Part of our Banking Services and Operations guide

Mortgage Fraud Definition

Mortgage fraud is a willful misrepresentation or omission of facts such as an overstatement of an ability to repay the loan or any such material information, which leads the loan lenders to approve or relax the terms and conditions of the loan such as the interest rate or the repayment schedule. This fraud falls under criminal offense.

Mortgage fraud convictions on the rise before the 2007-2008 housing bubble financial crisis, and the FBI warned in its press release in late 2004 and early 2005. Post the crisis, the Fraud Enforcement and Recovery Act came into force in 2009 as an outcome of the market crash to prevent the same from happening again.

- Mortgage fraud involves intentionally misrepresenting or omitting facts, such as overstating the ability to repay the loan or withholding material information, leading lenders to approve or modify loan terms.

- The categories of mortgage fraud are fraud for profit and fraud for housing. Fraud for profit involves a scheme where the fraudster makes money through the fraud. In contrast, fraud for housing involves an individual misrepresenting their income or occupancy status.

- The types of mortgage fraud include occupancy fraud, income fraud, incomplete or non-disclosure of liabilities, and using loaned funds for purposes other than property purchase, shotgunning, and air loans.

Mortgage Fraud Explained

Mortgage fraud refers to the deliberate actions of an individual or an organization to misrepresent or fabricate facts to secure a mortgage loan. These mortgage fraud cases have plagued the insurance and loan industry more than most types of fraud.

The above definition aligns with the Federal Bureau of Investigation (FBI) view. It implies that a borrower is not conveying the whole truth about his capacity and intentions for the borrowed funds he sought. Such hidden information can impact the lender’s ability to decide on the approval of a loan or determine the loan terms. The prospective borrower is committing mortgage fraud.

The aim borrower gets accused because he is withholding information for his interest at the loss of the lender’s interest. In addition, if the borrower overstates his earning capacity, he might lead the lender to think that the borrower can better repay the same. Thus, the lender might approve his loan application when in fact, he should not.

It may also be the case that it might mislead the lender to think that the loan is less risky than it is and sanction the same at a lower interest rate or defer repayment to later dates than he would, had the complete information about the borrower.

Therefore, it is prudent to conduct a rigorous background check of the borrower and all the parties involved in the process, including the financial institutions, to minimize the possibility of fraud.

Categories

The majority of the mortgage fraud cases fall into two categories. One, for profit or gains through fraudulent means or, two, to secure funding for a house. Let us understand the intricate details of the concept through the discussion below.

- Fraud for Profit: This type of fraud is of greater interest to the FBI. It involves an institutional borrower with insider information or greater industry knowledge. It uses the same to dupe the lender and extort money from him without backing it with commensurate collateral.

- Fraud for Housing: In this, a retail borrower overstates his capacity to secure a housing loan that he cannot pay off.

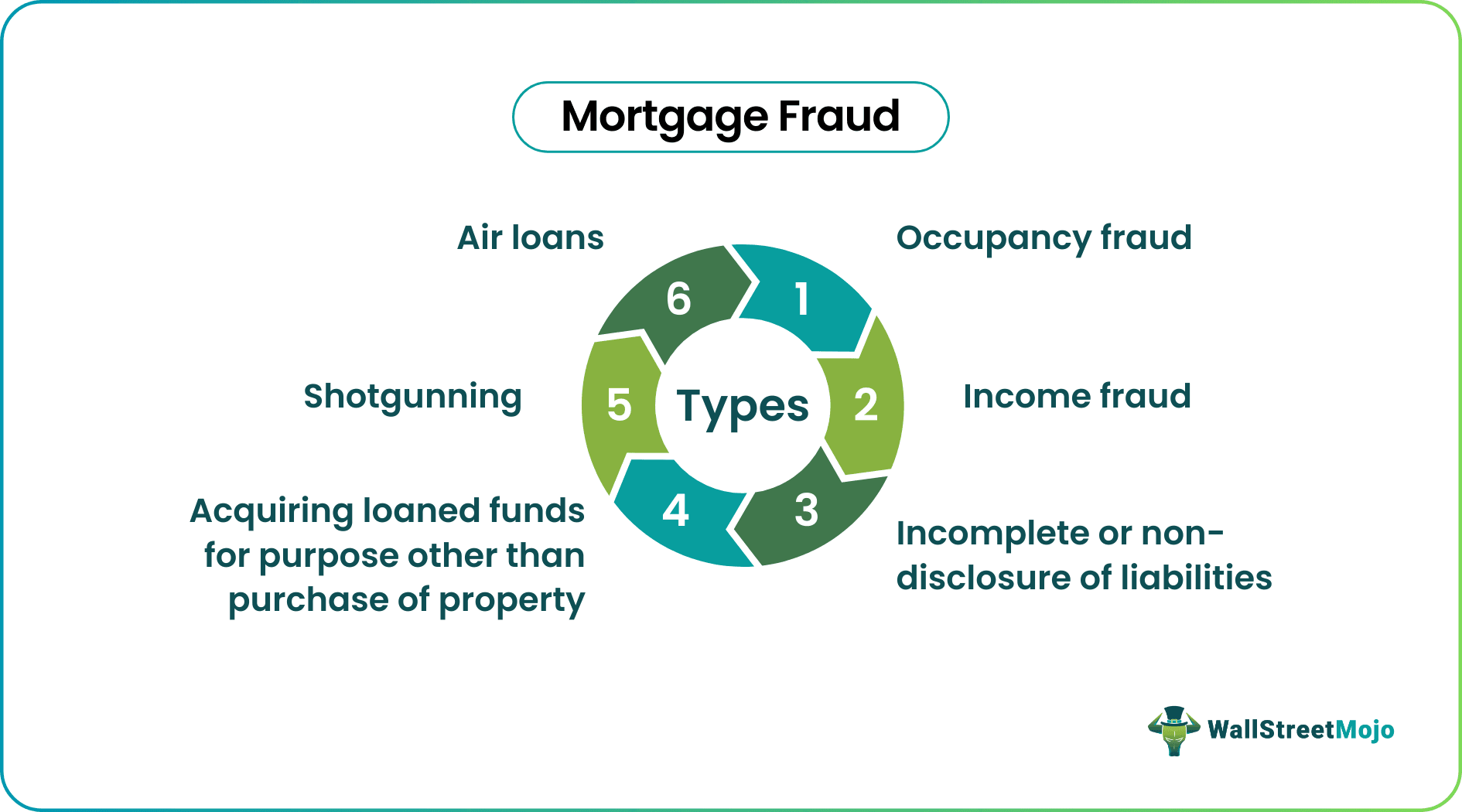

Types

The fraudulent activities that lead to mortgage fraud convictions come in different forms. However, the types below are factors that are closely considered, scrutinized, and placed impetus upon by both insurance and financial organizations. Let us understand the different types through the explanation below.

#1 – Occupancy Fraud

- Here, the borrower conveys to the lender that he needs the loan to purchase a property for his living purpose. However, the actual reason is to resell the same at a better price when such is available. Therefore, it is an investment rather than a necessity.

- In such cases, if the entire loan is not paid off and the title of ownership is passed on to the new buyer, there might be a possibility that he may not pay off the loan. Because of this reason, the loans for investment property attract higher interest rates. Therefore, the primary borrower has committed fraud by not mentioning the actual reason for borrowing the money.

#2 – Income Fraud

Here, the borrower conveys a higher income than his actual income. As a result, he may get a higher loan or a lower interest rate because a higher income means a better repaying capacity.

#3 – Incomplete or Non-Disclosure of Liabilities

Such is the case when the buyer does not give a complete picture of the liabilities that he is indebted by and secures a higher quantum of loaned funds or a lower interest rate due to a misrepresentation of the riskiness of the loan.

#4 – Acquiring Loaned Funds for Purpose other than Purchase of Property

- Under this type of fraud, the borrower overstates the value of the property he wishes to purchase from the loaned funds. Therefore, manages to acquire a greater amount of loan funds than necessary. The borrower then uses these funds for another purpose.

- It is fraudulent because the lender is exposed to a risk he is unaware of. Had he been informed, he might not have lent the funds or might have done so under different terms and conditions. At the time, this fraud was also known as appraisal fraud.

#5 – Shotgunning

Here several loans are taken out on the same property, each of almost the same value as the property itself. Therefore, the loaned amount becomes double or triple instead of the property’s actual value. That is a fraud because one might pay off only one of these loans by selling the property if the borrower defaults. Therefore, the loans taken after the first loan get lower priority and might not get repaid.

#6 – Air Loans

Air loans involve frauds conducted by a financial intermediary where they borrow funds for a property that does not exist. In such a case, these intermediaries falsify proof of such properties and borrow funds without providing any collateral. As a result, the lender is unaware of the sanctions of the loan and later faces the issue of not being able to recover the same by selling the collateral in case of a default because the collateral does not exist.

Examples

Let us understand the intricacies that leads to the filing of mortgage fraud cases with the help of a couple of examples. This will help us understand the concept in depth.

Example #1

ABC and XYZ were unable to secure a housing loan for over two years as their combined income was not sufficient for banks and other private financial organizations to sanction a loan to purchase a home.

They even tried persuading local lenders with exorbitant interest rates scared most people away in a desperate attempt at securing a loan to finance their dream home.

Out of frustration and desperation, they fabricated documents relating to their incomes, wrote off most of their liabilities on paper, and even faked their citizenship.

As a result, they secured the loan to purchase a 3BHK flat in New Jersey which was well and truly above their affordability. When they were unable to pay their EMIs on time for the third consecutive month, the second background check from their bank uncovered the truth and a case was filed. The court delivered mortgage fraud convictions against both ABC and XYZ.

Example #2

On November 4th, 2019, the U.S. Department of Justice sentenced Manuel Herrera and Moctezuma Tovar for wire fraud and mortgage fraud along with several other defendants. The defendants, who worked for Delta Homes & Lending Inc., created false loan documents and homebuyers to secure loaned funds. They overstated the incomes, liabilities, employment, and citizenship of these home buyers to secure funds and provided them money so that their balance sheet looked better than it was. Once they secured the funds in the name of these homebuyers, they returned them to Herrera and Tovar and their accomplices.

In this process, the lenders lost $4 million. The final decision is pending, but the penalty can extend up to 20 years of imprisonment and a $250,000 fine per defendant.

Indications

The following are potential red flags that should be taken care of and investigated by the lenders to prevent mortgage fraud cases.

- The same phone number is mentioned for the borrower and the employer in the loan application. That could be the case of employment fraud where the borrower might be misrepresenting his employment.

- The income specified is above the industry standards in the particular field mentioned on the application.

- The assets stated seem higher than that of an average individual in the profession indicated on the loan application.

- Background verification took less than usual time to proceed with the loan application to the next step of the evaluation process.

How to Prevent?

Ever since the housing bubble burst in the United States, banks and other financial organizations have been vary of such cases and are up to date about mortgage fraud convictions to black list such individuals or organizations. However, to understand the complete details of the concept, it is important for us to understand how to prevent such fraud. Let us understand them through the points below.

- Conducting thorough due diligence is one of the most important components of the loan sanction process. If it is shown properly, mortgage fraud is less likely to occur. However, it does not eliminate this risk because a fraudster may develop a new technique for conducting a fraudulent activity with a lender who might not have prior experience.

- A deeper investigation in case of the appearance of any of the above-mentioned red flags is a prudent way of ensuring no mortgage fraud.

- Third-party evaluation and appraisal of the borrower and the subject property can lead to an unbiased opinion based on an informed decision regarding loan approval.

Frequently Asked Questions (FAQs)

1. What is mortgage fraud vs. credit fraud?

Mortgage fraud involves misrepresenting or withholding information to obtain a mortgage loan. Credit fraud involves using someone else’s identity to apply for credit or opening credit accounts without intending to pay them back.

2. What role do mortgage brokers play in preventing mortgage fraud?

Mortgage brokers are responsible for verifying the accuracy of information borrowers provide, including income and employment history. They must also ensure the borrower can afford the loan they are applying for. In addition, mortgage brokers should be trained to recognize red flags of potential fraud, such as falsified documentation or inflated appraisals.

3. Can mortgage fraud affect my credit score?

Yes, mortgage fraud can affect your credit score. If you default on a fraudulent mortgage loan, your credit score will be negatively impacted, making it harder for you to obtain credit in the future. In addition, if your personal information was used in the fraud, it may take time and effort to clear your credit history and restore your credit score.

Recommended Articles

This article is a guide to Mortgage Fraud and its definition. Here, we discuss its types, categories, and indications along with examples & how to prevent it. You can learn more about it from the following articles: –