Table Of Contents

What Are Accounting Principles?

Accounting principles are the set guidelines and rules issued by accounting standards like GAAP and IFRS for the companies to follow while recording and presenting the financial information in the books of accounts. These principles help companies present a true and fair representation of financial statements.

As the name suggests, these principles are rules and guidelines maintaining which a company should report its financial data. Here is the list of the top 6 basic accounting principles –

Table of contents

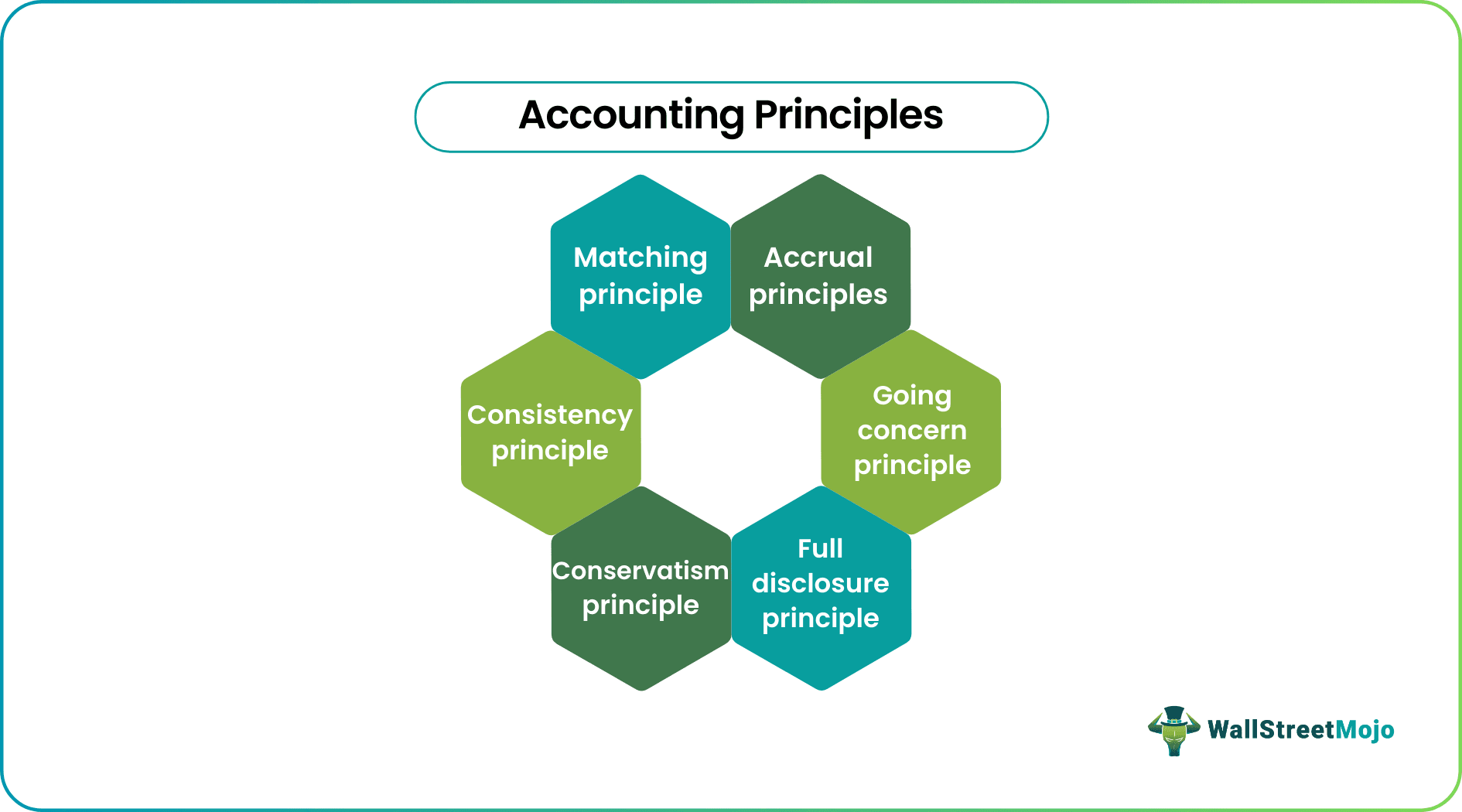

Top 6 Basic Accounting Principles

Here is the list of basic accounting principles that the company often follows. Let’s have a look at them –

- Accrual Principles

- Consistency principle

- Conservatism principle

- Going concern principle

- Matching principle

- Full disclosure principle

#1 - Accrual principle:

The company should record accounting transactions in the same period it happens, not when the cash flow was earned. For example, let’s say that a company has sold products on credit. As per the accrual principle, the sales should be recorded during the period, not when the money would be collected.

Accounting Principles - Explained in Video

#2 - Consistency principle:

If a company follows an accounting principle, it should keep following the same principle until a better one is found. If the consistency principle is not followed, the company will jump around here and there, and financial reporting will be messy. As a result, it would be difficult for investors to see where the company has been going and how it is approaching its long-term financial growth.

#3 - Conservatism principle:

As per the conservatism principle, accounting faces two alternatives – one, report a more significant amount, or two, report a lesser amount. To understand this in detail, let’s take an example. Let’s say that Company A has reported that it has machinery worth $60,000 as its cost. Now, as the market changes, the selling value of this machinery comes down to $50,000. Now the accountant has to choose one from two choices – first, ignore the loss the company may incur on selling the machinery before it’s sold; second, report the loss on machinery immediately. As per the conservatism principle, the accountant should go with the former choice, i.e., to report the loss of machinery even before the loss would happen. Conservatism principle encourages the accountant to report more significant liability amount, lesser asset amount, and also a lower amount of net profits.

#4 - Going concern principle:

As per the going concern principle, a company would operate for as long as it can in the near or foreseeable future. Therefore, by following the going concern principle, a company may defer its depreciation or similar expenses for the next period.

#5 - Matching principle:

The matching principle is the basis of the accrual principle we have seen before. As per the matching principle, it’s said that if a company recognizes and records revenue, it should also record all costs and expenses related to it. So, for example, if a company records its sales or revenues, it should also record the cost of goods sold and also other operating expenses.

#6 - Full disclosure principle:

As per this principle, a company should disclose all financial information to help the readers see the company transparently. Without the full disclosure principle, the investors may misread the financial statements because they may not have all the information available to make a sound judgment.

Recommended Articles

This was the guide to Accounting Principles and their definition. We discuss the top 6 basic accounting principles with examples and explanations. Here are the other articles in accounting that you may like –