Part of our Economic Concepts guide

Economic Assumptions Definition

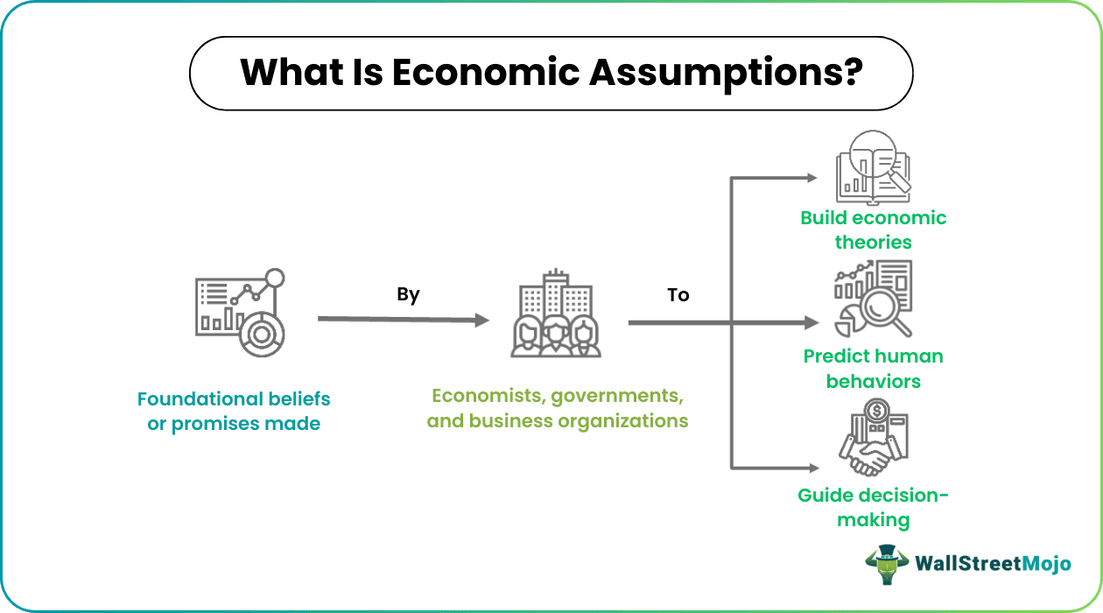

Economic Assumptions can be defined as foundational beliefs held by economists, governments, and business organizations. These assumptions serve to explain phenomena, understand consumer behavior, and facilitate critical decision-making based on these inferences. They form the basis of many economic theories and models, often used for hypothesis testing.

While some fundamental economic assumptions are widely accepted, it’s essential to recognize that economic thought is diverse, with different schools of thought holding varying and sometimes contradictory assumptions. As a result, these presuppositions are often subject to criticism and debate, both among economists and the general public.

- Economic assumptions refer to some concepts that economists, governments, and organizations might take for granted to achieve their objectives of explaining specific theories, understanding consumer behavior, making decisions, and developing economic models.

- There have been many instances where these assumptions have been used to successfully explain some concepts and develop solutions for economic and business problems.

- There are advantages and disadvantages to using such assumptions. On the one hand, it is one of the best ways to prove a hypothesis; on the other, some presuppositions might go too far as to be untrue.

Economic Assumptions Explained

Economic assumptions are fundamental components of both micro and macroeconomics and have been integral to the discipline since its inception. Economics is often characterized as both a science and an art. Economists formulate hypotheses and establish certain assumptions, much like in scientific fields.

These assumptions serve as a starting point, and economists aim to test and validate their hypotheses. When an assumption successfully explains a hypothesis, it is accepted as a theory. Furthermore, economic assumptions play a critical role in helping governments and businesses understand consumer behavior and identifying the factors that influence consumers’ choices and actions. This understanding is invaluable as it enables governments and firms to make informed decisions, develop economic models, and devise policies to optimize their objectives and outcomes.

It is important to note that not all economic assumptions are universal. The field of economics encompasses various schools of thought, including classical, neoclassical, and behavioral economics, which may hold differing assumptions. For instance, neoclassical economists generally assume rational decision-making, while behavioral economics recognizes the influence of emotions and cognitive biases on decisions.

However, the reliability of economic assumptions is subject to debate. Quality and accuracy in these assumptions are essential; they cannot be arbitrarily formulated to explain other economic concepts. Moreover, some economic assumptions have had adverse environmental consequences, as prioritizing economic growth over environmental concerns has contributed to ecological challenges.

5 Key Economic Assumptions

These are the most basic assumptions that form the basis for conventional economic theories and models.

- Scarcity – When economics as a discipline began to evolve, it was defined in terms of scarcity of resources. This limitation on the availability of natural resources led the way for economic transactions and activities. Humans have unlimited needs but limited resources, which thereby influence their actions, which are driven by the motivation to fulfill these needs and derive satisfaction.

- Trade-off – The imbalance between needs and resources compels humans to let go of what they have to gain what they do not have. So, they would have to choose what is more important. When this is done, they pay an opportunity cost. Economic transactions are a trade-off between resources and value (money).

- Self-interest – In economics, it is assumed that human beings act in their self-interest and try to maximize their satisfaction or gains. A simple example would be an agent trying to make a profit by connecting a buyer and seller. When people trade-off, they do so in such a way that either their needs are fulfilled, or they gain from it the most.

- Cost and benefits – Another assumption is that economic participants always engage in transactions by carefully evaluating their costs and benefits. This assumption opines that humans always reason and perform a cost-benefit analysis before buying or selling something.

- Models and graphs – In economics, all the theories and concepts can be technically and logically explained using diagrammatic representations such as models and graphs. Some examples include the demand curve, etc.

Examples

Let us analyze a few examples to gain clarity on the concept.

Example #1

Steve goes to an electronic store to buy a new phone. He plans to buy a brand X phone costing $800. But he came across a brand Y phone with top-notch features and made an impulse purchase of $1500, almost twice his planned purchase price. Steve didn’t stop to think about a cost-benefit analysis. His purchase was wholly based on his emotions. However, Steve might be one of the ten or twenty people who make such decisions. Some people think and buy rationally.

This example illustrates how emotions can override rational economic assumptions businesses tend to make in predicting purchasing decisions.

Example #2

In the realm of traditional economics, the belief that perpetual economic growth is the ultimate goal for societal advancement has reigned supreme. However, there’s a growing movement called degrowth that offers an alternative perspective. At the same time, conventional economic champions’ relentless economic expansion, and degrowth advocates emphasize the need for a more balanced and sustainable approach. They contend that gross domestic product (GDP) is an insufficient gauge of societal well-being and that continued global economic growth, which has seen exponential increases since 2005, is hindering critical climate goals.

Even seemingly modest growth rates of 2-3% annually are viewed as substantial and incompatible with the planet’s ecological capacity by degrowth. Instead, they champion the idea of constraining the production of non-essential goods and curbing demand for unnecessary items, thus paving the way for a more harmonious and eco-conscious future. This shift in perspective reflects a growing recognition of the importance of environmental preservation and societal well-being in the economic landscape.

Frequently Asked Questions (FAQs)

1. What economic assumptions underlay Reaganomics?

Reaganomics refers to the economic policies laid out by the 40th U.S. President Ronald Reagan. Some of the assumptions adopted in the policies are:

– If taxes are decreased, people will spend more, which will, in turn, enable the government to collect more taxes.

– Wealthy investors would put their savings into new businesses.

– Deregulation to remove government control over industries, allowing them to work freely, etc.

2. Can economic assumptions lead to environmental degradation?

Yes, economic assumptions can contribute to environmental degradation. Assumptions of unlimited growth and resource consumption often disregard the environmental consequences, leading to over-exploitation of natural resources, increased pollution, and habitat destruction. Such assumptions have been criticized for their adverse impact on the environment.

3. Are all economic assumptions universal?

No, not all of them are universal. Economic assumptions can vary depending on different schools of economic thought and perspectives. Various economists and economic theories may hold differing assumptions, making them far from universally applicable in the diverse fields of economics.

Recommended Articles

This article has been a guide to Economic Assumptions and its definition. Here, we explain the 5 key assumptions along with examples. You may also find some useful articles here –