Part of our Option Strategies guide

What Is An Interest Rate Floor?

The Interest Rate Floor in finance refers to the minimum interest rate applicable on the various derivatives products and loan agreements. The sole purpose of the floor application is to set the lowest interest rate that can be charged to the borrowers.

The interest rate floor stays below the interest rate cap. It acts as a bare minimum range above which the floating rate can move. As a result, most loan contracts and credit facilities work on the interest rate floor pricing. However, this rate might fluctuate with the borrowing costs. Moreover, it offers stability and protects borrowers from excessive interest rate fluctuations.

Key Takeaways

- Interest Rate Floor is a contract clause where financial institutions and lenders charge a minimum interest rate. They cannot set rates above this floor.

- These floor rates protect lenders from falling interest rates during a recession. These rates do not wish to lose on the lending cost due to the low rates.

- Hence, these are primarily applicable to derivatives products and loan products.

- The only difference between the interest rate floor and Cap is that the latter is above the ceiling, and the former is the minimum level.

Interest Rate Floor Explained

The Interest Rate Floor is the lowest bracket for a lender to charge an interest rate to the borrower. In other words, even if the market fluctuates, the former will charge the minimum rate based on the interest rate floor pricing. Therefore, applying an interest rate floor is visible in the derivatives and loan contracts. However, it does differ from interest rate floor swaps and fluctuations arising during it.

Thus, it is a contractual agreement between two parties. Often a borrower and a lender, where the lender agrees to pay the borrower if the reference interest rate falls below a predetermined minimum level known as the floor rate.

As per the rules, these rates cannot exceed the interest rate cap or fall below the interest rate floor. If it lowers anytime, the lender may lose the gain (cost of lending) on the contract. Thus, the interest rate floor agreements act as a protection to the lenders. They are usually purchased to safeguard their income from market fluctuations.

Besides, for many derivatives contracts, the interest rate floor swap refers to the floating rate that does not fall below a given level. Since there are premiums involved, it protects the investors from foreseen risks. Additionally, the floor rate, notional amount, compensation, and other details are negotiated and agreed upon based on the needs and preferences of the parties involved. Hence, the purpose of an interest rate floor swap is to manage interest rate risk. Thereby creating an interest rate collar or range within which the interest rate can fluctuate. It allows the parties to limit their exposure to interest rate movements beyond specific levels.

Examples

Let us look at the examples to comprehend the topic in the easiest way possible:

Example #1

Let’s say AMERCO Company based out of the US, obtains a variable rate loan from Bank of America for $500,000. The loan has a term of five years. However, the firm is concerned about the possibility of interest rates decreasing in the future and wants to protect against this risk.

Thus AMERCO Co. negotiates an interest rate floor agreement with the bank. Hence, they agree on the following terms:

- Notional amount: $500,000

- Floor rate: 3%

- Maturity: 5 years

Assuming that the reference interest rate, such as the prime rate, falls below 3% during the agreement term, the firm would receive payments from the bank to compensate for the difference. These payments help offset the impact of declining interest rates on the company’s borrowing costs.

For instance, if the reference interest rate drops to 2.5%, the firm would receive payments from the bank to compensate for the 0.5% difference between the floor rate of 3% and the lower reference rate of 2.5%.

Thus, by having these floor rates in place, the firm ensures that its borrowing costs will not fall below the specified floor rate of 3%. Therefore, this provides the firm with protection and stability against potential interest rate decreases.

Example #2

The Central Provident Fund (CPF) and Housing and Development Board (HDB) in a joint press statement on September 21, 2022 stated that the CPF members under 55 would continue to receive up to 5% interest on the first S$60,000 of their combined balances, with a maximum of S$20,000 coming from the Ordinary Account. Moreover, the Special, Medisave, and Retirement Account (SMRA) interest rate floor will continue at 4% until December 31, 2023, for one additional year.

On the first S$30,000 of their combined balances, CPF members aged 55 and over will get 6% interest yearly, with a maximum of S$20,000 coming from the Ordinary Account. The following S$30,000 will be paid to them at a rate of 5%.

On the other hand, the HDB Concessionary Interest Rate would stay at 2.6% through the end of the year, according to the press statement. Additionally, they said that the SMRA rates would be reviewed frequently and that CPF members would receive the higher floor rate or the pegged rate.

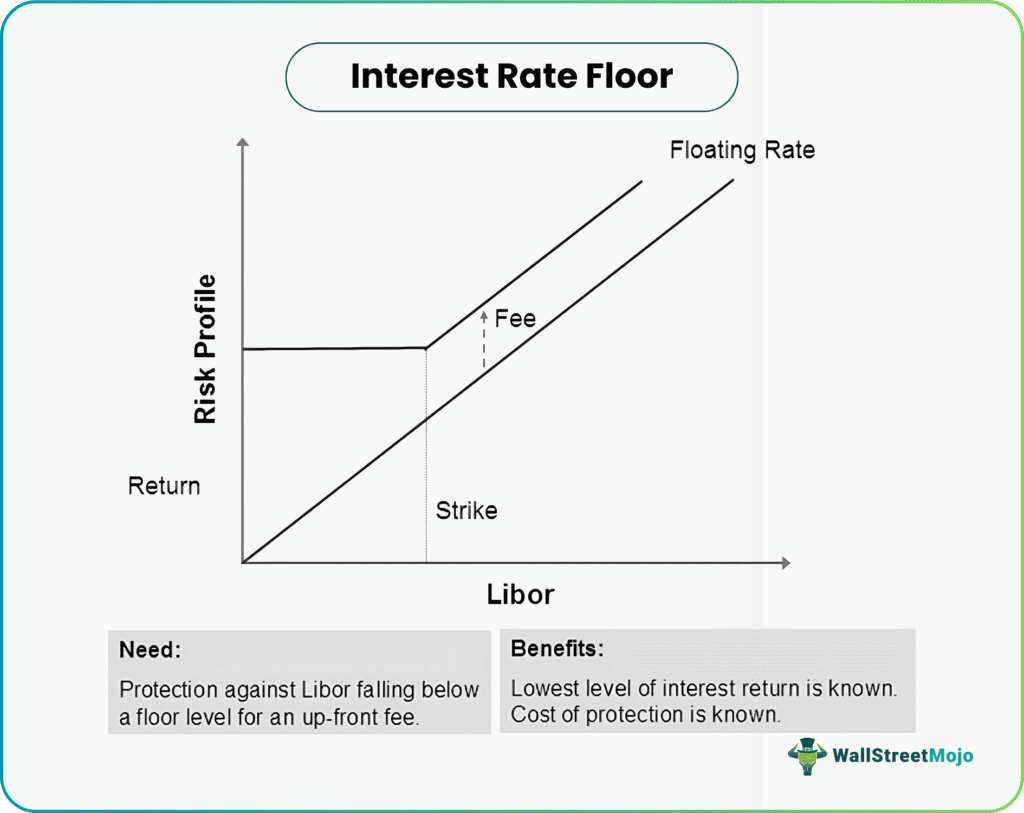

A graph will help to explain the concept with more clarity. As shown in the graph, the interest rate floor is protecting the interest rate, which is LIBOR in this case, from experiencing a free fall and leading to losses. Therefore, it is acting as a hedging instrument. Thus, even if the rate falls, the seller or the lender will be able to charge a minimum interest rate from the borrower. This is very useful in case the financial instrument has a floating rate system which fluctuates with the market. By using this concept, traders can gain clarity regarding their risk levels. This proves to be a form of insurance policy for lenders.

Advantages And Disadvantages

This rating system may benefit the issuer but has similar disadvantages. So, let us look at their pros and cons.

| Advantages | Disadvantages |

|---|---|

| It protects the lenders against uneven interest rate fluctuations. | Although it benefits the lenders, the customers or borrowers cannot enjoy the low-interest rates applicable to loan contracts. |

| They provide a way for investors to achieve better stability and financial management. | The borrowing costs may increase with the rising interest rate leading to a disadvantage for the borrower. |

| Hence, the risk associated with the contract reduces to a greater extent. | Implementing the floor system can sometimes be expensive compared to the cap. It involves legal complexities. |

| Plus, it ensures profitability with a minimum rate applicable. | Moreover, the floor system in the credit or debt market may affect the total demand and supply forces. |

| Those investors opting for a stable income can find it lucrative. | Additionally, such rates’ pricing strategy can be confusing and misleading. |

Interest Rate Floor And Cap

Although the interest rate floor and cap are almost similar, they have broad characteristics. So, let us look at their differences:

| Basis | Interest Rate Floor | Interest Rate Cap |

|---|---|---|

| Meaning | It refers to the minimum rate the lender cannot charge the borrower below. | The interest rate cap refers to the maximum ceiling for an interest rate. |

| Purpose | The primary purpose of the floor is to protect the lenders from falling rates. | Interest Rate Cap aims to provide ease to borrowers from rising interest rates. |

| Protection | Aims to reduce the burden on the lender. | These protect the borrowers. |

| Occurrence | Here, the floor system occurs mainly to provide security during the recession. | However, here the inflation causes a significant concern in implementing the interest rate cap. |

Frequently Asked Questions (FAQs)

1. What is the medium-term interest rate floor?

The medium-term interest rate floor refers to the interest rate applicable on products ranging from a few months to some years. Typically, the duration moves more than six months. The financial institutions verify the customer’s debt through a medium rate floor during low mortgage rates.

2. What is the interest rate floor to compute a loan?

Financial institutions can compute the interest rate for a loan. They can either follow simple interest or compound interest. However, other factors also matter during the calculation.

3. Can interest rate floors be customized?

Yes, the terms and conditions of these rates can be customized based on the parties’ agreement. Hence, this includes determining the floor rate, notional amount, maturity, and any specific provisions or adjustments.

Recommended Articles

This article has been a guide to what is an Interest Rate Floor. We compare it with the interest rate cap and explain its examples, advantages, and disadvantages. You may also find some useful articles here –