What Is Inventory Write-Down

Inventory write-down essentially means reducing inventory value due to economic or valuation reasons. When the Inventory’s value reduces for any reason, the management has to devalue such Inventory and reduce its reported value from the Balance Sheet.

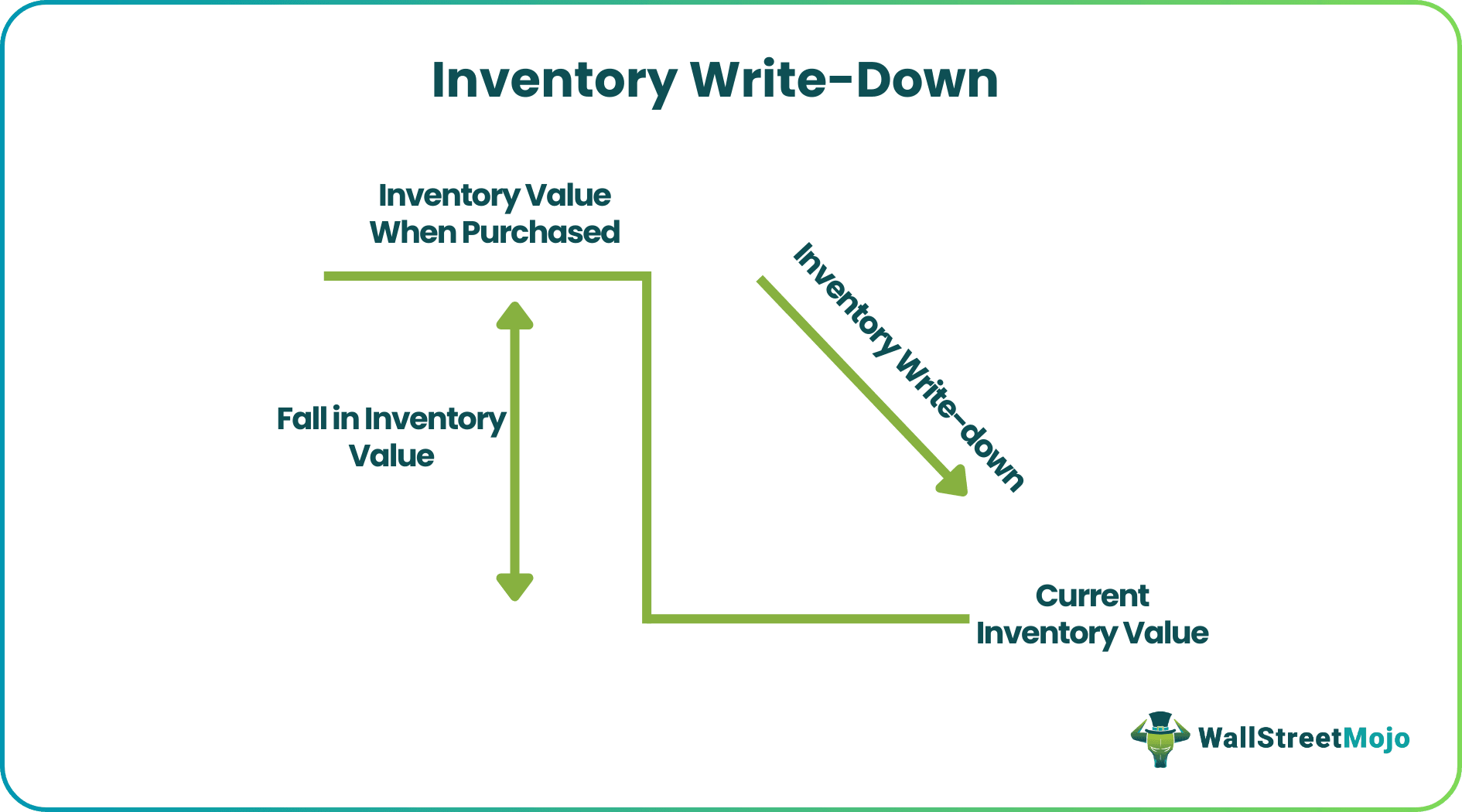

Inventory is materials owned by any business to be sold for revenue or useful for converting into final goods to be sold for revenue. Inventory may become obsolete or become less in value; at that time, the management has to write down the value of the Inventory. Therefore, the management has to compare the difference between the actual value of the Inventory vs. the original value of the Inventory when it was purchased initially. The difference between the two will be transferred to the Inventory to write down the account.

- A write-down of inventory means to lower the value of the inventory for financial or valuational reasons. The management must devalue such Inventory and lower its reported value from the balance sheet when the value of the Inventory decreases for whatever reason.

- Inventory is any material that a business owns and intends to sell for profit, or that can be used to create finished goods that will be sold for profit. Inventory may get dated or lose value over time, in which case the management will need to reduce the value of the stock.

- Inventory write-downs are a type of expense that will lower net profits in a given fiscal year. Any products damaged during manufacture, during transit from one location to another that is stolen, used as trials, or samples can also impact write-down inventory during the fiscal year.

Inventory Write-Down Explained

We use Inventory Write-down in the condition where the value of the Inventory reduces because the value has fallen because of the market or other economic reasons. Thus, there is a loss on inventory write-down. It is the opposite of an Inventory write-up where the value of the Inventory increases from its book value. A write down and write off are entirely different terms from accounting. We use a write-down when the value has decreased from its book value, but a write off means the value of the Inventory has become zero.

During quarterly or annual inventory valuation, the management has to put the fair value of Inventory in the books. Inventory has to be appropriately valued as per accounting methods and according to market valuation as well. Sometimes the inventory value increases, and sometimes we have to write down the value of the Inventory, which is called inventory write-down accounting. It also depends on the physical structure of the Inventory.

For the same lot of Inventory, the management may write off, do inventory write-down accounting, or sometimes write up the valuation of the Inventory.

How To Record?

To record the Inventory write-down in the books, we need to reduce the Inventory by creating a contra inventory account. Let’s understand in the following manner-

- First, the management has to understand the effect and also the value of the inventory write-down as these decisions will affect the process of the accounting treatment for Inventory write down.

- Once the management determines the value of the Inventory, which has to be written down, they need to decide whether that value is relatively small or large for the management. This decision will change from company to company.

- It is the process of reducing the value of the Inventory to keep the fact in the mind that the same part of the Inventory is estimated to be valued as worthless, which is showing in the books as the inventory write down entry.

- A certain amount of inventory write-down will be recorded as an expense for that particular period. Therefore, there is a loss on inventory write down this process is done at one time, unlike depreciation, which is recorded for more than one period.

Accounting Journal Entries

→ Explore all 30 Journal Entries articles

Let us look at the inventory write down entry. If the quantity of inventory that will be written down is very small, the the entry should be :

Cost Of Goods Sold A/c Dr.

To Inventory Account.

However, if the quantity of inventory that will be written down is quite large, the the entry should be:

Inventory Write-Down A/c Dr.

To Inventory Account.

Example

Let us take an example, there is a product that costs $100, but due to weak economic conditions, the cost of the product reduced by 50%. So, the value of the Inventory has gone down or has only scrap value. Thus, the management will record this difference in the books, which is called Inventory write down.

There are two ways of recording this as per the below example,

#1 – Journal Entries when Inventory Write-down is Small and Note Significant

#1 – Journal Entries when Inventory Write-down is Significantly high

The management should be aware of this part of Inventory management, as this affects the business in many ways. Recoding the true value of the Inventory in the accounts will provide the right picture of the business.

We should not record the value of this write-down in a future period. It should be recorded in a particular period when it was calculated.

Effect On Financial Statements

Inventory write-down is an expense in nature which will reduce the net income in a particular financial year. During the fiscal year, any damaged goods in production or damage during delivery from one place to another, goods stolen or used as trials and samples can also affect write-down inventory.

The effect of the inventory write-down can be summarized as per below,

- It reduces the allowance for inventory write down, which is recorded as expenses in the Profit & Loss Account, which reduces the net income for any particular financial year.

- If any business uses cash accounting, then the management write-down the value of the Inventory whenever problems occur, but in the case of accrual accounting, the management may choose to make an inventory reserve account , which is an allowance for inventory write down cover future losses because of inventory valuation changes.

- It also affects the COGS for any particular period. Let’s understand from the below-mentioned formula, COST OF GOODS SOLD = OPENING INVENTORY + PURCHASES – CLOSING INVENTORY. When we use this write-down, it increases the Cost of Goods Sold (COGS) for any particular period, because the management will not be able to receive payment of the said goods, which reduces the net income and taxable income as well. The value of the Inventory, which is written down, will not make any money for the business.

- It has a significant impact on any business’s net profit or balance sheet, as changes in the value of any inventory or assets will affect the profitability of the business.

Inventory Write-Down Vs Inventory Write-Off

Inventory write down reduce the asset value in the books whereas, write-off make the asset value zero. Let us look at the basic differences between them.

| Inventory Write-Down | Inventory Write-Off |

|---|---|

| It reduces the asset’s value in books of accounts. | It makes the current and future asset value zero. |

| The actual asset value does not change. | The actual asset value changes. |

| It is done for accounting and tax purpose. | It is done because the asset is no longer worth using. |

| It can be repeated in the business. | It is a one time business event. |

Frequently Asked Questions (FAQs)

What distinguishes an inventory write-off from a write-down of inventory?

A write-off occurs when an asset loses its value and must be completely deleted from accounting records. In contrast, an inventory write-down occurs when an asset’s value depreciates but retains some value.

When an inventory write-down is necessary, what do we do?

An accounting procedure that documents an inventory value decline is known as an inventory write-down. It is necessary when the market value of the inventory falls below its balance sheet book value. The write-down will lower the inventory’s balance sheet value and result in a cost on the income statement.

How can inventory write-downs be minimised?

The right amount of inventory can be ordered to reduce inventory. Order just the right amount of stock. Consider how much inventory the company has previously sold and written down before placing an order. Then consider any modifications that might have occurred that will affect upcoming sales.

Recommended Articles

This article has been a guide to what is Inventory Write-Down. We explain the journal entries and difference with inventory write-off, along with examples. You may learn more about accounting from the following articles –