Part of our Option Strategies guide

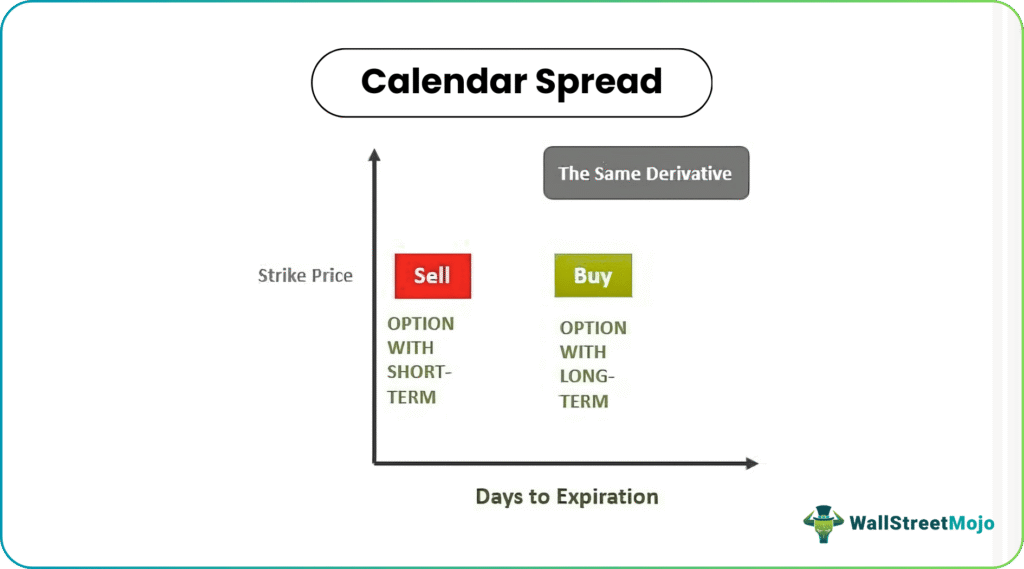

Calendar Spread Definition

A calendar spread (or time spread) refers to a market-neutral strategy of buying a long-term call option and selling a short-term call option of the same derivative simultaneously, having the same type, strike price, and slightly varying expiration times. It minimizes the impact of time on the options trade for the day traders and maximizes profit.

Options and futures traders mostly use the calendar spread. It is beneficial only when a day trader expects the derivative to have a price trend ranging from neutral to medium rise. It is a low-risk strategy to profit from the transit of time and implied volatility of derivatives. The prices of options start decaying on approaching the expiration date.

Key Takeaways

- A calendar spread is technique traders employ to buy and sell the same derivative of the same strike price but with different expiration dates.

- It helps in minimizing the effect of time decay on options trading. However, as the expiration time gets extended, the premium also increases.

- It involves selling a shorter-dated contract and simultaneously buying a longer-dated contract. The lesser expiration date option gets sold, and the long expiration date option gets bought, as a rule.

- Time spread adjustments get utilized by traders to derive additional credit during options trading.

Calendar Spread Option Strategy Explained

A calendar spread strategy is a market-neutral option or futures strategy in which traders anticipate various volatility levels of derivatives at different periods, having controlled risk in either direction. The sole aim of such a calendar spread is to garner profit using the directional derivative trend towards the strike price at low risk when the market goes in the opposite direction.

The calendar spread option strategy consists of purchasing a call option long-term and selling a call option short-term derived from the same financial instrument with the same exercise price but a different expiration date. In other words, traders try to benefit from the anticipated differences between time transit and options volatility. As a result, they can minimize the risk and impact arising out of price trends of the derivative options.

Technically, time spread allows the traders to trade at different degrees of volatility skew to:

- Make the most of the acceleration of decay of time or theta.

- Limit the vulnerability of impact on the price of derivatives.

In a way, the calendar gives the required flexibility to create the trading so that options trading becomes profitable irrespective of the underlying security of the derivative, whether it –

- Rises,

- Falls, or

- Remains stable.

Moreover, the time spread has two legs of similar options- calls or puts. Traders buy one leg, whereas they sell the other leg, but both have the same strike price and different expiration dates. As a rule, the sell option has a lesser expiration date than the buy option. Furthermore, the premium for a longer expiration time is higher. As a result, investors trade the time spread for a debit. A time spread helps the traders focus on options’ time value rather than their volatility dynamics.

Calendar Spread Type

These spreads are also called horizontal spreads and are different from vertical spreads. Vertical spreads consist of buying and selling an option of the same type and expiration, but with different strike prices. They are also called intra-market, inter-delivery, or time-spread.

- Diagonal Calendar Spread – It is a spread wherein, for a month, traders use two different strike prices. So, in short, it is a modified spread. It involves different strike prices. While entering it, the investors believe in the neutrality or bearishness of the stock price for the short term.

- Double Calendar Spread – It involves buying future months’ call and put options and selling near-month calls and puts with the same strike price.

- Reverse Calendar Spread – It acts reversely, wherein the traders take an opposite position. They sell a longer-term option and buy a short-term option on the same underlying security.

Examples

The following calendar spread examples will help us understand the topic more clearly.

Example #1

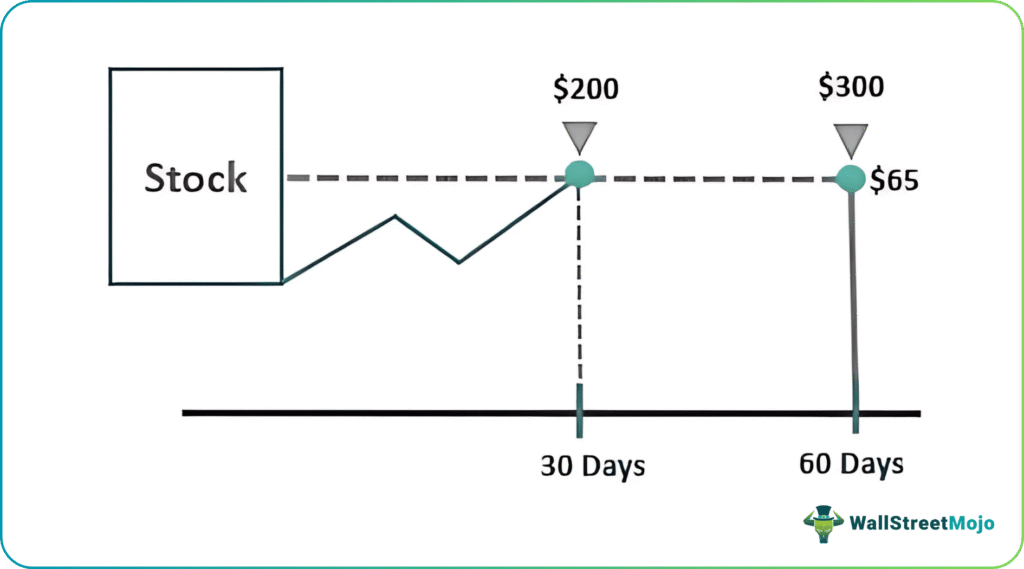

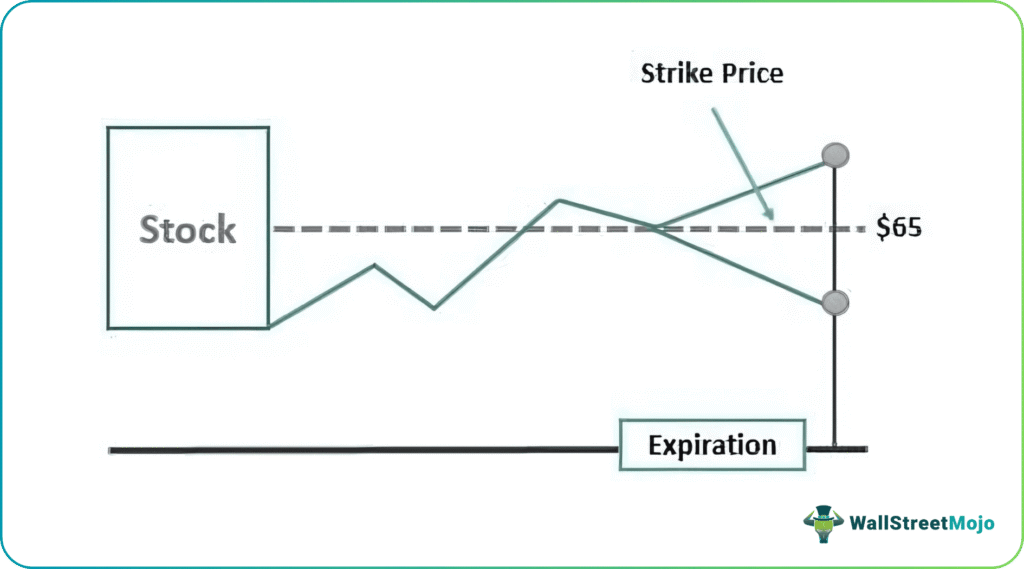

Let’s take an example of XYZ stock trading at $65 to understand the calendar spread strategy.

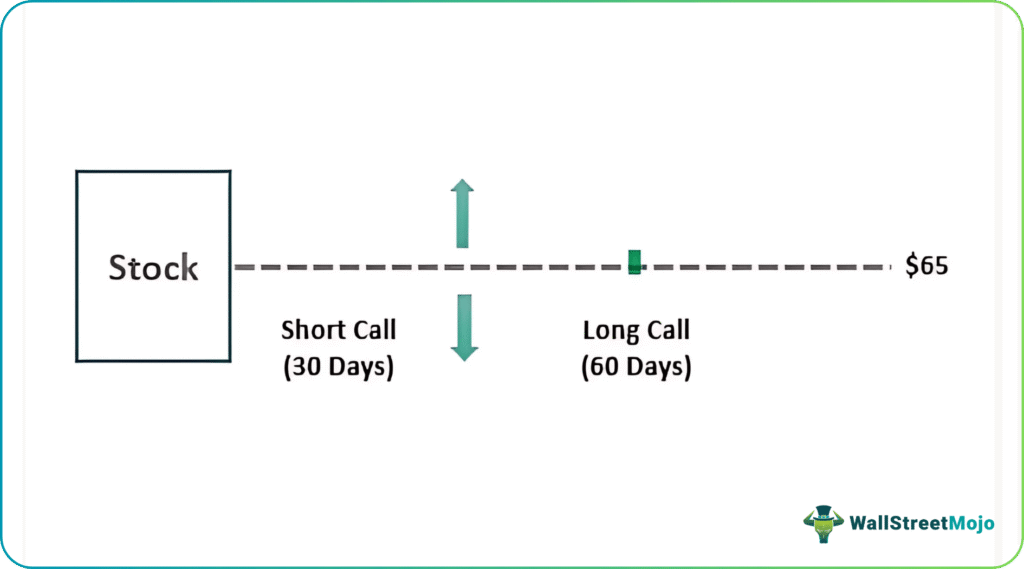

An investor sells a $65 strike call with 30 days until expiration for $2 or $200 of premium and simultaneously buys a $65 strike call with 60 days for expiration for $3 or $300 of premium (Figure 1). The investor thus pays $1 for the calendar. So, the maximum risk is $100 ($300-$200=$100) per spread. This example sells a 30 days option, but the investor may choose to sell weekly options to take advantage of accelerated time decay.

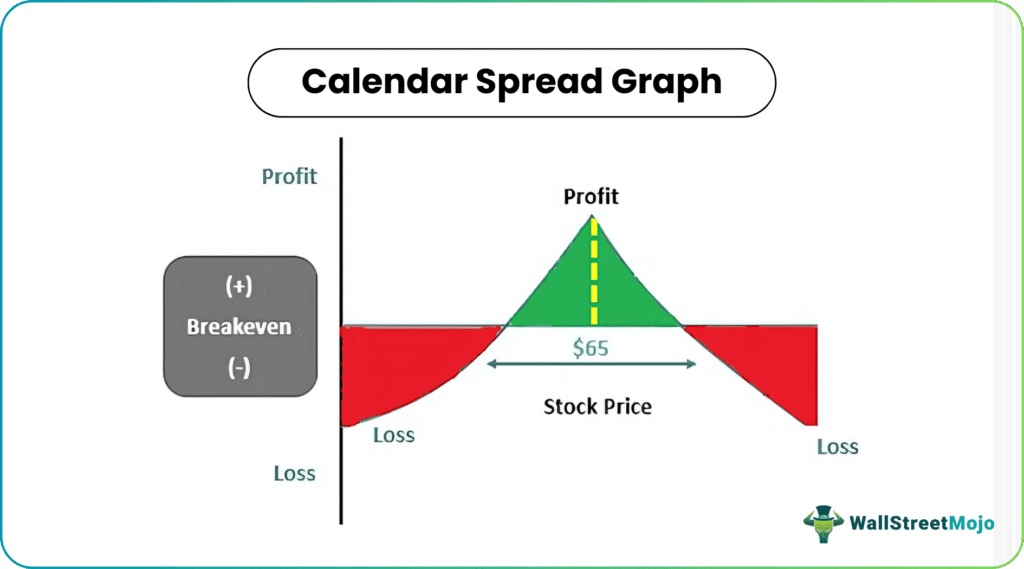

- XYZ stays near $65: As long as the stock trades near $65, the calendar spread will profit from the time decay of the short option premium (Figure 2). Longer-term option decay at a slower rate than shorter-term options. Even though the long option part of the spread is losing money from time decay, the short option decays faster. This difference generates a profit.

- XYZ moves far from $65: While the investor is waiting for the near-term option premium to shrink over time after initiating the calendar spread, the stock could easily move away from the strike price in either direction (Figures 3 & 4).

Though the underlying can certainly move enough to create a loss in the trade, it would take a substantial move to create a complete loss. However, investors must always decide how much they are willing to lose before placing any trade.

- XYZ finishes at $65: With XYZ at exactly $65 at expiration, the short call is worthless, but the long call still has value and is worth $2 (Figure 1). So the value of the calendar spread has widened to $2. Note that this is the best-case scenario, and it is unlikely that the stock will settle exactly at the options’ strike price at expiration.

- XYZ above or below $65: If XYZ settles slightly higher or lower than $65 at expiration (Figure 4), the net profit will shrink.

Profits will continue to shrink and eventually turn into a loss the further the underlying moves away from the $65 strike.

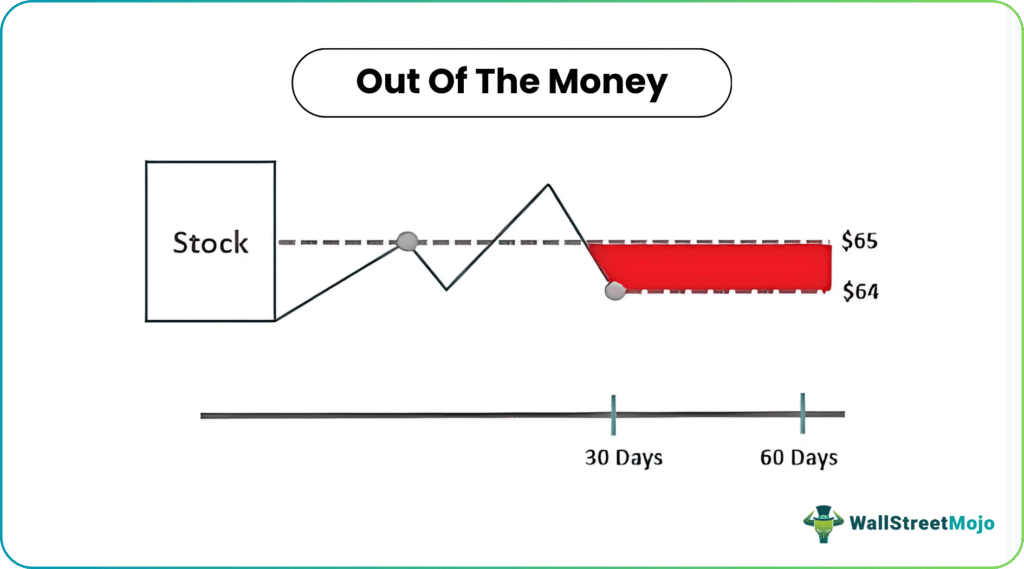

- XYZ is below $65 at expiration: With XYZ at $64 (Figure 5), the short call option is out of the money and expires worthless. However, since the investors still have the long call option, that option can later be sold to lock in again. Or, if one forecast is now bullish, the investor may keep the long call with theoretically unlimited upside profit potential.

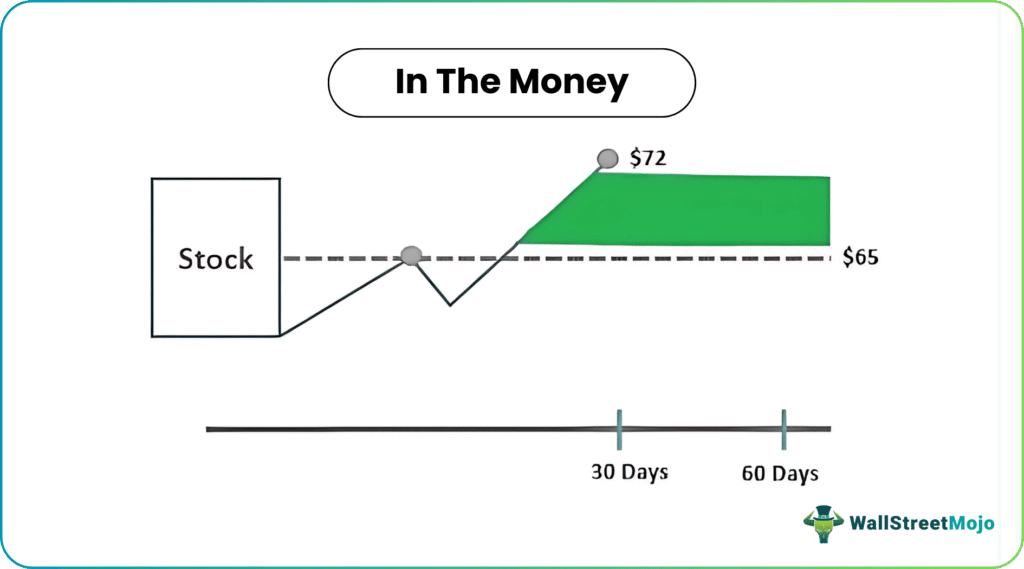

- XYZ is above $65 at expiration: Let’s assume that XYZ closes at $72 (Figure 6) at expiration. With the stock above the the strike price, the short call expires in the money, and the investor must sell a share. To avoid assignment, the trade can be closed anytime before expiration.

The calendar spread may produce a good rate of return when an investor’s neutral forecast is correct, with the underlying closing at or near the strike price of the call options.

Example #2

Here is another example to understand the calendar spread options strategy.

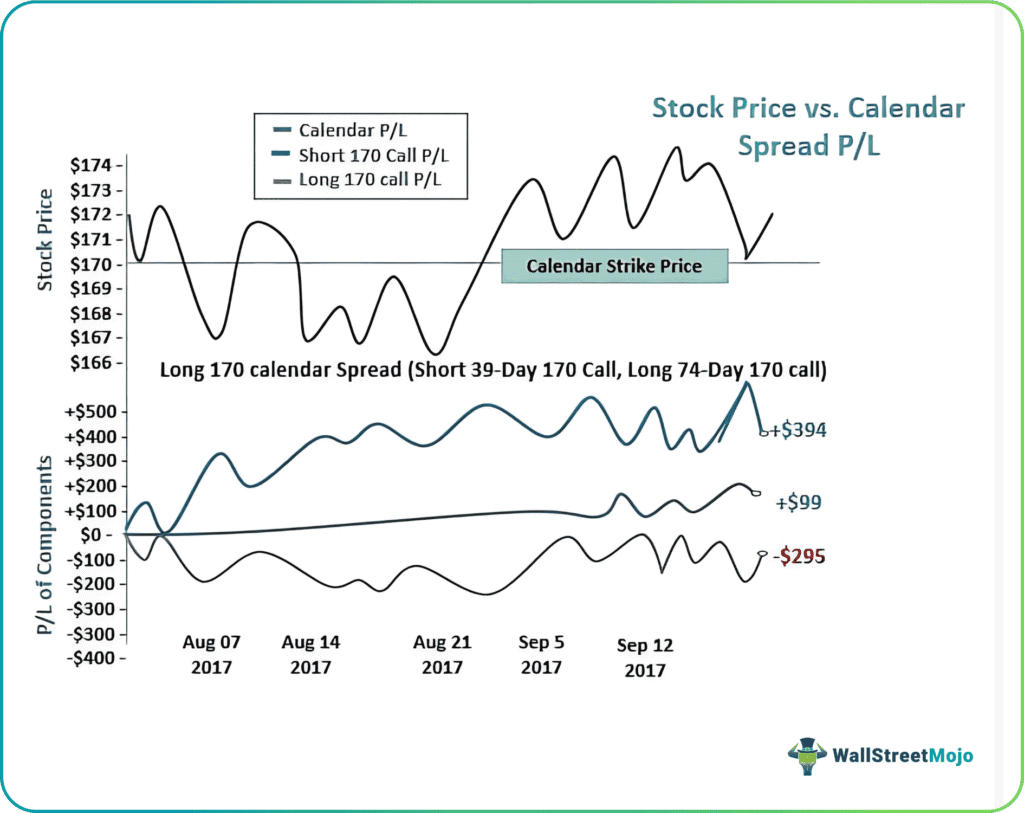

Let’s assume here that the stock price at entry is $171.98. In this trade, everything is kept constant except the expiration cycle of the two options.

Here, the long calendar components are as follows:

- Short 170 Call (39 Days to Expiration)

- Long 170 Call (74 Days to Expiration)

Now, let’s assume the calendar spread entry price to be the following:

- Sold 39-Day Call for $5.50

- Bought a 74-Day Call for $7.75

So, entry price = $7.75 – $5.50 = $2.25 (Paid)

The trader is anticipating the stock price to remain close to $170 as time passes since she purchased the 170-call spread. Further, the spread’s price should increase if the stock price remains near the strike price of the calendar (here, $170). Since the price of the long calendar spread is calculated by subtracting the price of the short option from the price of the long option, we get the following data:

| Date | Short Call Price | Long Call Price | Calendar Spread |

|---|---|---|---|

| Entry Date | $5.50 | $7.75 | $2.25 |

| Near-Term Expiration | $1.56 (-$3.94) | $4.80(-$2.95) | $3.24 |

Further, the stock price hovers around the strike price of $170, and the spreads’ price increases from the entry price of $2.25 up to $3.24. The price increased due to a decrease in the short calls’ price at a faster rate than the long calls’ price. So, in this example, the short $170 call that the trader initially had 39 days to expiration lost $3.94 of value over the period, while the long $170 call with 74 days to expiration at entry lost $2.95. As a result, the spread price increased as the short option lost more value than the long option.

Since near-term options decay faster than longer-term options, the long calendar spread increased from the entry price, generating profits for the trader who bought the calendar spread.

The Profit & Loss of the calendar spread can be visualized by looking at the P&L of the components over time. The top part of the graph depicts the changes in the stock price relative to the calendar strike price of $170. The other half shows the P&L of the spread as a whole and each option component of that calendar spread.

For example, since the trader sold the $170 call for $5.50 and it decreased by $3.94 (Table 1), the P&L on the short $170 call is +$394. On the other hand, the trader buys the $170 call in the long-term expiration cycle for $7.75 and loses $2.95 of value, which accounts for a total loss of $295. Hence the net P&L here is $99. Thus the trader makes a net profit of $99.

Calendar Spread Adjustments

The calendar spread adjustment is related to the put of options derivative. Traders adjust the put calendar spreads during the options trading to increase the credit. For example, one can adjust calendar spread in the following manner:

- If the prices of the derivatives rise incessantly just before the maiden expiration date, then the traders buy the short put option.

- After that, the short put option gets sold off when its price attains the underlying stock’s price or security of the derivative.

- As a result, the trader gets extra credit for trading the derivative of the option.

Frequently Asked Questions (FAQs)

What are calendar spreads?

The time spreads are a neutral options strategy with low risk and directional characteristics that gain from the time transit or surge in the implied volatility.

How to adjust the calendar spread?

One can adjust the time spread by replacing short calls with higher strike prices when the stock rises so that it is expected to breach the upper limit of the break-even range. Moreover, one must adjust when the stock falls to an extent where there is a possibility of the breach of the lower level of the break-even range.

When to use calendar spread?

The best time and strategy to use the time spread is when one expects the security price to reach the proximity of the strike price just near the expiration of the front-month option.

How to trade calendar spreads?

With calls or puts, one can trade time spreads as they are equivalent to price strikes and expirations while using ATM (At the Money) strikes for making trade neutral and OTM (Out Of The Money) or ITM (In The Money) strikes for biased trade.

Recommended Articles

This article has been a guide to Calendar Spread and its definition. Here, we explain its types, examples, and calendar spread adjustments. You can also go through our recommended articles on corporate finance –