What Is A Home Equity Loan?

A home equity loan is taken against a property or a house. It is also referred to as a second mortgage. The main purpose of an equity loan is to help homeowners secure financing by using home equity. The interest on equity loans is lower than on unsecured loans; the property acts as collateral.

If the borrower defaults, the lender has the right to seize the property; but the primary mortgage lender gets to clear liabilities first. These loans charge fixed interest rates. The loan tenure ranges between five and thirty years.

- Home equity loans are issued to homeowners. The property’s loan amount is determined by subtracting the total loan amount from the property’s current market value.

- Since equity loans are considered secured debt, they have lower interest rates than personal loans or credit cards. The property itself acts as collateral.

- Acquiring an equity loan is challenging for borrowers who have poor credit histories. In addition, equity loans are notorious for hidden fees—extra fees, closing costs, etc.

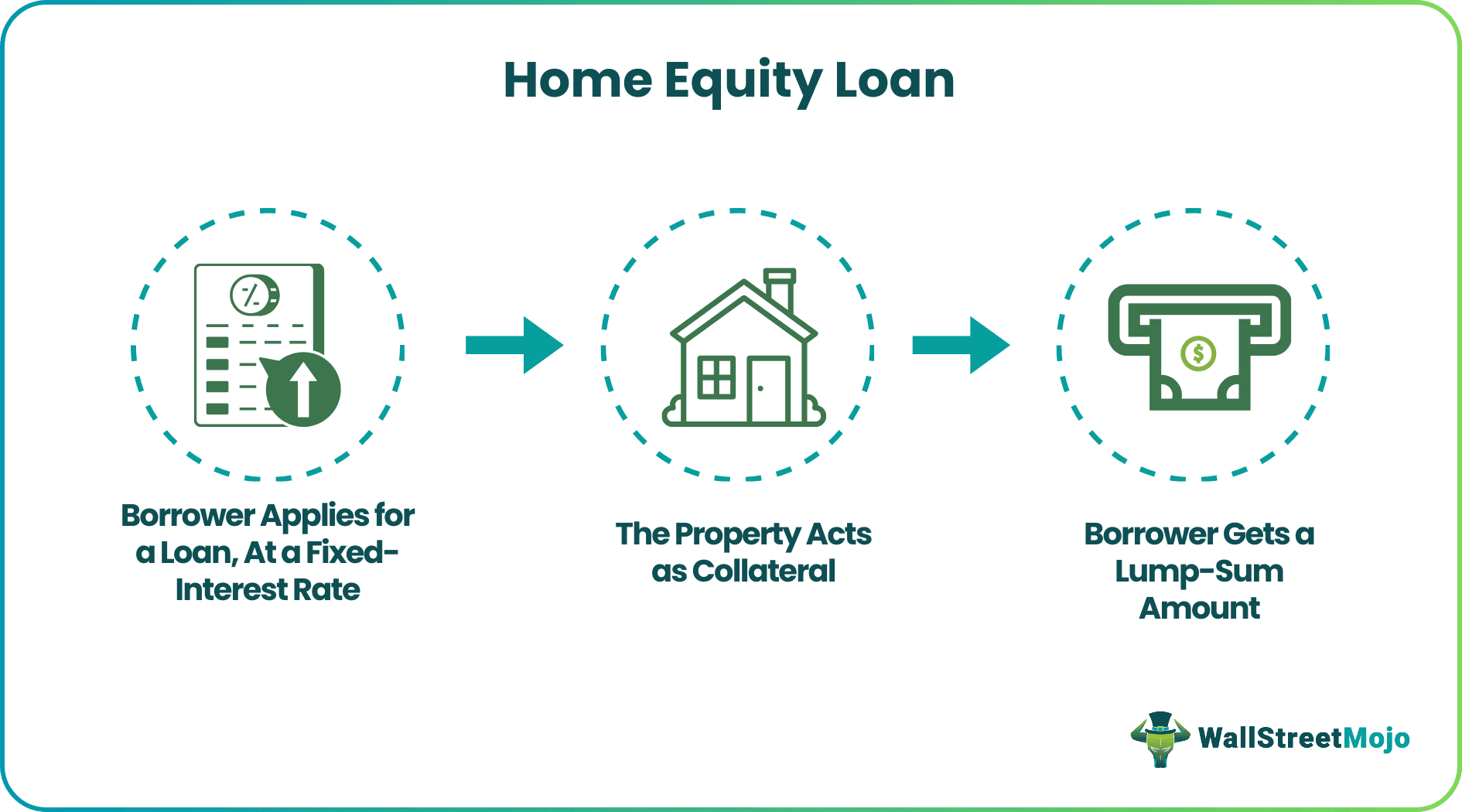

How Does A Home Equity Loan Work?

A home equity loan enables lenders disburse the loan amount against the property (collateral). An equity loan differs between the prevailing market price and the existing loan amount—at a particular time. Also, any lien associated with the property is subtracted from the property’s market price.

When an individual purchases a house on loan, they repay the amount in the form of monthly installments. Simultaneously, the market value of the property rises. The more owners pay off the loan, the more their home equity is. Thus, over time, the borrower’s equity rises—till the lien is completely paid. Once the loan is paid completely, the borrower has 100% equity.

Usually, lenders follow the combined loan-to-value ratio (CLTV). It is the ratio of combined secured loans on the property and its current market value. The CLTV ratio of the property is assumed to be 80%-90%. In addition, lenders consider the credit history of the borrower. Based on these factors, an appropriate interest rate is charged on loans.

Equity loans come with five to thirty years tenure—fixed interest rates. In addition, interests on equity loans are less than credit card interests because these loans are considered secured debt (the property acts as collateral).

These loans are commonly seen during home renovations; it helps borrowers with tax deductions, pressing financial needs, medical expenses, education expenses, etc.

Requirements

Applicants must meet the following home equity loans requirements:

- The credit score plays an important role in determining the interest rate and the loan amount. Ideally, the credit score should at least be around 680. But if a borrower possesses higher credit scores, they can receive lucrative loan terms (borrower perceives fewer potential risks).

- Lenders look for a stable source of income. That is, lenders check the stability of the income source before disbursing the amount. Lenders are subject to higher risk exposure if the employment source or business looks unstable. As a result, they might refuse the loan or apply for higher interest rates.

- These loans are granted based on the loan-to-value ratio of 80%-90%. The borrower needs at least 15-20% equity in the property (ownership) to qualify for the loan. Loan-to-value is a ratio of secured loans on the property and the property’s current market value.

- Lenders prefer a low debt-to-income ratio. The debt-to-income ratio is calculated by dividing total debt by the gross income of an individual. Lenders are exposed to higher risk if the borrower already possesses multiple debts. Again, in such scenarios, the lender refuses the loan application or charges exorbitantly high interest.

Examples

Let us look at home equity loan examples to understand the concept better:

Example #1

Let us assume that Claire purchased a property worth $2,000,000. Then, using the property as collateral, she borrows $1000,000.

Thus, her current home equity is as follows:

- Home Equity = $2,000,000 – $1,000,000 = $1,000,000.

Over time, the value of the collateralized property increases to $5,000,000. The pending loan amount is only $500,000. Now Claire’s home equity is as follows:

- Home Equity = $5,000,000 – 500,000 = $4,500,000.

Alternatively, if the property’s value had fallen, Claire’s equity would also have been reduced. That is, if the property price falls to $1,500,000, with a pending loan of $500,000. Then, Claire’s home equity would be as follows:

- Home Equity = $1,5,00,000 – 500,000 = $1,000,000.

Example #2

In August 2022, a study was conducted by Black Knight. Black Knight is a mortgage technology and data provider.

The study found that US homeowners (nationwide) experienced the largest annual increase in tappable equity, amounting to $11.5 trillion. This occurred in the second quarter of 2022. The typical homeowner doubled their equity (up to 25%). They held at least 20% ownership of their houses during a strong sellers’ market. The demand for houses soared, and the inventory became scarce.

Pros And Cons

The pros of home equity loans are as follows:

- Equity loans have low-interest rates (lower than personal loans).

- Equity loans come with fixed interest rates.

- Since it is a popular loan, borrowers can choose from various options—different banks, payment schemes, etc.

- It encourages people to buy properties. Real estate investments are long-term assets.

- Real estate investment suits those lacking knowledge of capital markets, mutual funds, and financial instruments.

- Equity loans come with long tenures—up to 30 years.

- The interest rate is tax deductible if a homeowner applies for an equity loan for home renovation.

Equity loans also have the following cons.

- Banks readily offer equity loans because the newly acquired property is taken as collateral. This arrangement, though, is risky for the borrowers.

- Characteristically equity loans have long tenures—ten to twelve years—potential risk for the borrower. Therefore, they must ensure a regular source of income well into the future.

- Acquiring an equity loan is challenging for borrowers who have poor credit histories.

- If borrowers fail to make regular repayments, they risk losing the entire property, including the initial down payment.

- Equity loans are notorious for hidden fees—extra fees, closing costs, etc.

Home Equity Loan vs HELOC vs Cash-Out Refinance

Let us look at home equity loan vs HELOC vs cash-out refinance comparison to distinguish between them:

- A home equity loan uses the property as collateral and disburses funds against it. In contrast, a home equity line of credit (HELOC) works like a credit card; the borrower receives monthly installments. In comparison, in a Cash-out refinance (COR), a homeowner takes a new mortgage loan of higher value to close the old mortgage loan—they receive the difference in cash.

- For equity loans, the rate of interest is fixed. For HELOC, the interest rate fluctuates. COR interest rates can be as low as 3%.

Frequently Asked Questions (FAQs)

1. Are home equity loans tax deductible?

Yes, equity loans are tax-deductible if the borrower takes the loan for renovation. In addition, tax deduction of up to $750000 is allowed on HELOCs, equity loans, and residential mortgages.

2. Which is better refinance or a home equity loan?

Cash-out refinance offers very low-interest rates. On the other hand, equity loans are expensive because they are secondary loans. If a borrower defaults, the primary mortgage holder will be paid first.

3. Where to get a home equity loan?

Lenders who offer regular mortgages, such as banks and credit unions, are common sources for home equity loans. They are often a good choice for borrowers with high credit scores and verifiable income. However, their application processes can be lengthy and their lending criteria restrictive.

For borrowers who need funds urgently for business or investment purposes, private lenders offer an alternative. These specialist firms can often provide a second mortgage with faster settlement times and less documentation because they source capital differently. For instance, a firm like Royce Stone Capital works with family offices and private investors, allowing them to fund loans that may not meet traditional bank requirements.

Recommended Articles

This article has been a guide to what is Home Equity Loan. We explain its comparison with HELOC and cash-out refinance, requirements, pros, cons, and examples. You can learn more about it from the following articles –