What Is A Mortgage Recast?

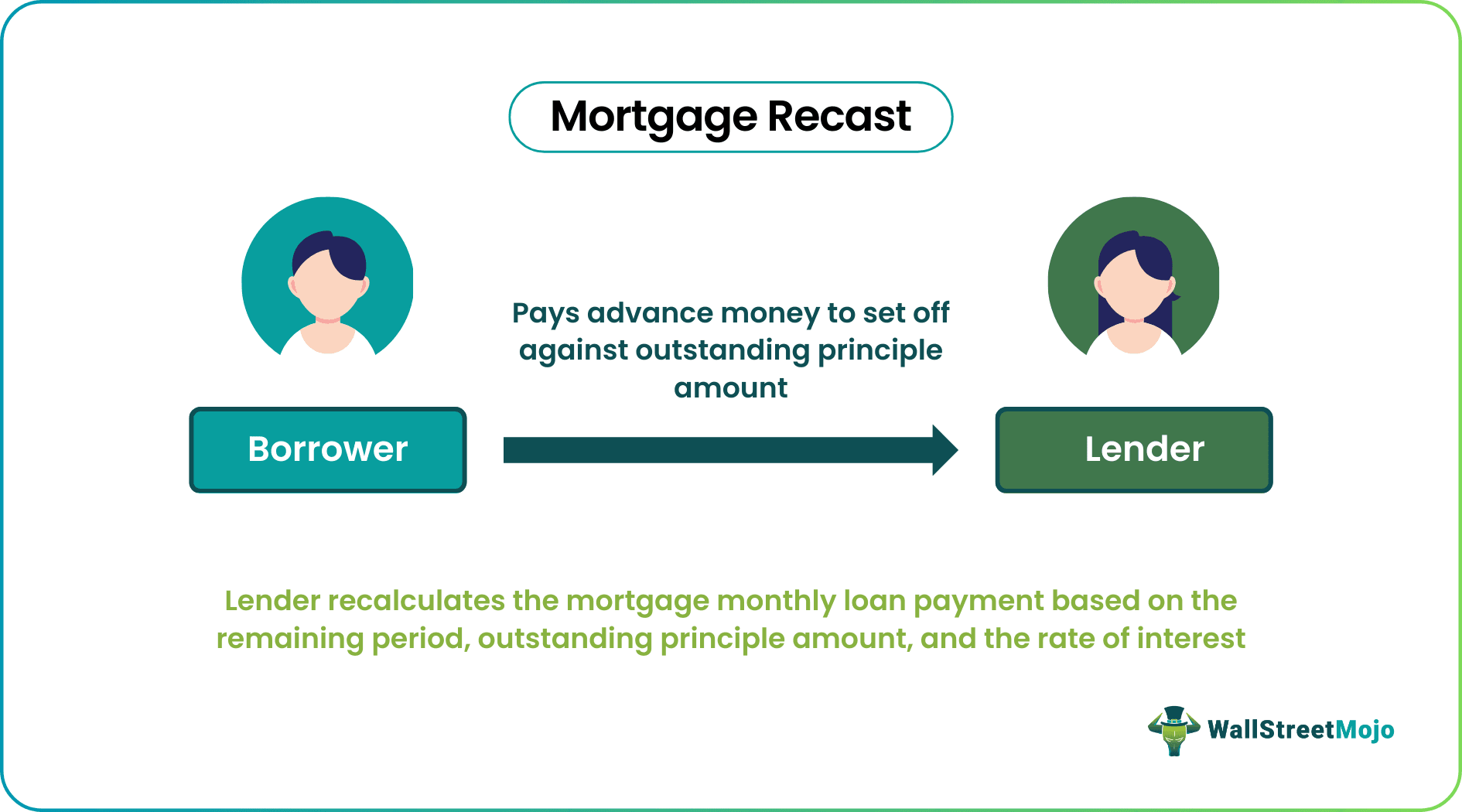

Mortgage Recast is when the borrower prepays either some or the full amount of outstanding principal resulting in a reduced loan balance, and therefore the financial institution recalculates the mortgage monthly loan payments based on the remaining period, outstanding principal amount, and the rate of interest.

The above discussion clearly showed that a mortgage recasting is different from refinancing due to the above-mentioned reasons. Also, mortgage recasting has provided an easy way for the borrowers in order to reduce the interest burden over a period of time by keeping the maturity period the same and to lower the principal repayment every month after providing a lump sum amount of principal payment in advance to the lender.

How Does Mortgage Recasting Work?

The mortgage recasting works on the basic principle of finance. There are several factors because of which interest is charged by the lender, which includes time factor as well as a risk factor. The concept of the time value of money work, taking into consideration the different elements such as rate of interest, time period, and outstanding amount of borrowing, etc. Normally there are specific amortization schedules for loan repayment, which includes equal monthly payment or payment of principal and interest as per predefined rate.

When the borrower has a large amount of money then, such money can be transferred to the lender in the form of the mortgage and calculate mortgage recast to reduce the outstanding balance of the loan as well as to reduce the interest burden and monthly principal burden of such loan.

Thus the borrower pays advance money to set off against the outstanding principal amount, and the lender recalculates the outstanding amount with the remaining period of maturity and rate of interest, which provides the re-casted mortgage amount.

Also, the total amount of interest payable by the borrower to the lender after mortgage recasting will obviously be lower as compared to the amount that the borrower would have paid without doing so.

This is because of the time value of the money factor present in the interest calculation of the principal outstanding.

However, if the principal repayment is higher than the outstanding amount payable on a specific installment when we and calculate mortgage recast, the balance amount outstanding shall be recalculated using the finance concepts taking into account the present value of the balance loan amount discounted at the rate of interest.

Calculations

Every borrower does not allow a loan recasting. Thus the first thing to be assured is that the borrower allows the same as per the contract entered. Further following conditions must be satisfied:

- The minimum principal reduction standards must be fulfilled: where the borrower allows recasting, there are specific norms related to minimum amount repayment of principal, which needs to be satisfied as a first condition.

- Recasting fees are to be paid by the borrower as per the norms of financial institutions.

Types

Below mentioned are the various types of such mortgage recast letter sample that one should have knowledge about so as to select the right kind that suits one’s financial condition, objective and risk taking capacity.

- As mentioned earlier, only those mortgages in which the specific conditions are allowing the recasting is there can only be recast. Such mortgages are associated with a negatively amortized loan, which has a payment structure such that allows schedule repayment of an amount less than the loan’s interest charges.

- Negatively amortized mortgages are also termed as payment option adjustable-rate mortgages or Option ARM.

- Further, no government-backed loan can be re-casted, and hence, Jumbo CDs, USDA, VA loan, etc. cannot be recast.

Examples

Given below is the calculation example to recast your mortgage.

| Particulars | Amount |

|---|---|

| Current Principal Balance | $1,125,000.00 |

| Annual Interest Rate | 5.00% |

| Current Monthly Principal and Interest Payments | $100,000.00 |

| Interest portion left | $29,671.58 |

| Lump-Sum reduction in principal | $500,000.00 |

| Recasting Fee | $25,000.00 |

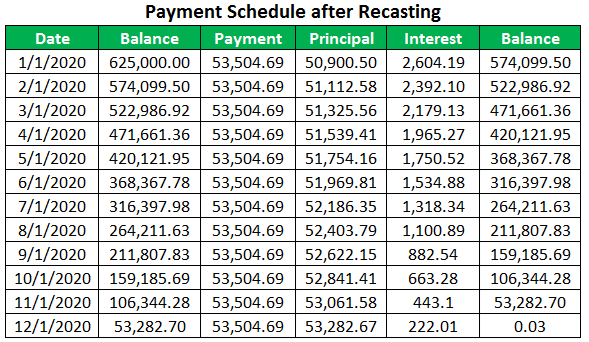

The number of remaining payments is 12. Calculate the recast mortgage savings.

Solution:

The number of remaining payments is 12. Now, we will calculate the recast loan balance first.

- Recast loan balance = Current principal balance – Lump-sum reduction in principal

- = $1,125,000 – $500,000

- = $625,000

Calculation of the remaining installment amount:

- Installment = Principal amount / Annuity factor @5% for 12 months

- = $625,000 / 11.68122

- = $53,504.69

| Recast Comparison | Payment | Interest |

|---|---|---|

| Existing Terms: | $100,000.00 | $29,671.58 |

| Recast Terms: | $53,504.69 | $42,056.11 |

| Recast Savings: | $46,495.31 | -$12,384.53 |

Pros And Cons

Given below are some of the pros and cons of mortgage recasting.

Pros

- The overall interest paid on the borrowings is much lower as compared to what amount of interest payable if the recasting of mortgage is not done. Hence, it lowers the monthly payment Burden

- The average interest rate payable by the borrower gets in line with the expected rate of interest payable.

- Re-qualifying for a new loan becomes a tedious job, and hence the process of mortgage recasting removes the administrative works of obtaining a new loan.

Cons

- The process of mortgage recasting doesn’t shortage the time period the term of the loan; hence unlike refinancing, it doesn’t reduce the loan period.

- Though the interest payments get reduced due to recasting, the drawback is that it makes more of your money get types up in the mortgage, and hence there are chances of liquidity crunch.

- Recasting involves charges like fees, administrative charges, etc., and hence the financing fees burden increases.

It is always important to understand the concepts of mortgage recast letter sample, terms and conditions thoroughly so that one can decide whether to go for the process or not and how much beneficial it will be in future. This will help in taking informed financial decisions.

Mortgage Recasting Vs Refinancing

- Where the borrower makes a sizable amount of lump-sum loan repayment and fulfills the predefined conditions, then such repayment can be termed as mortgage recasting while, on the other hand, loan refinancing happens when the borrower turns the existing loan into a new loan which different terms of the loan being favorable terms for the borrower. Thus there is a thin line that defines the difference between mortgage recasting and refinancing.

- Under the terms of the former, the borrower makes lump-sum payments making himself or herself ahead from the stated schedule of repayment, and the lender rescheduled the principal balance amount outstanding being the amount lower in terms of annual interest payment, number of years of repayment, and annual repayment of principle, while in the later, transfer of loan takes place where the new lender has been transferred the loan from the old lender and the further repayment is to be done to the new lender only as per the new terms of the loan.

Mortgage Recast Vs Principal Payment

Both the above concepts deal with the repayment procedures of mortgage loan balance. But there are some differences between them as follows:

- In case of the former, the borrower repays a lumpsum amount to the lender to reduce the remaining loan amount, which is not the case with the latter.

- In case of the former, the monthly payments are recalculated and fixed depending on the remaining loan balance, term and rate of interest. But in case of the latter, the monthly repayment amount remains the same and there is no recalculation.

- The former directly reduces the monthly repayment amount leading to a huge reduction in cash outflow every month. However, for the latter, since the monthly payments do not change, the cash outflow remains the same.

- The former may involve some terms and conditions that the lender may set for the borrower leading to complexity in calculation. But the latter is a straight and simple process with no extra terms and conditions apart from the ones related to normal lending and borrowing.

It is upto the borrower whether they will go with the former or the latter, by keeping in mind their own financial strength, objectives of borrowing, time period, etc. But the former is more advantageous since it shortens the term and reduces the monthly payments.

Recommended Articles

This has been a guide to what is Mortgage Recast. We explain its pros & cons, differences with principal payments & refinancing, example & calculation. You can learn more from the following articles –