Table Of Contents

What Is A Non-Cash Expense?

Non-cash expenses are expenses that are not related to cash. Even if they’re reported in the income statement, they have nothing to do with cash payments.

The most common non-cash expense is depreciation. If you have gone through a company's financial statement, you would see that the depreciation is reported, but actually, there’s no cash payment.

For example, we can say that Tiny House Builders Inc. buys new equipment. They see that they need to charge $10,000 for depreciation. If they need to report the depreciation for the next ten years, they will report the depreciation for the equipment for the next ten years. But actually, there would be no cash payment.

New to accounting? - No Problem. Do have a look at these basics of accounting tutorials.

Table of contents

Why Do Non-Cash Expenses Need to be Recorded?

As per the accrual accounting, the items must be recorded whenever the transaction happens.

For example, when the sales are initiated, the sales should be recorded in the income statement irrespective of the money received. On the other hand, in cash accounting, the sales would be recorded only when the cash is being received.

And for the same reason, we need to record non-cash expenses even when the company doesn't pay anything in cash.

Non Cash Expense Video Explanation

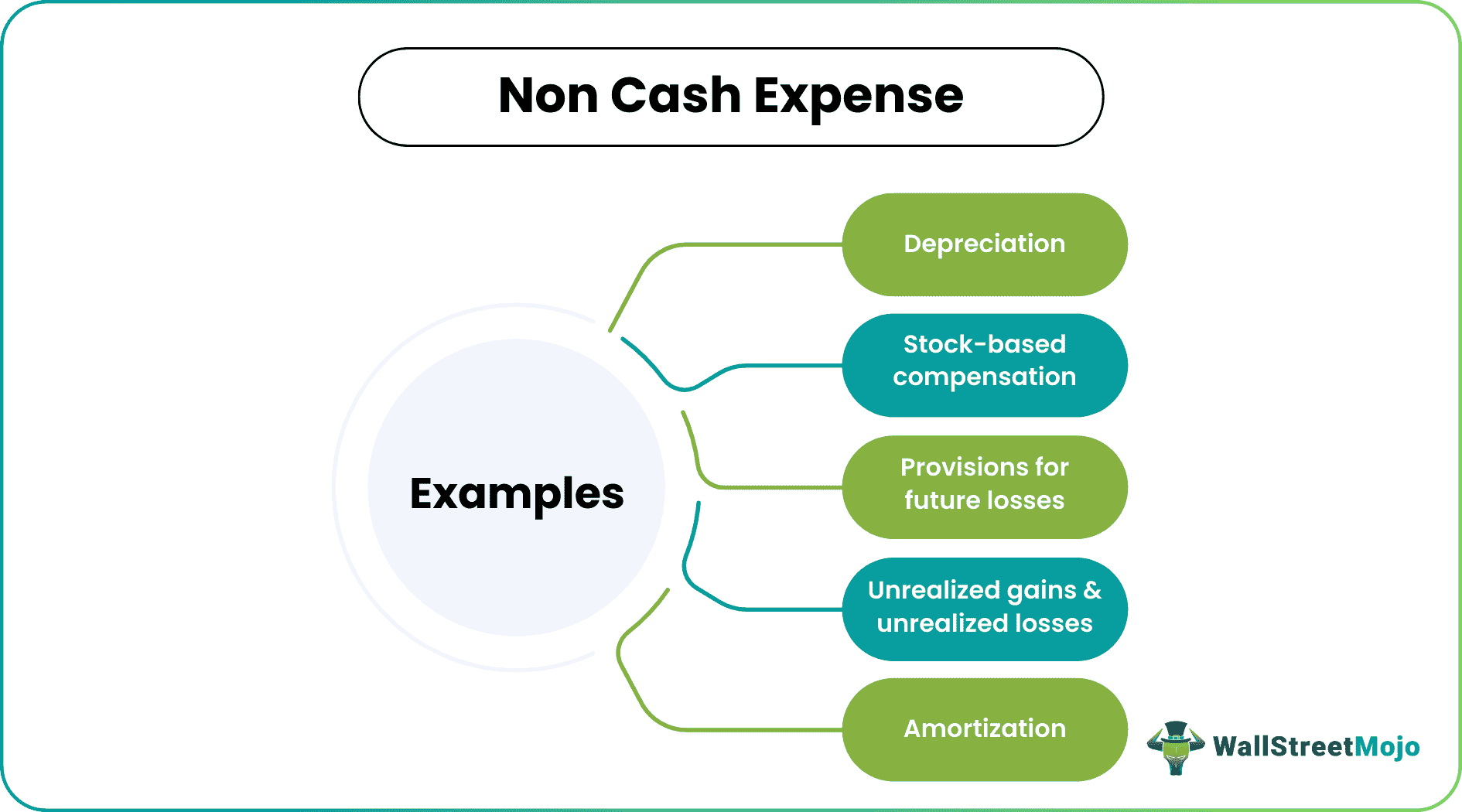

List of Non-Cash Expense Examples

Let’s look at the most used non-cash expense examples below and understand how they work.

#1 - Depreciation:

A company needs to set aside a certain amount of wear and tear if it buys any machinery or asset. And that expense is recorded every year in the company's income statement. This expense is called depreciation, and it is a non-cash expense. As mentioned earlier, depreciation is a non-cash expense.

source: Ford SEC Filings

#2 - Amortization:

Amortization Expense is just like depreciation, but for the intangible, Let’s say that a company has built a patent by expending around $100,000. Now, if it lasts for ten years, then the company has to record the amortization expense of $10,000 each year as an amortization expense.

source: Amazon SEC Filings

#3 - Unrealized gains & unrealized losses:

These are two sides of the same coin. When an investor invests in investment and feels that it would earn them more profits in the future, we call it unrealized gains. There's no cash profit. It’s just on the paper until the position is closed. On the other hand, the unrealized loss is also the same. But in this case, the investor feels that the investment will yield more future losses (but only on paper). Since these are not cash profits or losses, we will only consider them non-cash items (the unrealized loss can be termed a non-cash expense).

source: Amazon SEC Filings

#4 - Stock-based compensation:

Many companies pay their employees stock options. These stock options are included in the compensation package. These are not direct cash, but they’re the company shares. When a company doesn’t have enough cash to pay off its employees, they go for stock-based compensation. Even if the employees leave the organization; they can get full value out of their stock-based.

#5 - Provisions for future losses:

Companies often create provisions for expected losses. For example, if a company sells a portion of its total sales on credit, there's always a chance it wouldn't receive the whole amount in cash. Few customers may not pay at all, and the company would need to call them "bad debt." Before the effect of "bad debt" hits the company, it wants to protect its interest. And that’s why they create “provisions for bad debt.” And this is one of the non-cash expenses because nothing goes out in cash.

Why Are Non-Cash Expenses Adjusted for Valuing a Company?

When financial analysts look at the free cash flow of the company while conducting a discounted cash flow valuation method, noncash-expenses have no place in it. These non-cash expenses reduce the actual cash if they’re not adjusted.

That’s why these expenses are added back while calculating the firm's free cash flow. Since the free cash flow of the firm states the business's financial viability, we can’t include non-cash expenses.

Conclusion

Non-cash expenses are useful when we record them in the income statement. Recording non-cash expenses allows us to find out the net income.

But the net income of a company isn’t always useful for investors. They want to know what the company’s actual worth is. That’s why we need to value a business. To value a business, we need to examine the cash flow of business. And while calculating the free cash flow, we will add the non-cash expenses to get the actual cash inflow/outflow.

Recommended Articles

This has been a guide to non-cash expenses and a list of non-cash expense examples. We also look at how non-cash expenses are recorded in the financial statements. You may also have a look at the following accounting tutorials –