Secured Loans Meaning

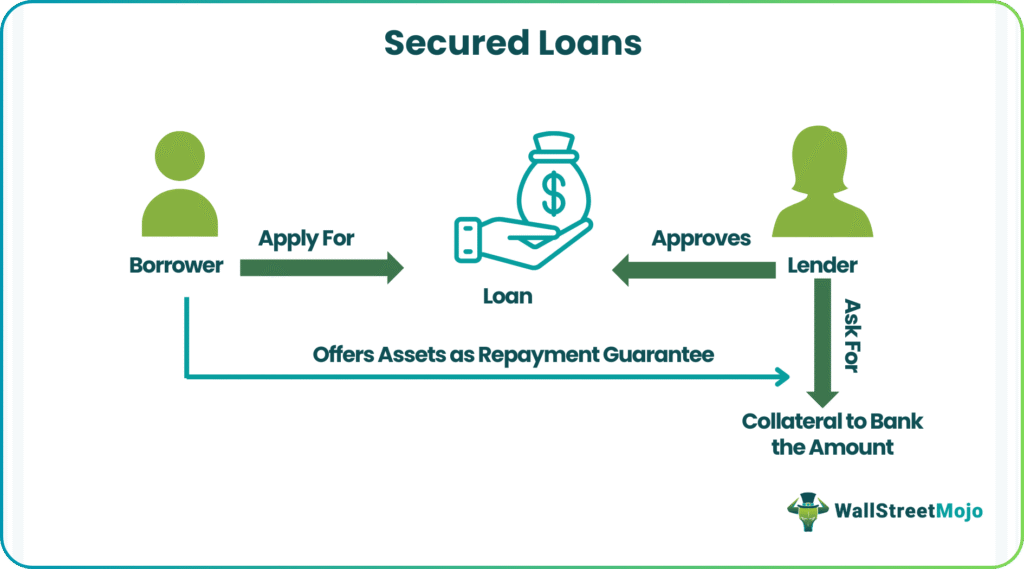

Secured loans refer to the type of loans approved and received against a guarantee or collateral. If they fail to do so, the lending institution acquires the collateral to compensate for the amount that the borrowers were allowed.

Secured loans can be obtained for business purposes and personal requirements. It is different from their unsecured counterparts, only approved based on the borrowers’ credit score. Common types of collateral-backed loans are mortgage loans, car loans, secured credit cards, pawnshop loans, life insurance loans, etc.

Key Takeaways

- Secured loans are finances that the lenders offer against collateral or security at a comparatively reduced interest rate.

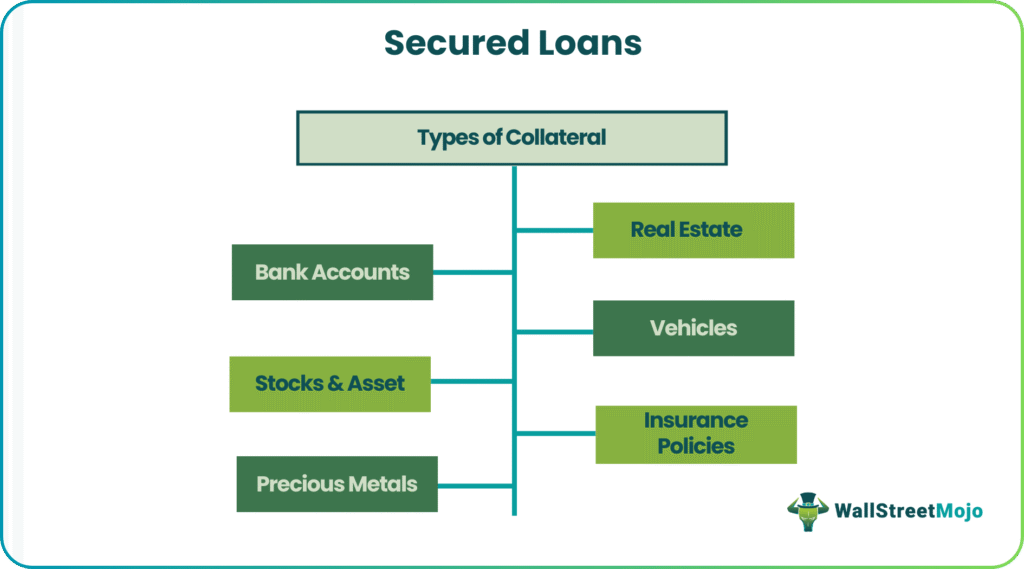

- The types of collateral considered by banks or private lenders include real estate property, life insurance policies, stocks, assets, etc.

- The collateral-based loans are approved fast, given the repayment guarantee that lenders already receive in the form of security.

- These loans against security are meant for personal and business purposes and are mainly preferred when the funds required are high in value.

How Do Secured Loans Work?

Secured loans are called so as the lending institutions, be it a bank or a private lender, secure the loan amount against collateral. Collateral is an asset or set of assets that back borrowers’ promise to repay the loan amount within the specific period. As a result, the financial institutions acquire the assets that borrowers offer as a guarantee for repayment in the event of default.

In short, the collateral tends to be the condition that, when found satisfactory, allows lenders to approve the borrowers’ loan application. Collateral/security can be anything, from real estate property to a bank account to stocks and assets to life insurance policies, etc.

Such collateral-based options are available for large loan amounts, which borrowers are likely to default on. The only aim of such loans is to ensure that lenders recover the lent amount irrespective of the financial crisis or other struggles the borrowers might go through. A loan seeker is expected to pay the installments at regular intervals. If borrowers are unable to pay back, their asset or collateral acts as a security. The lenders can use it to get back their lent amount in such events of default.

In short, collateral-backed loans assure the lender of repayment even if the amount is too huge. As a result, people with poor credit ratings can also take secured loans for bad credit for their personal or business purposes. Moreover, borrowers are likely to receive a loan at a much lower interest rate due to this assurance.

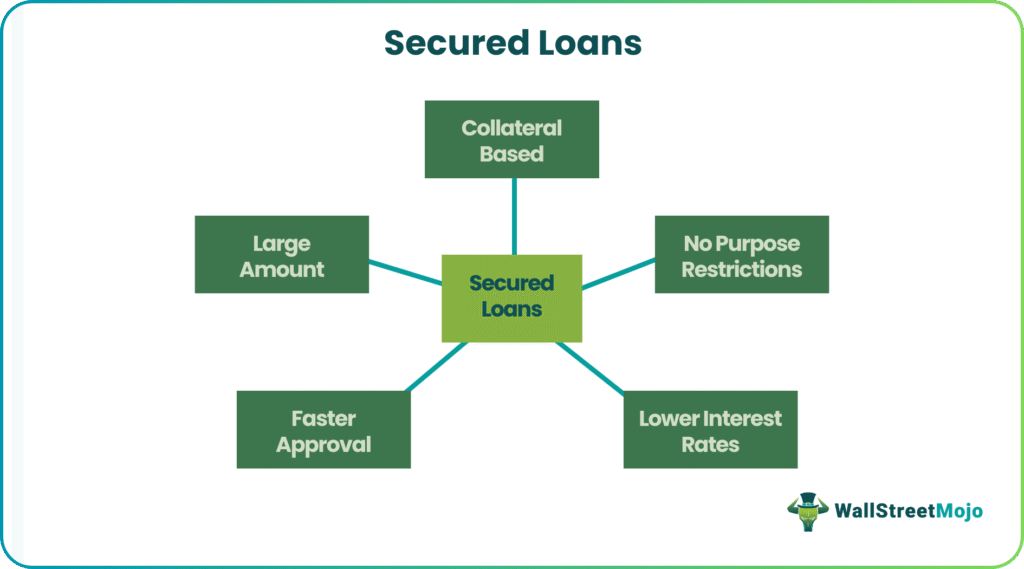

Features

#1 – Collateral-Based

The secured loans are collateral-based, i.e., the funds are lent against security to secure lenders. Thus, the borrowers use an asset/property as collateral to back the loans. In most cases, however, the borrowers use the same house or car to secure the loans they take up loans to purchase. This arrangement helps buyers buy assets/equipment easily, and at the end of the day, the lender also remains secure.

#2 – Lenient Interest Rate

The interest rate is comparatively lower given the guarantee against repayment that lenders receive from borrowers. Thus, borrowers have to pay less interest than an unsecured loan.

#3 – Large Amount

Most people apply for collateral-based loans when they require borrowing a significant amount. And when the amount is higher, lenders need assurance for repayment. Hence, the borrowers back the loan amount with an asset to ensure the lenders are less worried about the huge amount and its payment terms.

#4 – No Purpose Restrictions

These loans are available for both personal requirements and business purposes. Hence, your purpose doesn’t determine whether you will be allowed to take the finance. However, the terms and conditions for secured loans for business are a bit different. Since the businesses have more money to pay off, the loan amount is usually higher than housing and car loans. Therefore, a business must let the bank/financial institution use one of its assets/machinery/furniture/raw materials as collateral for the loans.

#5 – Faster Approval

As the loan is collateral-based, lenders focus on is the property kept as a security against the lent amount. Thus, the application or credential verification takes a backseat, making the approval process faster.

Advantages & Disadvantages

Though collateral-backed loans help borrowers fulfill their personal or business requirements in different ways, it has certain limitations at the same time. Here is a list of the pros and cons of these loan options:

| Pros | Cons |

|---|---|

| Lower interest | Chances of loss of assets |

| Faster approval | Some lenders offer collateral-specific loans (e.g., a house for a home loan) |

| Tax deductions are applicable | |

| No strict rules to qualify |

Examples

Let us consider the following secured loans examples to understand the concept better:

Example #1 (Conceptual)

Mary desires to buy a car. So, she contacts a bank for a car loan. The bank says that they will approve the loan on one condition. It states that the loan seeker needs to keep the car as collateral until the loan amount and the interest charges are paid off.

The lender also clears that Mary’s acceptance will mean a much lower reduced interest rate for the loan amount. So, she agrees and acquires the housing loan to buy her dream house.

Example #2 (In the Event of Default)

Roger takes a housing loan from a bank and pays off the loan in installments. However, he lost his job and started defaulting as he ran short of funds. As a result, the bank declares ownership of the house. The bank conducts property valuation and notices that the market value of a house isn’t enough to pay off the entire loan. So, the bank sells off the house and asks Roger to pay the difference.

Secured Loans vs Unsecured Loans

Secured and unsecured loansare two loan options borrowers receive while looking for finance. Though both these alternatives assess the credit score and eligibility of the borrowers before approving the funds required, there are a few differences between the two that loan seekers must be aware of before choosing one of them.

As the name suggests, collateral-backed loans are secured against collateral/security. These are applied for or offered to individuals who require a large amount to make a big purchase. As the loan repayment is guaranteed, the approval is faster as no specific credentials need to be verified. The collateral backing the loan amount is enough.

On the other hand, an unsecured loan is obtained based on the credit score that the borrowers acquire. Some examples of such loans include student loans, personal loans, etc. The income proof and other financial credentials are perfectly checked along with the credit scores. The lenders approve the loan application if the score and ratings are up to the mark.

As these loans are collateral-based, the secured loan rates are lower as lenders are assured of receiving repayments even in the event of default. On the contrary, the interest rate charged is higher for unsecured finances as there is no guarantee against the lent amount.

Frequently Asked Questions (FAQs)

What are secured loans?

Secured loans are finance alternatives that lenders offer borrowers only when they keep an asset/security as a guarantee against the lent amount. It is to ensure they can repay the amount even if they are not in a position to. In short, a collateral-backed option secures the lenders’ amount in the event of default.

Do secured loans build credit?

Yes, these loans help build your credit history. Thus, secured loans for bad credit must be applied for and used when required. If people with a bad credit history need a loan, they can keep their assets as collateral and pay the installments on time to make sure they can retrieve their property after the repayment is made in full. As a result, they get a chance to build their credit history positively.

Are secured loans good or bad?

Secured loans are, of course, good as they help loan seekers make big purchases by paying lower interest rates for the funds acquired. However, the only risk is the collateral kept as a guarantee against the lent amount with the lender. In case of default, borrowers might lose the assets completely.

Recommended Articles

This is a guide to what is a Secured Loan, its meaning and features. Here we explain its benefits and limitations along with some practical examples. You may also learn more about fixed income from the following suggested articles –