Part of our Profitability Ratios guide

What Is Diluted EPS?

Diluted Earning Per Share (Diluted EPS) is a financial ratio to check the quality of the Earnings per Share after considering potentially dilutive securities that may increase the number of outstanding shares in the future. Calculating diluted EPS is useful when the company has a complex capital structure and contains convertible securities like Preference Shares, Stock Option, Warrants, Convertible Debentures, etc.

It helps in calculating and measuring the company’s profitability based on each share because it considers the possible dilution of the existing shares. Thus, it accounts for the result or the impact of the dilution on the capital structure of the company.

- Diluted EPS is a financial ratio assessing Earnings Per Share quality in complex capital structures with convertible securities like preference shares, stock options, warrants, and debentures.

- It determines the firm’s profitability by accounting for the existing shares’ dilution, affecting the capital structure, and computing profitability based on each claim.

- Using this strategy, investors can evaluate businesses’ performance by comparing like-minded companies across industries. It makes it easier to make informed and crucial decisions. Depending on their income potential assessment, potential for future growth, and share pricing, investors can decide about investment in a company.

Diluted EPS Explained

Diluted EPS is a financial metric that helps in calculation of the earnings that are available to each of the common stocks of an organization after taking into account all the potentially dilutive securities like convertible bonds, stock options, stock warrants that have been converted into common shares. Thus, it evaluates the profit level of the company.

In the diluted EPS calculation process, the items that are deducted are preferred stock dividend because the holders of preference shares have a priority over the common shareholders while dividend is distributed. The weighted average of the number of shares that are diluted, takes into consideration the potential dilution of the stock options and other convertible securities.

For the above purpose, we need to consider the impact of the dilution process. As we study the topic further, it will be clear that the value of diluted EPS is lower than the basic EPS, because the basic EPS only accounts for the outstanding common shares. The objective of including the potentially dilutive securities in the calculation is to find the effect of conversion of securities in future in the earninf per share of the company.

Adjusted diluted EPS is a very commonly used metric for calculation of earnings of the organization and also its performance on a per-share basis. It gives an insight into the effect of the process not only on the company operations but also on the shareholders.

Diluted EPS Explanation in Video

Formula

Given below is the formula used for the calculation. Let us understand the same in details.

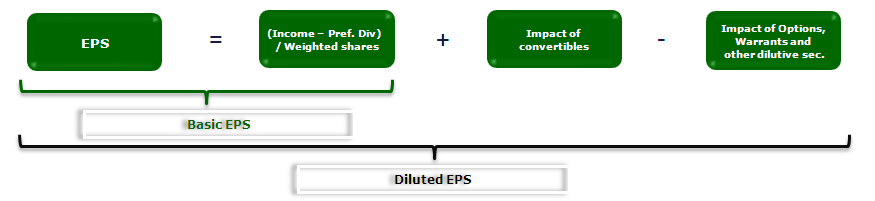

Diluted EPS Formula = (Net Income – Preferred Stock Dividends) / (Weighted Average Number of Shares Outstanding + the Conversion of Any in The Money Options, Warrants and Other Dilutive Securities)

From the above-diluted earnings per share formula, you can understand you need to look at the entire balance sheet and the income statement Diluted EPS Calculation.

How To Calculate?

Next, we see the different steps that help in the calculation. The steps are as follows:

To find adjusted diluted EPS, start from basic EPS and remove the adverse effect of all dilutive securities outstanding during the period.

The Diluted EPS Formula is as per below =

The adverse effects of dilutive securities are removed by adjusting the numerator and the denominator of the basic EPS formula.

- Identify all potentially dilutive securities: convertible bond, options, convertible preferred stock, stock warrants, etc.

- Calculate the basic EPS. The effect of potentially dilutive securities is not included in the calculation.

- Determine the effect of each potentially dilutive security on EPS to see whether it is dilutive or antidilutive. How? Calculate the adjusted EPS assuming the conversion occurs. If adjusted EPS (>) basic EPS, the security is dilutive (anti-dilutive).

- Exclude all anti-dilutive securities from the calculation of diluted earnings per share.

- Use basic and dilutive securities to calculate normalized diluted EPS.

Examples

Let’s take an example for Diluted EPS Calculation.

Example #1

Good Inc. has the following information in the year-end 2017 –

- Net Income: $450,000

- Common Shares Outstanding: 50,000

- Preferred Stock Dividend: $50,000

- Unexercised Employee Stock Options: 5000

- Convertible Preferred Stocks: 23,000

- Convertible Debt: 10,000

- Warrants: 2000

Calculate the Diluted Earnings Per Share.

All information is given in the example above. We will put it in the diluted earnings per share formula.

- First, we will find out the earnings per share.

- Basic Earnings per share = Net Income / Common Shares Outstanding = $450,000 / 50,000 = $9 per share.

Diluted Earnings per Share Formula = (Net Income – Preferred Stock Dividends) / (Common Shares Outstanding + Unexercised Employee Stock Options + Convertible Preferred Stocks + Convertible Debt + Warrants)

- Or, Diluted EPS Formula = ($450,000 – $50,000) / (50,000 + 5000 + 23,000 + 10,000 + 2000)

- Or, DPS = $400,000 / 90,000 = $4.44 per share.

Example #2

We note the following in Colgate’s Earnings Per Share schedule.

source – Colgate 10K filings

- Basic EPS Calculation Methodology – Basic earnings per common share are calculated by dividing net income available for common stockholders by the weighted-average number of shares of common stock outstanding for the period.

- Diluted Earnings Per Share Calculation Methodology – The normalized diluted EPS are calculated using the treasury stock method based on the weighted-average number of shares of common stock plus the dilutive effect of potential common shares outstanding during the period.

- Dilutive potential common shares include outstanding stock options and restricted stock units.

- Anti-dilutive securities – As of December 31, 2013, 2012, and 2011, the average number of anti-dilutive stock options not included in diluted earnings per share calculations was 1,785,032 3,504,608, and 3,063,536, respectively.

- Stock Split Adjustment – As a result of the 2013 Stock Split, all historical per share data and numbers of shares outstanding were retroactively adjusted.

How Useful Is Diluted EPS To The Investors?

The diluted EPS equation is a very useful metric for every investor because it gives additional knowledge about the potential earnings of the company and how the investors are impacted because of it.

- Diluted Earnings Per Share isn’t very popular among investors because it is based on a “what if” analysis. But it’s quite popular among financial analysts that want to ascertain an organization’s earnings per share in its truest sense.

- The basic assumption behind calculating diluted EPS is this – what if the firm’s other convertible securities get converted into equity shares.

- If the firm’s capital structure is complex and consists of stock options, warrants, debt, etc., and outstanding equity shares, diluted earnings per share must be calculated.

- Financial analysts and potential investors who are very conservative in judging the company’s earnings per share assume that all the convertible securities, like stock options, warrants, debt, etc., can be converted into equity shares. Then the basic EPS would be reduced.

- Though this idea that all the convertible securities will convert into equity shares is just a fictitious one, still calculating diluted earnings per share helps a potential investor look through all the aspects of the company’s capital structure.

- It also allows the investors and shareholders to assess the risk involved in the dilution process and evaluate how the returns and future earnings on the stocks and financial securities can be impacted.

- It is a very good method of comparison between peer companies. The investors can compare companies of similar profile across sectors or industries and evaluate their performance.

- It helps in informed investment decisions, which is very crucial for every investor. On the basis of their assessment of a company’s earning potential, future growth opportunity and share valuation the investors can decide whether to invest in the company or not.

Diluted EPS Vs Basic EPS

The concepts given above are two different methods of calculating the earning per share of the business. Let us try to find the differences between them.

- The diluted EPS equation takes into account all the potentially dilutive securities of the business, but the latter takes onto account only the outstanding common shares of the company.

- The former is calculated by dividing the net income after deducting the preferred stock dividend by the weighted average of diluted shares and the latter is calculated by dividing the numerator of the former by the weighted average of common shares.

- The former is a more conservative measure of the profitability of the company than the latter. The latter is a more straightforward measure.

- The former takes into account the potential dilution of securities and its impact on shareholders, but the latter does not do so.

- The value of diluted EPS is lower than the basic EPS.

Thus, the above are some important differences of the two processes.

Frequently Asked Questions (FAQs)

When should both basic and diluted EPS be disclosed?

For each class of equity shares with a separate right to partake in the net profit for the period, an organization shall show basic and diluted earnings per share on the face of the statement of profit and loss.

Is diluted EPS a GAAP measure?

Free cash flow, diluted EPS excluding certain factors, and total segment operating income aren’t performance indicators that conform to generally accepted accounting principles (GAAP) or that are computed per those guidelines.

Is diluted EPS better?

Undiluted EPS is not as precise as diluted EPS. Since diluted EPS considers the effects of all potential stock diluters, it is more advantageous for fundamental research. It ensures that the EPS of the organization is consistent with projected growth. Therefore, it is more critical for the P/E calculation.

What does a higher Diluted EPS indicate?

A higher Diluted EPS generally suggests that the company is generating strong earnings and that the potential dilution from convertible securities is not significantly impacting the revenues available to common shareholders. It can be seen as a positive sign for investors.

Recommended Articles

This has been a guide to Diluted Earnings Per share and its meaning. Here we discuss how to calculate diluted EPS along with examples. You may also have a look at the following articles to learn more about advanced shares –