds unlike the latter where there is not fresh issue.

Thus, the above are some of the significant differences between the two financial concepts.

Frequently Asked Questions (FAQs)

What is the difference between calling a bond and bond refunding?

Bond calling refers to an issuer redeeming a bond before its maturity date. This often happens when interest rates have dropped, allowing the issuer to replace the higher-interest bonds with lower-cost financing. On the other hand, bond refunding involves issuing new bonds to replace existing ones, usually to lower interest costs. While both aim to reduce borrowing costs, bond calling ends the bond’s life early, while refunding extends it with new bonds.

What are the different types of bond refunding?

There are two main types of bond refunding: current refunding and advance refunding. Current refunding occurs when the issuer replaces old bonds with new ones without a time gap. Advance refunding involves issuing new bonds well before the old ones mature, holding the proceeds in escrow until the call date. This allows issuers to take advantage of favorable market conditions when they arise.

What are the risks associated with bond refunding?

Bond refunding poses risks due to market uncertainties. Interest rates may not be as favorable as expected, potentially leading to higher borrowing costs for the new bonds. Credit rating changes or unfavorable market conditions could also limit an issuer’s ability to refinance, impacting their financial flexibility. It’s essential for issuers to carefully assess market conditions and potential risks before pursuing bond refunding.

Recommended Articles

This has been a guide to what is Bond Refunding. We explain it with example, its process, when does it occur & its differences with bond refinancing. You can learn more about it from the following articles –