Definition of Economics

Economics refers to choices or decisions made by individuals, businesses, and governments regarding the production, distribution, and consumption of goods and services. It also studies their resource allocation for the same during scarcity. In short, it is a branch of social science dealing with the interaction of people with value.

Scarcity implies the limited availability of resources, such as land, capital, machinery, and labor. Economics examines effective resource utilization for the production of commodities. Also, it investigates the role of government incentives and policies in increasing production and trade efficiency. Based on how people, entities, and nations interact to find ways to meet increasing demands with scarce resources, it could be micro and macroeconomics.

- Economics is the field of social science that deals with the study of the scarcity of resources. It analyzes factors affecting the production, distribution, and consumption of goods and services in an economy.

- It examines the allocation of scarce resources by individuals, businesses, and governments. Besides, it investigates the reasons behind poverty, unemployment, and slow economic growth.

- Understanding market changes and the behavior and performance of an economy can help in resource allocation.

- Micro and macroeconomics are two types of Economics. They differ from each other based on decisions made by individuals, entities, and nations to meet increasing demands with limited resources.

Economics Explained

Economics focuses on studying causes of scarcity, ensuring acquisition, allocation, and utilization of scarce resources, and determining how to maximize production efficiency. The rest of the process analyzes proper distribution to and consumption of finished goods by the people.

A country’s economic activity revolves around the production, trade, and consumption of products and services. Labor, land, machinery, and capital are crucial for production. They all work together to enhance productivity. Furthermore, the efficient use of resources and raw materials results in a higher standard of living. Scarcity occurs when demand for products and services exceeds available resources, making it difficult for everyone to meet the needs of the people.

A functioning market involves the decision-making by buyers and sellers, including individuals, families, entities, and societies, to keep moving. These decisions depend on market changes, behavior and performance of an economy, and policies made by the hierarchical authorities. Several factors, including laws, policies, culture, history, and geography, govern an economy.

Types Of Economics

Microeconomics and macroeconomics are the two categories of economics based on scarce resource allocation. While the former focuses on individual and corporate choices, the latter is more concerned with how an entire economy interacts, trades, and makes decisions.

#1 – Microeconomics

It studies the behavior of individual consumers and decision-making by producers in times of scarcity. Other essential functions of it include:

- Examining market structures and how entities interact to create economics systems

- Analyzing the impact of supply or demand in economics on production and price

- Understanding ways to reduce costs and increase profits

- Studying the distribution of scarce resources by individuals and businesses

- Explaining interaction of the people with value

Factors

It considers the following factors to understand the behavior and decisions of individuals and firms:

- The elasticity of Demand: It refers to the demand and response of consumers to price.

- Law of Supply and Demand: The higher the price, the lower the demand and increased supply. The lower the price, the higher the demand and decreased supply.

- Utility: The ways goods or services are beneficial to consumers.

- Fixed Costs and Variable Cost: These associate with the production of goods and services. Variable cost varies with the volume of production, while fixed cost does not change.

- Marginal Cost: It is the additional cost to increase the production of goods and services.

- Opportunity Cost: It incurs upon deciding to allocate a scarce resource and signifies the value or benefit missed when choosing one option over another.

- Market Failure and Externalities: It happens when businesses do not assign prices effectively to consumers. It may lead to negative and positive externalities.

- Market Structures: It comprises perfect competition, monopoly, duopoly, monopolistic competition, oligopoly, monopsony, and oligopsony. These terms explain the competitiveness of the market.

#2 – Macroeconomics

It studies the behavior, performance, and decisions of an economy on the domestic and global levels. Other essential functions of it include:

- Collecting economic data to structure the economy

- Analyzing effects of monetary and fiscal policies

- Understanding the role of labor, capital, and technology in the economic growth

- Examining the economy and how it interacts with markets

Factors

It considers the following factors to understand how an economy measures its domestic production concerning scarcity:

- Business Cycle: It indicates the upward and downward trend of economic growth. It is also the transition of the economy towards the decline and recession. The government manages business cycles by raising or lowering taxes and adjusting interest rates.

- Foreign Direct Investment (FDI): It is the process of international businesses investing money in foreign countries. It can be of horizontal, vertical, and conglomerate types.

- Gross Domestic Product (GDP): It is the measurement to capture and represent the economic output. It refers to the value of goods and services produced by the country in a particular period.

- Inflation: It refers to the price rise of products and services in a period, leading to an increase in the cost of living. It is measured by using the Consumer Price Index (CPI).

- International Trade: It includes tariffs, regulations, and other protection policies that affect trade among nations.

- Money Supply: The value placed on goods or services is money, a medium of exchange. An increase in money supply can lead to inflation, while a decrease can lead to deflation.

- Scarcity: It indicates the limited availability of resources.

- Unemployment Rate: Unemployment results in zero economic output, which leads to low quality of living and standards.

Apart from the main categories, other sub-branches of economics are:

- Neo-classical

- Development

- Environmental

- Behavioral

- Econometrics

- Labor

Ecoomics Example

Let us look at the real-life economics examples to understand the concept:

Example #1

Lucy has a limited amount of money in her bank account. She prioritizes and plans what she needs to buy with the available funds. Lucy starts purchasing less expensive utilities instead of purchasing goods of a luxurious brand. It implies that she makes decisions based on the availability of money in her bank account, which is a scarce resource and adjusts her lifestyle accordingly.

Example #2

Consider a situation where the cost of gasoline is $3 per liter. People can buy 50 liters per week on average at this price. They can buy 60 liters every week if the price drops to $2.5 per liter. If the price is cut more, perhaps to $1.50 per liter, they can buy 100 liters.

Hence, as the price of gasoline decreases, the demand increases. Also, when the price is higher, the requirement declines. It shows an inverse relationship between the price and quantity.

Why Is Economics Important?

Economics studies the scarcity of resources to understand how individuals, businesses, and governments can quantify their allocation to optimize the production, distribution, and consumption of products and services. Besides, it serves many other functions:

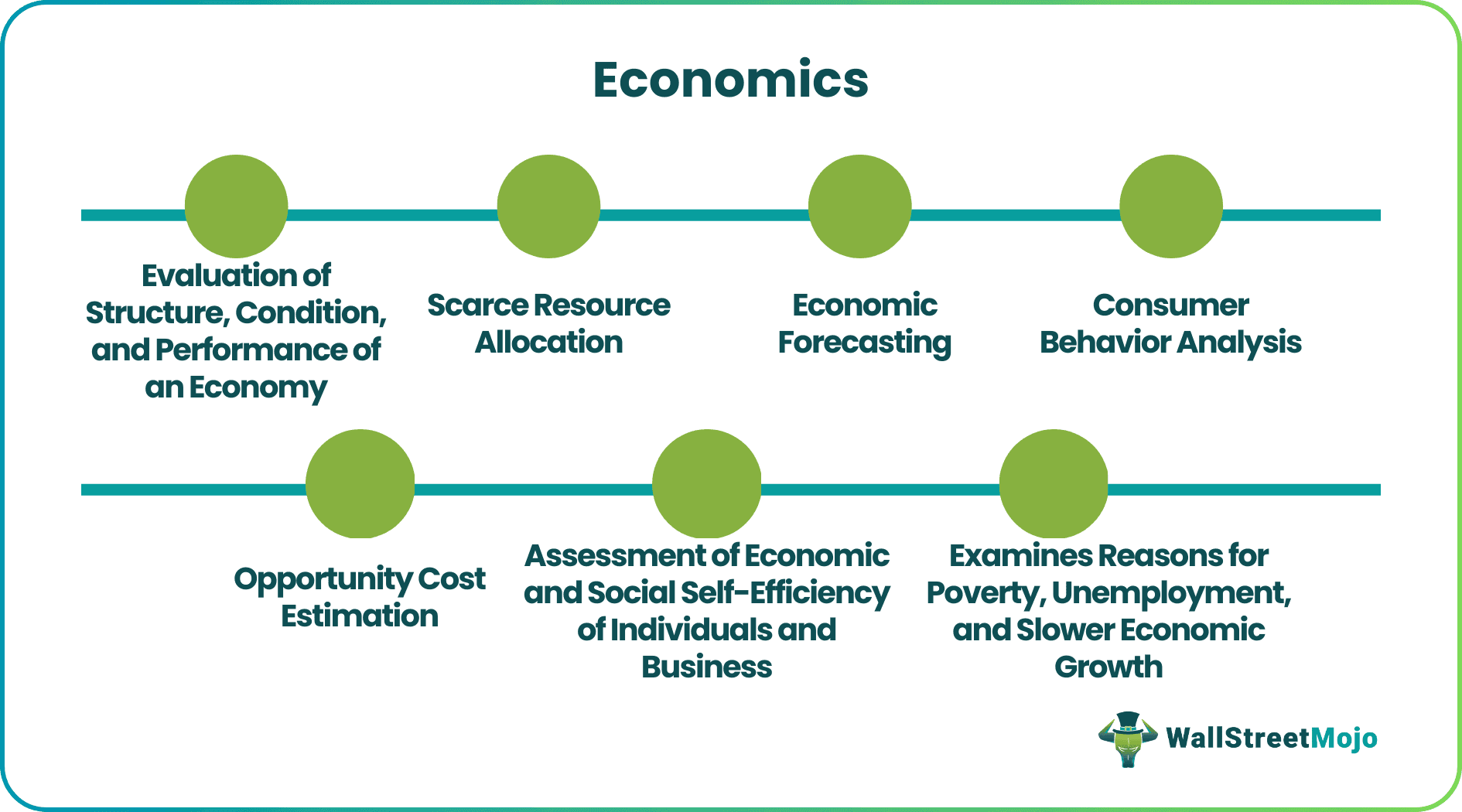

- Deals with strategies for allocating scarce resources

- Analyzes changes in the structure, behavior, and performance of an economy

- Evaluates the state of the economy statistically, thereby explaining its significance

- Studies public policies and examines their impact on the economy

- Deals with the distribution of the income in the society

- Understands the extent of the government intervention in the economy

- Provides an idea of the opportunity cost

- Assesses the economic self-efficacy to improve financial decisions and behavior of individuals and businesses

- Investigates reasons for poverty, unemployment, and slower economic growth

- Performs the economic forecast based on the current situation and helps the government make important decisions

- Provides ideas to deal with the financial crisis

- Leaves room for applying economic forces on the routine social issues

Frequently Asked Questions (FAQs)

What is economics?

Economics is the study of scarce resource allocation by individuals, businesses, and governments during times of scarcity. It also examines their decisions or choices affecting the production, distribution, consumption of goods and services.

Why is economics important?

It serves many crucial functions for an economy, such as studying the scarcity, finding ways to optimize production, distribution, and consumption of commodities, analyzing the behavior and performance of an economy, investigating reasons for poverty, unemployment, and slower economic growth, assessing the financial decisions and behavior of individuals and businesses, etc.

What are the two major types of economics?

Micro and macroeconomics are two categories of economics. While the former focuses on individual and corporate choices in times of scarcity, the latter is more concerned with how an entire economy interacts, trades, and makes decisions on the national and international levels.

Recommended Articles

This has been a guide to Economics and its Definition. Here we discuss how does economics work along with types, examples, and factors. You may learn more from the following articles –