What is the LIFO Inventory Method in Accounting?

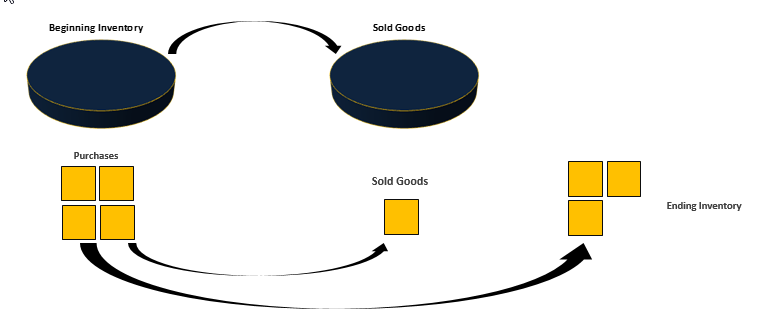

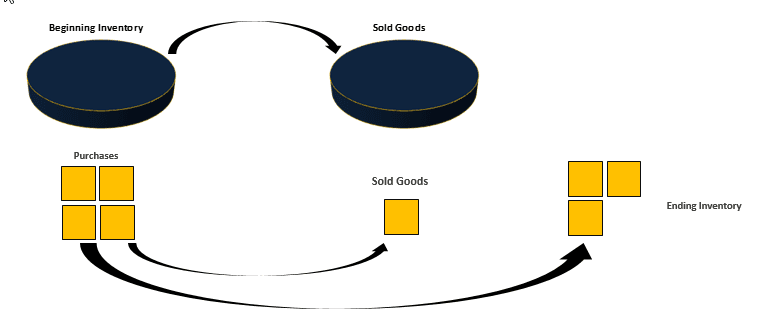

LIFO (Last In First Out Method) is one of the accounting methods of inventory value on the balance sheet. Other methods are FIFO inventory (First In First Out) and Average Cost Method.

LIFO Accounting means Inventory, which was acquired last, would be used up or sold first. It implies that the cost of goods sold would include the cost of inventory acquired recently. And the cost of Inventory remaining, as reported in the balance sheet, would be the cost of the oldest inventory remaining.

Inventory forms a part of Current Assets in the balance sheet. It can be taken as collateral for loan/ working capital purposes. Hence it is necessary to measure the value of Inventory on the balance sheet. The amount of Inventory purchased determines the cost of goods sold (COGS), determining the profitability and tax liability.

Due to the above two main reasons, it is necessary to have a method to arrive at the value of Inventory. It is where LIFO accounting, FIFO, and Average Cost Method come into the picture. Companies have to disclose which method they are adopting for Inventory Valuation in their financial statement.

LIFO Method Example

In this LIFO method example, consider the case of M/s ABC Bricks Ltd, a distributor of cement bricks. The company receives orders from customers every week. It receives brick stock from the manufacturer daily; however, the prices keep changing daily.

The details of stock purchases are as follows:

M/s ABC Bricks Ltd

| Day | No of Bricks | Cost Price | Cumulative Stock Value |

|---|---|---|---|

| 1 | 20 | ₹ 25 | ₹ 500 |

| 2 | 30 | ₹ 27 | ₹ 1310 |

| 3 | 50 | ₹ 29 | ₹ 2760 |

| 4 | 40 | ₹ 31 | ₹ 4000 |

| 5 | 60 | ₹ 33 | ₹ 5980 |

| 6 | 30 | ₹ 35 | ₹ 7030 |

On day 1 of the week, the company purchased 20 bricks for Rs. 25 per piece. This price increased to Rs. 35 per piece by the end of the week due to strong demand in the market.

On the 6th day, the company also receives an order of 50 bricks at a selling price of Rs 36 per piece. Assuming the company is following the LIFO method of inventory accounting, the purchase value of these 50 bricks being sold can be calculated as follows:

LIFO Accounting – Profit & Loss Calculations

Rs. 1710/- would be reported as COGS in the Profit & Loss statement. In this transaction, there would be a profit of Rs 90/- (50 bricks x Rs 36 – Rs 1710/-) in this transaction, and tax liability on profit would be Rs 27/- considering the flat tax rate of 30%.

LIFO Accounting – Balance Sheet Calculations

The remaining Inventory reported on the balance sheet would be at its actual original purchase cost. Thus the inventory value can be calculated as follows:

Impact Due to LIFO Method Example

- Due to the LIFO Inventory method, COGS came out to be Rs 1710/-, resulting in only Rs 90/- as profit. Since we considered purchase cost as that of the last inventory purchased, our COGS remained higher, ensuring lower profit and thereby lower tax outgo. Thus, LIFO Accounting (Last In First Out method) results in lower tax outgo in inflationary conditions.

- Since profit is on the lower side, the earning per share would be lower. Thus, LIFO Accounting (Last In First Out Method) results in lower EPS in inflationary conditions.

- The remaining inventory value is Rs. 5320/-, which is lower since it is valued at the purchase price of that particular batch of bricks. Due to the LIFO method of Inventory, the value of the remaining Inventory is considered lower than the present market value/ replacement value of that Inventory. Thus in inflationary conditions, the LIFO method results in a lower stock valuation on the Balance sheet than the extent replacement value.

What is the Case in Deflationary Market Conditions?

Viz: in the deflationary market scenario, LIFO Accounting (Last In First Out Method) results in the reverse of the above.

- Higher tax outgo as COGS is reported lower and profits are higher.

- Due to higher reported profits, EPS would be higher.

- The Inventory would be valued more than the current market value/ replacement value resulting in inflating the balance sheet.

LIFO Method Advantages and Disadvantages

- In an inflationary market, LIFO methods result in higher COGS as Inventory is valued at recent prices. It results in lower net worth and lower EPS for shareholders. It results in lower net income and lower tax liability for the company. However, due to lower net worth, the company’s reserves & surplus remain lower than what they would have been if LIFO (Last In First Out method) was not used.

- In the deflationary market, LIFO (Last In First Out Method) results in lower COGS as Inventory is valued at recent prices. It results in higher net income and higher tax liability for the company. However, due to higher net income, the company’s reserves & surplus remain higher than what they would have been if LIFO (Last In First Out Method) was not used. It results in higher net worth and higher EPS for the shareholder.

Thus, the LIFO method of Inventory has both its benefits and drawbacks. Management has to weigh both and decide whether to use the LIFO method for Inventory valuation or not as per business needs.

Global Treatment of LIFO Method of Inventory

- IFRS, followed in most countries, does not allow LIFO accounting.

- US GAAP allows the LIFO method of Inventory.

- In India, as per Revised AS 2, the LIFO Inventory method is not permitted, and companies would have to account for Inventory based on either FIFO or weighted average cost method.

Significance for Investors

Investors should scrutinize accounting policies disclosed by the company and trends in the change in accounting policies before making any decisions. Use of LIFO Accounting (Last In First Out Method) or FIFO or Average cost method has wide implications on the P&L and Balance sheet, as shown above.

Recommended Articles

For more on Inventory, explore these related articles from our Inventory guide.