Part of our Option Strategies guide

What Is Debit Spread?

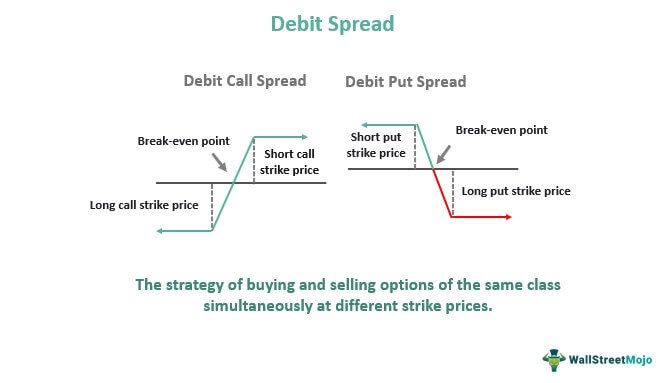

A debit spread is an options strategy created by buying an option with a higher premium and selling an option with a lower premium simultaneously. A debit occurs when the premium paid is higher than the premium received. The underlying assets and classes of the options involved in the strategy are the same, but the strike prices differ.

The strategy can utilize two or more options, but the cost of purchasing the options should be greater than the price received for selling the options. In other words, the initial return from selling options is lower than the cost of buying the options. Hence there is a net debit from the trader’s/investor’s account. Therefore, it is referred to as the debit spread.

- A debit spread is an options strategy of simultaneously buying and selling options of the same class. Both options share the same expiration date but different strike prices, and the difference in premium should result in a net debit.

- The trader’s account is debited in this type of trading. At the same time, the trader’s account is credited in case of the credit spread.

- In credit spread, the trader sells the stock at the high premium rates and purchases at the low premium rates, while at the same time, it is risky to trade in credit spread. In contrast, it is less risky to trade in the debit spread.

Debit Spread Explained

A debit spread is also known as the net debit spread. It involves buying and selling an option within the same asset class on the same underlying asset at different strike prices on the expiry date. One can design a bullish and bearish debit spread.

Generally, it can be a debit put spread or call debit spread. Bear put spread is another name for the debit put spread. The term “bear” relates to the technique of making money when stock prices are bearish or declining. The word “debit” describes how the plan was developed to result in a net cost or net debit. Call debit or bull call spread contains buying and selling a call option with the same expiration but different strikes.

Adjustment

Prompt debit spread adjustment can help traders reduce the risk associated with the strategy. For instance, in the case of a bull call debit spread (bull call spread), there is a fixed expiration date hence the time to make a profit is limited. Like most options strategies, the bull call spread can be adjusted, but cost increases the risk and extends the break-even point.

When the price starts decreasing at a fast pace, the trader can add a bear put spread at the same strike price and expiration as the bull call spread. As a result, a reverse iron butterfly is formed, which makes the put spread profitable if the underlying price declines further.

Examples

Let us look at examples to understand the concept better:

- Call debit spread: A trader buys a call option with a strike price of $100 for $2 (long call). At the same time, the trader sells another call option on the same underlying security with a higher strike price of $105 for $1 (short call). The debit value or the net cost of the spread is $1 ($2-$1). The difference between strike prices is $5 ($105-$100). The maximum profit will be the difference between strike prices minus the net cost of the spread of $4 per share ($5-$1). The maximum profit can be realized when the stock price moves above the short call’s strike price at expiration.

- Put Debit Spread – Another simple example is a trader buying a put option with a strike price of $50 for $4 and simultaneously selling a put option with a strike price of $40 for $2. Therefore, the established net debit is $4-$2, which is $2.

Risk

If the stock price at expiration is below the lower strike (strike price of the long call), both call options will expire without making any impact. The maximum risk will be the net cost of the spread, including commissions. In other words, a loss of the net cost of the spread occurs if both call options are held to expiration and expire when the stock price is below the lower strike.

Debit Spread vs Credit Spread

Let’s look at the difference between debit and credit spreads:

| Debit Spread | Credit Spread |

|---|---|

| The trader buys a high-premium option and sells a low-premium option on the same underlying asset. | The trader sells a high-premium option and buys a low-premium option on the same underlying asset in a credit spread. |

| Net payment: The trader’s account gets debited because the cost of purchasing the option is more than selling the option. | Net receipts: The traders receive a credit to their account because they sell an option with a high premium and buy an option with a low premium. |

| Apt during the period of low implied volatility | Apt during periods of high and low implied volatility |

Frequently Asked Questions (FAQs)

Is a call debit spread bullish?

Call debit or vertical call spread is a bullish options trade with a maximum profit and loss determined upon entering. Call spread occurs when one purchases a call option with a strike price and sells another with a higher strike price than the other, and they both possess the same expiration date. The maximum loss will be the net debit or net premium paid. The maximum profit will be the spread between the call strikes minus the net premium of the contracts.

When would you use a debit spread?

It is preferred when the implied volatility percentile falls or below 50%. Furthermore, traders may use it to offset the cost of purchasing a pricey option. If they anticipate a modest price change in the underlying asset, they can opt for a debit spread rather than buying a single option. Furthermore, they are available in bullish and bearish forms.

What is the max profit on a debit spread?

The maximum profit and loss are easily identifiable. The maximum potential profit equals the width of the strike prices minus the debit paid. The maximum loss potential is equal to the net debit paid.

Recommended Articles

This has been a guide to What is Debit Spread. We explain its adjustment techniques, examples, and comparison with the credit spread. You may also find some useful articles here –