Part of our Option Strategies guide

What Is An Iron Condor?

An iron condor is an options trading strategy that lets investors play safe and ensure profits by restricting their upside and downside risks. It allows them to enjoy two call and two put options and have four strike prices to take the trade. A mature trader can easily facilitate steady income using this strategy.

While the call option allows traders to buy, the put option lets them sell assets/derivatives based on how suitable they would be based on the current market fluctuations. The selection of strike prices and the prediction of market volatility play an important part in the iron condor strategy, helping people earn a profit when the market doesn’t show any significant movement.

Key Takeaways

- An iron condor is an options trading strategy with four strike prices for investors to close a trade, helping them be in a safe zone and trade at a limited risk.

- The four strike prices allow them to take trades at long call, long put, short call, and short put options.

- It differs from the regular condor strategy, which allows two puts or two call options.

- This is a limited risk and limited profit strategy. So, the investor will fear being trapped in deals involving unlimited risk.

Iron Condor Explained

The iron condor options technique is a limited risk strategy that offers four strike prices, giving investors a safe zone for returns in a non-volatile market. This strategy is based on options, which are derivative instruments. Therefore, the security on which the strategy is planned should belong to the derivative market.

The iron condor strategy is only applicable when the market is non-volatile. In the case of a volatile market or extreme movements, the strategy seldom works. An initial inflow is the maximum profit for the deals strategized using this technique.

The strategy maximizes profits if the underlying security price remains between the middle strike prices. The call and put options are bought to avoid extreme outcomes of the movement of stock prices in one particular direction. If the non-volatile market persists, the strategy helps earn a sustainable profit.

Conversely, a multi-leg strategy, a reverse iron condor, limits the profit potential and is risk-defined. However, unlike the iron condor technique, its reverse counterpart helps traders play safely in a volatile market. Here, the trader buys a lower strike out-of-the-money (OTM) put and sells OTM put at an even lower strike. In addition, they can buy an OTM call at a higher strike and sell a call at an even higher strike point.

Iron Condor Options Strategy

The iron condor strategy offers four options:

- Long call (Buy a call option at a strike price higher than the current asset price)

- Long Put (Buy a put option at a strike price lower than the current asset price)

- Short Call (Sell a call option at a strike price lower than the long call)

- Short Put (Sell a put option at a strike price higher than the long put)

All four options are placed at different strike rates. The selection of strike prices and the prediction of volatility is crucial. Once the strategists determine the strike prices, it helps provide sustainable income until the market remains non-volatile.

Traders receive money when they sell options and pay when they buy them. The options are bought and sold to ensure an initial inflow at the initiation of the strategy. The initial inflow is the maximum profit a person earns from this strategy.

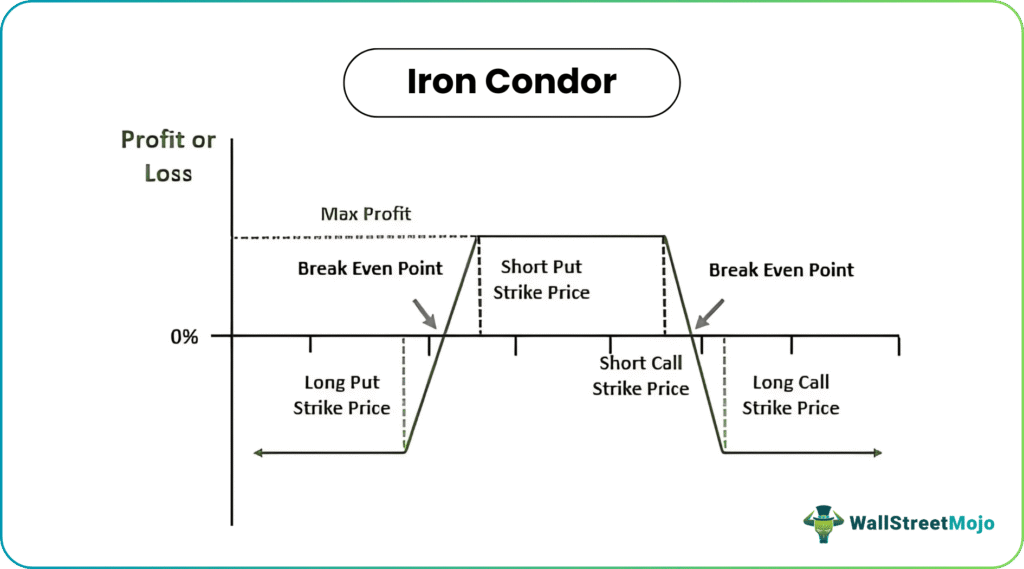

The iron condor strike prices are chosen so that if the share price remains between the middle two strike prices, the strategy guarantees maximum profit.

The concept can be understood clearly with the help of the following example and diagram given. In the diagram, the portion depicting the profit and the loss are well identified. If the price of the underlying asset is within the short-strike prices, as given in the diagram, then there is profit. However, during expiration, if the price of the underlying asset goes above or below the strike prices, the trader will incur a loss. The breakeven figure points are also clearly marked in the figure. Traders sometimes exit the positions before the expiration. This is done either through an exit from the entire strategy, exiting from any one spread, or buying back the short option from the strategy.

How To Trade?

This strategy applies when investors know the security price won’t move much. When traders sell options, there is limited profit but unlimited loss potential. Thus, if investors think the stock price will not move, they decide and choose sell options to earn the premium. The investors sell at the money (ATM) or close out of the money (OTM) put and call to generate a higher return.

As investors are more into selling put and call, the stock price moves up or down. If the stock price moves up, it indicates huge losses in the sold call. On the other hand, if the stock price moves down, it depicts the chances of loss on the short put. In such a scenario, the investors are recommended to opt for buying options to prevent such extreme outcomes. Thus, the investors buy a call option to hedge from a short call and a put option to be safe from a short put.

Now, if the stock price doesn’t move, all the options expire, and the investors still have the initial inflow, which is their maximum profit. Investors lose the initial inflow and incur losses if the stock price moves. The losses, however, remain limited to a bracket.

Example

The share price of XYZ is $100. Mr. X thinks that the stock price will remain at that level. So, he plans to set up a strategy to earn from the non-volatility.

- Call Option @102 Strike – $10 Premium

- Call Option @115 Strike – $5 Premium

- Put Option @ 98 Strike – $12 Premium

- Put Option @ 80 Strike – $7 Premium

The call option with strike 102 is very close to the share price, so it is a kind of ATM call. By selling this option, X has a chance to earn a $10 premium. The trader buys an OTM call option to be safe from the sudden movements in the stock price by paying a premium of $5. Therefore, the net premium earned in this leg is ($10 – $5) = $5

When X notices that the stock price is less likely to move, he bets on the downside. As he thinks that the price will not go down, he sells an ATM put in to ensure earning a higher premium. The premium earned from the strike price at 98 is $12. However, the trader will incur a loss if the stock price falls below expectations. Thus, he buys a put option to protect himself. The premium for OTM put is less.

So, here:

- X buys an OTM put @ strike 80 by paying $7.

- Net inflow from this leg is ($12 – $7) = $5

- Total inflow from both the legs = $5 + $5 = $10

Other Potential Scenarios

- If the stock price remains between $98 to $102. Then all options are worthless, and the investor earns $10.

- Suppose the stock price goes below 98 and reaches 80. The call options are worthless as investors will incur a loss from the short put. The loss amount, here, will be ($98 – $80) = $18. Once the stock reaches $80, the long put can prevent the investor from further losses. As the inflow was $10 and the outflow was $18, the net loss came to $8.

- Suppose the stock price moves above 102 and reaches $115. The put options will expire worthlessly, making the trader incur a loss of ($115 – $102) = $13 from the short call. When the stock price reaches $115, the long call protects traders from further losses. So, here, the total inflow is $10 and outflowed by $13, indicating the loss worth $3.

This is how to trade and make iron condor profitable if the stock price remains in the middle.

Iron Condor vs Iron Butterfly

Both iron condor and iron butterfly offer four trading options to investors – two calls and two puts. While the former involves lower risk and reward provision, the latter is a higher risk-higher reward option. However, as the short positions of the iron butterfly are equal to or almost close to the current price of the asset in question, the premium collected is way higher.

Frequently Asked Questions (FAQs)

What is the iron condor options strategy?

An iron condor is a derivative strategy designed to earn a profit on a limited loss and limited profit basis with four options having the same expiration date at different strike prices. This helps create a strategy to earn profit in a non-volatile market.

How to adjust the iron condor?

Investors/traders can also opt for iron condor adjustments by making slight changes in the trade, considering the market movement. They might also extend the time range for taking the trade.

Are iron condors profitable?

Yes. The iron condor strategy is profitable, especially when the underlying security price is between the middle strike prices and expires. However, even the movement in the market would not lead to severe losses as the risk is limited.

Recommended Articles

This is a guide to What is Iron Condor. We explain its options and how to trade it with an example and compare it with an iron butterfly. You may learn more about financing from the following articles –