Part of our Income Statement guide

What Are Extraordinary Items?

Extraordinary Items refer to those events considered unusual by the company as they are infrequent. The gains or losses arising from these items are disclosed separately in the company’s financial statement during the period such items came into existence.

Such items may affect the financial performance of the business in a significant manner. However, they may be treated in the statements differently, and used depending on the type of accounting standards that are followed. They are highly unusual or totally unrelated to the normal business operations.

Extraordinary Items Explained

The extraordinary items are a financial concept used in Generally Accepted Accounting Principles(GAAP) in the US before issuing the Accounting Standards Update(ASU) No- 2015-1. This rule came into effect after December 15, 2015 and it abolished this concept from GAAP.

Due to the above reason, the corporates are no longer required to show or report the items in their financial statements. However in extraordinary items accounting, some items that were previously included under the extraordinary item category and reported in the financial statements are losses due to any kind of natural disaster or calamity, losses due to any political problems in the country, asset expropriation by the government of the country, etc.

Let us have a look at the ZTE Annual Report. We note that the Net profit Attributable to Shareholders is RMB 2,633 million. However, when we remove the extraordinary items from the Income Statement, the Net Profit gets reduced to RMB 2,072 million.

Thus, from the above explanation, we note that since this financial concept is no longer in practice in the industry, the companies do not include them in the financial statements as extraordinary item. Instead, asper the current standards of accounting, any significant event or transaction is included in the statements as a normal income or loss incurred from continuing operations. The extraordinary items accounting are seperately reported so that the users of the financial statements can get clarity and all transactions remain transparent.

Features

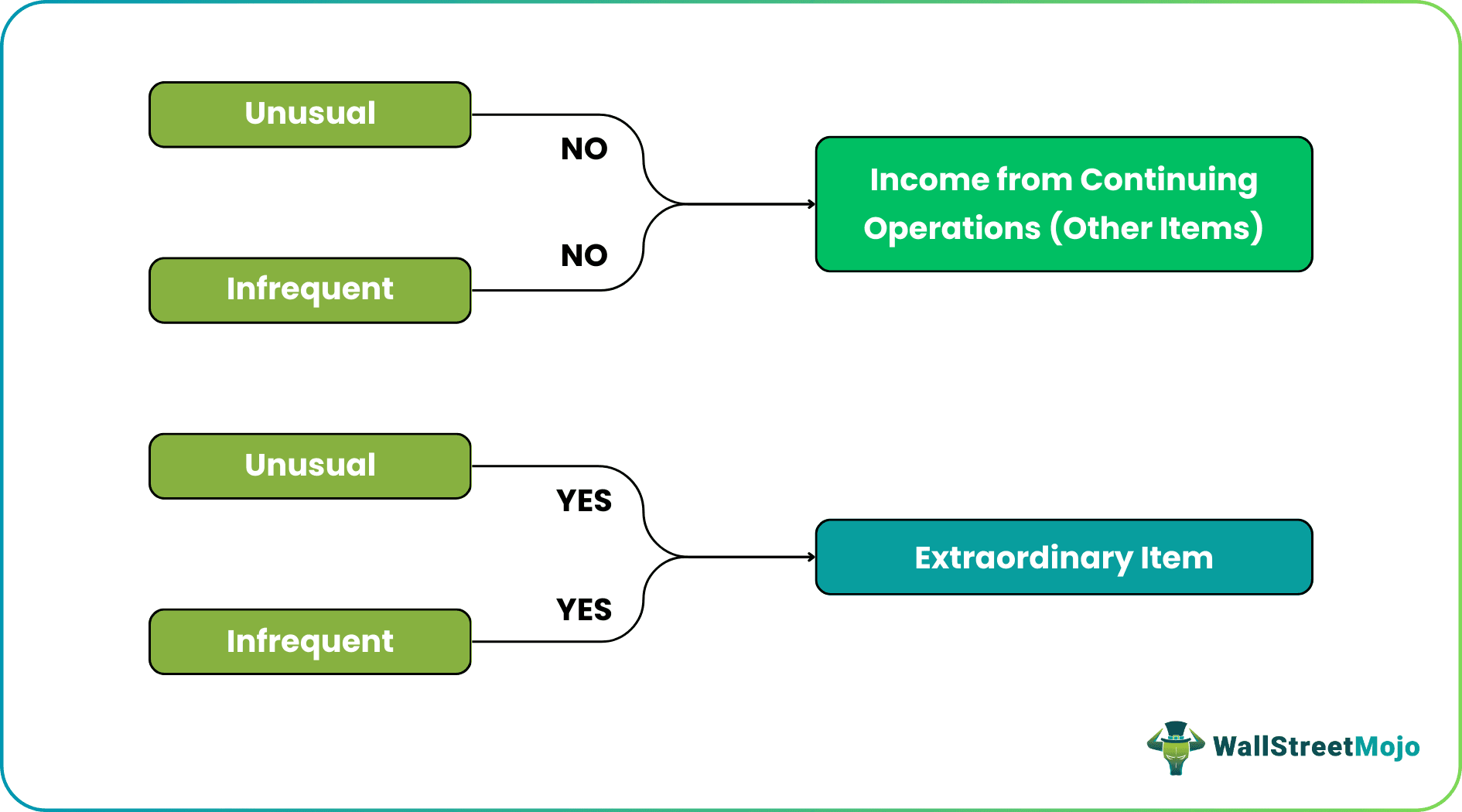

The income statement extraordinary items refer to gains and losses from specific business transactions, which are unusual and rare from the normal course of business. In other words, they pertain to transactions that do not form a part of the company’s day-to-day business operations.

Some of the critical aspects are:

Materiality

Transactions above the material limit of an organization will classify under extraordinary items of the company. Materiality is subjective to the size of the balance sheet and the industry to which the company belongs.

- Example 1: In the case of XYZ Co., if it is involved in the scrap sale of a business unit in Chicago, which has led to a business gain of $ 10,000 will not be material enough to be classified as an extraordinary gain. It is because the value of one car will be more than $ 10,000, which is not material, keeping in mind that the entire revenue of XYZ Co. is $ 100 billion.

- Example 2: A small-time retailer who sells hotdogs outside Central Park earns royalty amounting to $ 5,000 for selling his hotdog recipe to a chain store will classify this transaction as an extraordinary item as it is above the materiality threshold. Why is it material in this case – because the annual profit of the retailer is somewhere around $ 5,000 itself.

To check whether the transaction is material for reporting it as an extraordinary item, the following three levels of materiality should be checked:

- A particular income statement extraordinary items concerns the total income reported for that period.

- A particular extraordinary item is material concerning the annual income of the last 4-5 years taken into account.

- A particular extraordinary item is material concerning any other criteria defined by the company policy, e.g., a holding company (parent company) may require its subsidiary companies to report all extraordinary items above a certain threshold.

Rare / Unusual transactions

They will be rare in nature. They are transactions that do not occur on a day-to-day basis. As we saw in the case of XYZ Co., discontinuing the car manufacturing business is something that does not happen regularly. It will happen once in 5 years or ten years or, at times, never in the company’s lifetime.

The vital point is that not all rare/unusual/non-recurring transactions are necessarily defined as extraordinary items. There can be non-recurring transactions but, at the same time, are not extraordinary.

- Example 1: XYZ Co. feels that the current capacity of manufacturing buses is limited, and there is a lot of scope in the market for increasing revenue. Keeping this in mind, the management has approved investing in a new plant to increase production capacity. It is a non-recurring transaction; however, the same can be taken as an increase in capital assets rather than classified as a tremendous loss.

- Example 2: Continuing with the very first example of XYZ Co. Where they intend to discontinue their car manufacturing business is a non-recurring transaction and qualifies as an extraordinary gain.

Video Explanation of Extraordinary Items

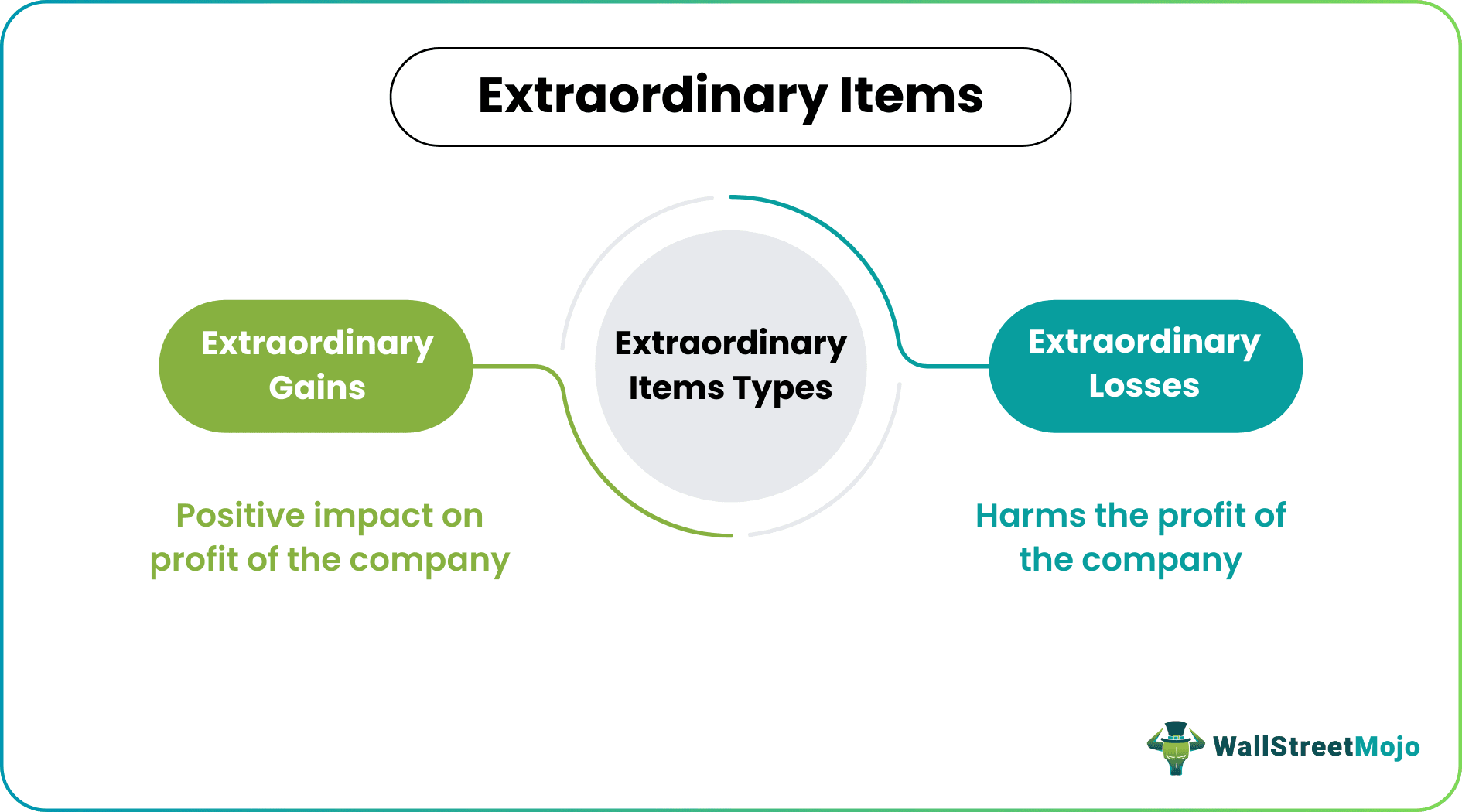

Types

They can be bifurcated into extraordinary gains and extraordinary losses. Losses harm the profit of the company, whereas extraordinary gains have a positive impact on the profit of the company.

It is essential to understand the fact that whether the event or the transaction falls under the category of list of extraordinary items or not is subjective. It requires a thorough and careful analysis of the event and the circumstances that lead to it. Since, as mentioned earlier, the rule of reporting has changed and now these items are shown as a regular financial reporting process, additional information is needed to let the users know and catagorize them as extraordinary or not.

Examples

Some examples of both gains and losses due to such events will help in understanding the concept. Let us go through list of extraordinary items as given below:

Example of extraordinary gains

- Gain on account of sale of discontinued business segments

- Gain from a recent announcement from the government announcing previous subsidies to be sanctioned now

Examples of extraordinary losses

- Loss on account of uncontrollable natural calamities such as earthquakes, floods, hailstorms, etc.;

- Loss on sale of discontinued business segments

- Loss on account of losing a legal case which has led to colossal tax penalties

- Loss on account of a long workers strike which has disrupted business for more than a month

The above examples are generic and can vary on a case-to-case basis. For instance, loss on account of the flood cannot be claimed as an extraordinary loss in the case of businesses in areas declared flood-prone areas. It is due to the assumption that businesses are aware of the climatic conditions in the area and are still willing to take the risk of doing business in that area. Hence, this is a part of the business risk which the organization must have already taken into account.

Another example that we can consider is the case of a private equity firm that has its core business investing in startups. In this case, gain or loss from selling a business is normal and not irregular or rare. Therefore, it cannot claim gain because of selling long-term investments as extraordinary gains.

Also, the important point is that there is confusion regarding treating the write-off/write-back of various assets as a great loss. In this context, the write-off of the following business assets is in the normal course of business. A company should not treat these as an extraordinary items:

- Inventories

- Accounts receivable

- Amortization of intangible assets

- Loss or gain on account of foreign currency exchange and other transactions

- Sale of fixed assets

It is because write-off/write-down of the these current and fixed assets are considered very normal for any given business, and the following explanation should suffice for not treating it as an extraordinary item:

- Inventory lying in the warehouse will get old and obsolete. It happens with almost all businesses and is only part of operational loss.

- A certain part of accounts receivable expects to turn into bad debts in the normal course of business, and it is an operational loss.

- Intangible assets should be amortized yearly, just as tangible fixed assets depreciate yearly.

- Foreign currency will fluctuate daily. If there is a business requirement to enter into foreign currency transactions, the gain or loss from these transactions is considered to be normal.

- Buying and selling of fixed assets is an essential part of the business. Even if these transactions are rare, businesses require them from the operational point of view. Any profit earned or loss incurred from the sale of fixed assets should only be treated as part of operational income/expense.

Accounting

It is necessary to clearly understand the method of accounting of these type of assets as extraordinary items in financial statements. There has been a significant change in this field since January 2015, as detailed below. Let us study the same.

(Before January 2015)

All extraordinary items are to be presented separately in the financial statements. Presenting it separately means that the gain or loss from extraordinary items should be segregated from the profit/loss from ordinary operations and shown as a separate line item in the income statement after considering the tax effect.

The company should also disclose the applicable taxes on these extraordinary items separately, and along with it, they should also disclose earnings per share for such items.

The following is the Income Statement of XYZ Co. to show the presence of extraordinary items:

Income Statement of XYZ Co.

| Particulars | Amount | Amount |

|---|---|---|

| Net Sales (Revenue) | $ 1,00,000 | |

| Less: Cost of goods sold | ($ 55,000) | |

| Gross Profit | $ 45,000 | |

| Other operating income | $ 10,000 | |

| Operating expenses | ||

| a) Selling & advertisement expenses | $ 2,000 | |

| b) Administrative expenses | $ 2,500 | |

| c) Auditor’s remuneration | $ 2,000 | |

| d) Other expenses | $ 1,000 | ($ 7,500) |

| Operating income | $ 47,500 | |

| Other income (classified as non-operating such as interest income) | $ 500 | |

| Other expense (classified as non-operating such as financial cost) | ($ 2,000) | |

| Net income / (loss) from operations | $ 46,000 | |

| Less: Corporate Tax @ 10% | ($ 4,600) | |

| Profit from operations after tax (A) | $ 41,400 | |

| Extraordinary items | ||

| a) Loss on account of a hail storm | ($ 25,000) | |

| b) Gain on account of sale of the business segment | $ 15,000 | |

| Loss from extraordinary items | ($ 10,000) | |

| Savings on tax @ 10% | $ 1,000 | |

| Net loss from extraordinary items (B) | ($ 9,000) | |

| Net Income | $ 32,400 | |

| Earnings per share from operating income (Assumption – company has issued 1000 equity shares) | $ 41.4 | |

| Loss per share on account of extraordinary items | $ 9.0 | |

| Net earnings per share | $ 32.4 |

Why is the above presentation necessary? It is to give a true picture to the various users of the financial statement.

Elimination (After January 2015)

In January 2015, FASB issued an update to Extraordinary items eliminating the need to provide Extraordinary Items in the income statement. Eliminating this concept of extraordinary items in financial statements will save time and reduce costs for preparers because they will not have to assess whether a particular event or transaction event is extraordinary.

source: fasb.org

It was primarily argued that users find information about unusual or infrequent events and transactions useful. However, they do not find the extraordinary item classification and presentation necessary to identify those events and transactions. Others thought that it is extremely rare in current practice for a transaction or event to meet the requirements to be presented as an extraordinary item.

Extraordinary Items Vs Exceptional Items

Both the above terms are used to describe some special events or transactions in the company operations that are mentioned in the financial statements, which affect the performance and profitability. However, the treatment of both the concepts has some differences as per the accounting standards followed in the organization.

- The former refers to transactions and events that occur in an unusual manner or very less frequent, whereas the latter refers to transactions that may be infrequent but not extraordinary. They are within the scope of the business.

- The former refers to transaction that are unusual in nature, which is not the case with the latter. Exceptional items arise from ordinary business activities or core operations.

- Some examples of the former include loss due to natural calamity or sale of business assets by the government, etc but the examples of the latter include cost or restructuring or sale of non-core assets, writing down of some company assets, etc.

It is to be noted that both are disclosed in the financial statements for users to be aware of the same.

Recommended Articles

This article has been a guide to what are Extraordinary Items. We explain them with examples, accounting, differences with exceptional items, types & features. You may learn more about financing from the following articles –