What Is FIFO Inventory Method?

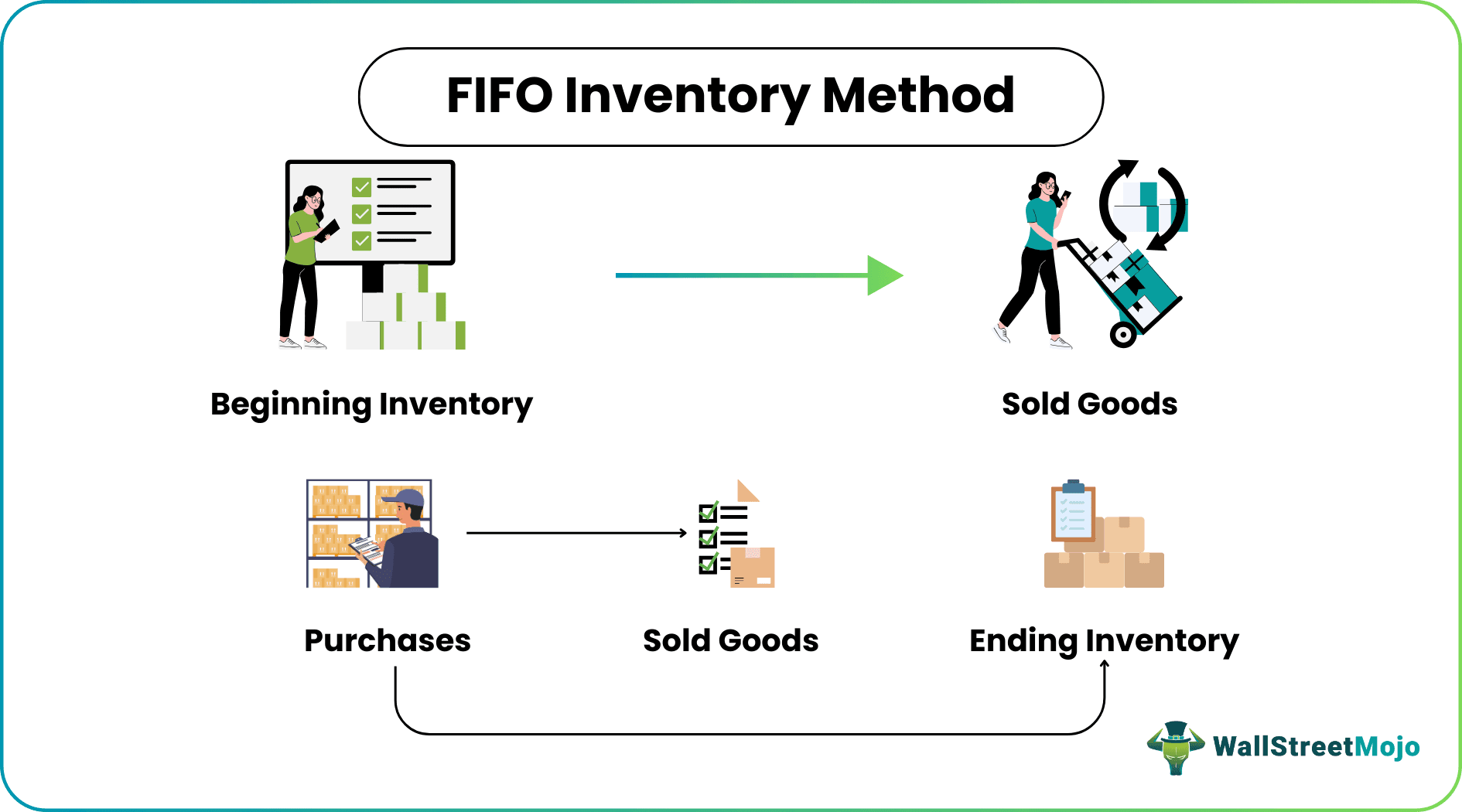

The FIFO accounting method stands for First In First Out. It is one of the most common methods to value inventory at the end of any accounting period; thus, it impacts the cost of goods sold during the particular period.

Inventory costs are reported either on the balance sheet or are transferred to the income statement as an expense to match against sales revenue. When inventories are used up in production or are sold, their cost is transferred from the balance sheet to the income statement as the cost of goods sold.

FIFO Inventory Method Explained

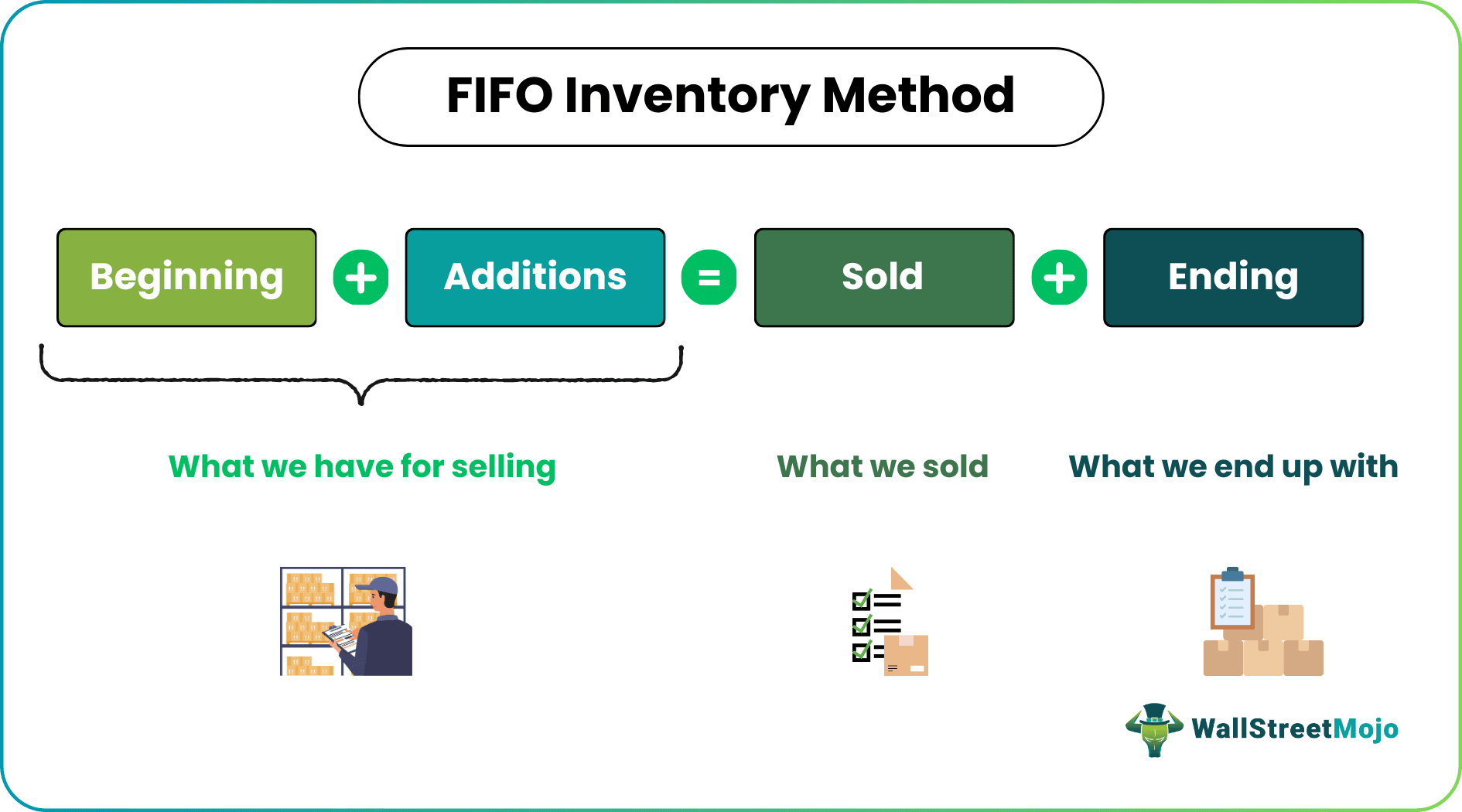

Under the FIFO inventory method formula, the goods purchased at the earliest are the first to be removed from the inventory account. This results in remaining in the inventory at books being valued at the most recent price for which the last inventory stock is purchased. This results in inventory assets recorded at the most recent posts on the balance sheet.

Conversely, this method also results in older historical purchase prices allocated to the cost of goods sold (COGS) and matched against current period revenues.

The FIFO method of inventory valuation results in an overstatement of gross margin in an inflationary environment and therefore does not necessarily reflect a proper matching of revenues and costs. For example, in an environment where inflation is on an upward trend, current revenue will be matched against older and lower-cost inventory items, resulting in the highest possible gross margin.

The FIFO method inventory valuation is commonly used under both International Financial Reporting Standards (IFRS) and Generally Accepted Accounting Principles (GAAP).

Reason

A business in the trading of perishable items generally sells the items purchased first. The benefits of FIFO inventory method typically give the most accurate calculation of the inventory and sales profit. Other examples include retail businesses that sell foods or other products with an expiration date.

However, there are times when even other businesses that don’t fit this description of perishable items use the First In, First Out method for the following reason: Profit and loss statement would reflect a higher gross profit and shows a stronger financial position that is higher net profit to the investors. From the balance sheet point of view the inventory is also valued at a cost at the current price. This would result in a strong balance sheet as inventory would potentially carry a higher value under the FIFO method inventory valuation (assuming an inflationary environment).

Examples

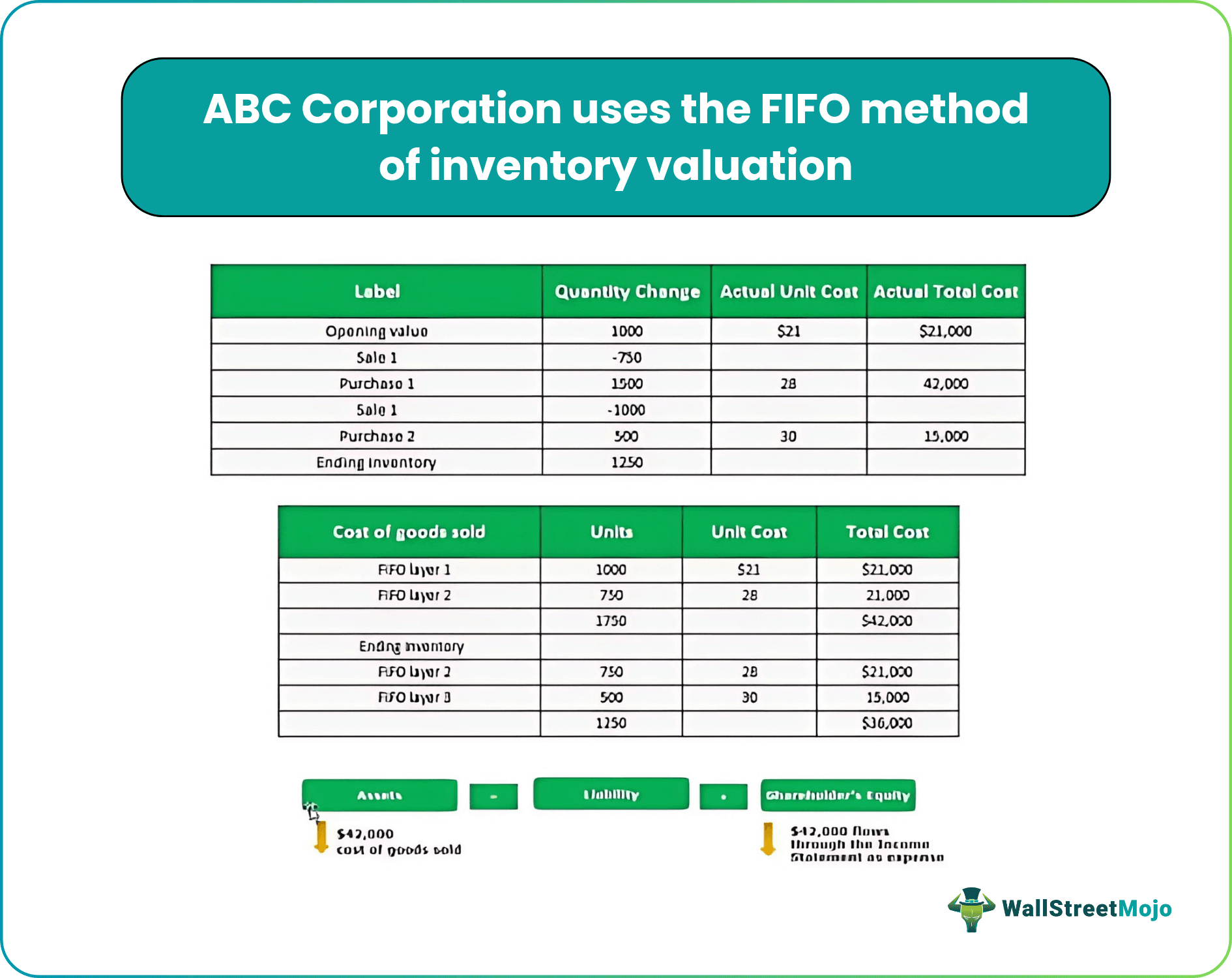

Let us look at an example of FIFO inventory method below.

ABC Corporation uses the FIFO method of inventory valuation for December. During that month, it records the following transactions:

Unit of Goods sold: 1000 Beginning inventory + 2000 Purchased – 1250 Ending inventory = 1750 Units. Calculation of First In First Out method

The controller uses the information in the above table and the FIFO inventory method formula to calculate the cost of goods sold for December and the inventory balance as of the end of December.

The $42,000 cost of goods sold and $36,000 ending inventory equals the $78,000 combined total of beginning inventory and purchases during the month.

Thus, the above example of FIFO inventory method gives a clear idea about the valuation process.

Advantages

- The FIFO method of accounting saves time and money spent calculating the exact inventory cost of being sold because the inventory recording is done in the same order as purchased or produced.

- Easy to understand is one of the benefits of FIFO inventory method

- . Ending inventory is valued based on the most recent purchase price; therefore, inventory value better reflects current market prices of similar products.

- As the oldest available units are used for the cost of goods sold calculation, the possible risk of reduced net realizable value (NRV) and resulting loss recognition is negated as an entity is not dragging any old inventory units in records.

- As the closing stock value is critical in current asset calculation and related accounting ratios (for example, liquidity ratios), the FIFO inventory valuation method is much more relevant to value-ending inventory.

- Normally in an inflationary environment, prices are constantly rising, which will cause an increase in operating expenses. Still, with FIFO accounting, the same inflation will cause an increase in ending inventory value that will help increase gross profit and ultimately cover other inflated operating expenses.

Disadvantages

source: bp.com

- One of the biggest disadvantages of FIFO accounting method is inventory valuation during inflation; the First In, First Out method will result in higher profits and thus will result in higher “Tax Liabilities” in that particular period. This may result in increased tax charges and higher tax-related cash outflows.

- The use of the perpetual FIFO inventory method is not a suitable measure of inventory in times of “hyperinflation.” During such times, there is no particular pattern of inflation, which may result in the prices of goods inflating drastically. Thus, in such periods, matching most prior purchases with the most recent sales would not be appropriate and present a distorted picture as the profit may be pumped up.

- The FIFO inventory valuation method would not be price patterns. This may result in misstated profits for the same period.

- Although the perpetual FIFO inventory method is easy to understand, it may get cumbersome and clumsy to extract and operate the costs of goods, as a substantial amount of data is required, resulting in clerical errors.

FIFO Inventory Method Vs LIFO Inventory Method

Under the FIFO inventory method, whatever comes in first is sold out first whereas under the LIFO inventory method what is purchased last is sold out first. However, the differences between them as given below:

| FIFO Inventory Method | LIFO Inventory Method |

|---|---|

| The items bought first are sold first. | The items bought last are sold first. |

| Good practice and suitable in any industry. | Not useful in all industries since old stock remains idle. |

| Provides accurate and updated inventory value. | Does not provide accurate and updated inventory value. |

| Under an inflationary economy, the cost of goods sold(COGS) will show a lower value. | Under an inflationary economy, the cost of goods sold(COGS) will show a higher value. |

| Due to lower COGS, profit will be high. | Due to higher COGS, profit will be low. |

Recommended Articles

This has been a guide to what is FIFO Inventory Method. We explain it with examples, advantages, disadvantages, and reasons for using it. Here we also look at the advantages and disadvantages of using FIFO accounting on inventory valuations. You may also have a look at these articles below to learn more on accounting –