Part of our Profitability Ratios guide

What are Anti Dilutive Securities

Anti-Dilutive Securities can be defined as those financial instruments that the company has at a particular point in time that is not in common stock form. Still, if they are converted into the common stock, then that would increase the earnings per share of the company.

Let’s take an example to illustrate how the anti-dilutive securities work and how to treat the anti-dilutive securities while calculating the diluted EPS.

Example

Company R has issued a convertible bond of 250 at $200 par for a total of $50,000 with a yield of 15%. Company R has mentioned that each bond can be converted into 20 shares of common stock. The weighted average outstanding number of common shares is 16000. The net income of Company R for the year is $20,000, and the paid preferred dividends are $4000. The tax rate is 25%.

Find out the basic EPS and the diluted EPS. And compare the two.

In the above example, first, we will calculate the earnings per share for Company R.

- Earnings per Share (EPS) = Net Income – Preferred Dividends / Weighted Average Number of Common Shares.

- Or, Basic EPS = $20,000 – $4000 / 16000 = $16,000 / 16,000 = $1 per share.

To compute the diluted EPS, we need to calculate two things.

- First, we will calculate the number of common shares converted from convertible bonds. In this situation, 40 common shares would be issued for each convertible bond. If we convert all convertible bonds into common shares, we will get = (250 * 20) = 5,000 shares.

- Second, we need to find out the earnings from the convertible bonds as well. Here’s the earnings = 250 * $200 * 0.15 * (1 – 0.25) = $5625.

Now, we will calculate the diluted EPS of Company R.

Diluted EPS = Net Income – Preferred Dividends + Earnings from the Convertible Bonds / Weighted Average Number of Common Shares + Converted Common Shares from Convertible Bonds.

- Diluted EPS = $20,000 – $4,000 + $5625 / 16,000 + 5000

- Diluted EPS = $21,625 / 21,000 = $1.03 per share.

If by any chance, the fully diluted EPS is more than the basic EPS, then the security is anti-dilutive securities.

- In the above example, we saw that the convertible bonds are anti-dilutive securities because the basic EPS (i.e., $1 per share) is less than the dilutive EPS ($1.03 per share) when we take the convertible bonds into account.

When a company has anti-dilutive security like the above example, it excludes the anti-dilutive securities from the diluted earnings per share.

Video Explanation of Anti Dilutive Securities

How to check if Convertible Debt is an Anti Dilutive Security?

Before calculating diluted EPS, one needs to check if this security is anti-dilutive. To check whether the convertible debt is anti-dilutive, calculate

- If this ratio is less than basic EPS, convertible debt is dilutive security and should be included in the calculation of diluted EPS.

- If this ratio exceeds the basic EPS, then the convertible debt is anti-dilutive security.

How to check if Convertible Preferred stock is an Anti Dilutive Security?

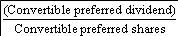

To check whether the convertible preferred stock is anti-dilutive, calculate

- If this ratio is less than basic EPS, a convertible preferred stock is dilutive and should be included in the calculation of diluted EPS.

- If this ratio exceeds the basic EPS, then the convertible preferred stock is anti-dilutive security.

Recommended Articles

This has been a guide to what anti-dilutive securities are. Here we discuss how convertible debt and preferred stock can become anti-dilutive security with examples. You may also learn more about Corporate Finance from the following recommended articles –