What is Responsibility Accounting?

Responsibility Accounting is a system of accounting where specific individuals are made responsible for accounting in particular areas of cost control. In this accounting system, responsibility is assigned based on knowledge and skills. If the costs increase, the person assigned is held accountable and answerable.

- Responsibility Accounting is an accounting system where different individuals are assigned accounting responsibilities in distinguishing areas of cost control.

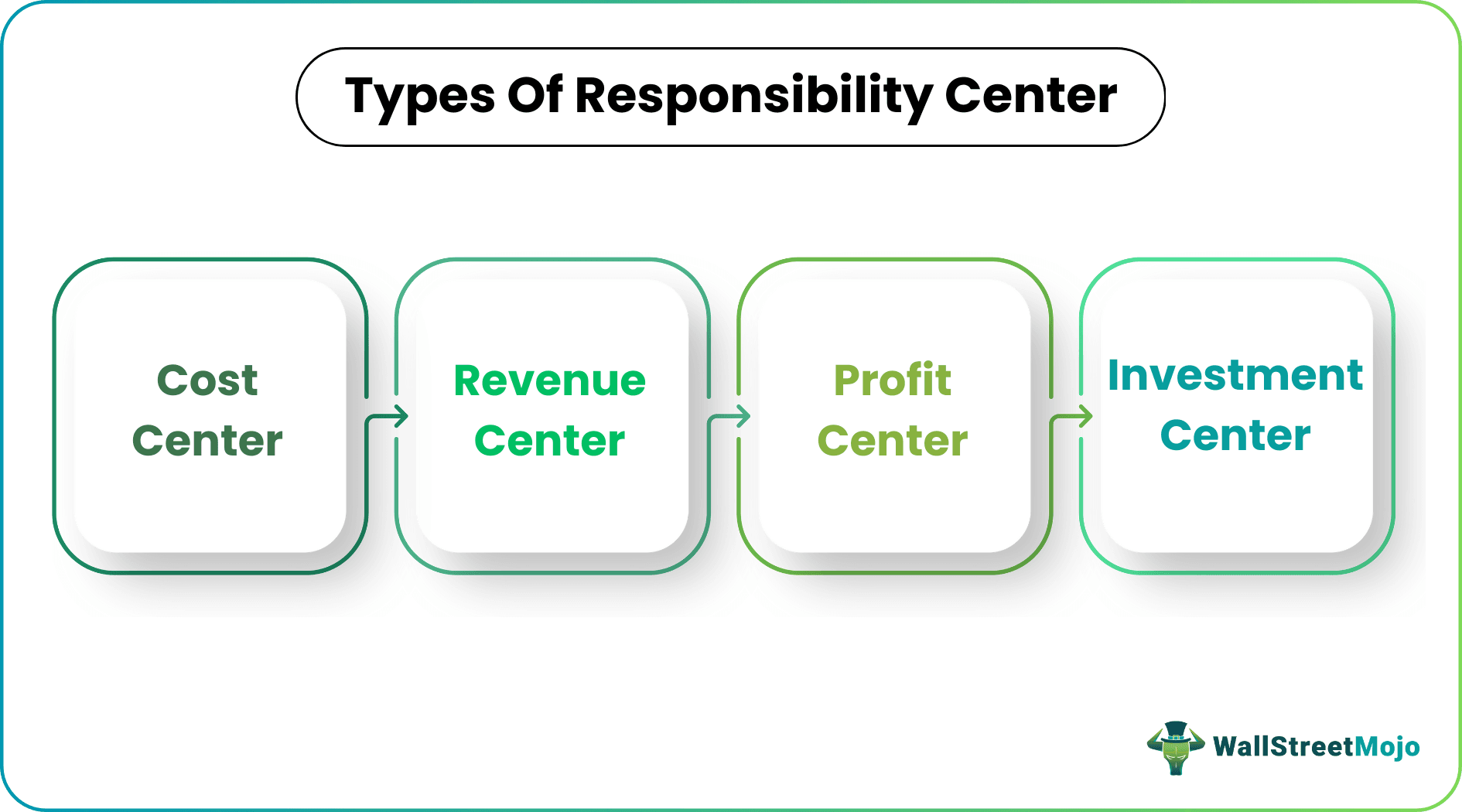

- There are four types of responsibility centers, namely the cost center, revenue center, profit center, and investment center.

- The components of responsibility accounting include inputs and outputs, identification of responsibility center, target, and actual information, responsibility between organization structure and responsibility center, etc.

- Although responsibility accounting is a method that establishes a system of control and accountability, it also requires skilled manpower, which increases its cost. Additionally, such a type of accounting also applies only to controllable costs, making it tough to be convenient always.

Steps of Responsibility Accounting

Below are the steps involved in responsibility accounting.

Defining responsibility or cost center.

Tracking the actual performance of each responsibility center.

Comparing actual performance with the target performance.

Analyzing the variance between actual performance and target performance

Fixing responsibilities for each center after variance analysis

- Communicating corrective actions to the individuals of each center.

Types of Responsibility Center

Below are the types of responsibility centers.

#1 – Cost Center

This center consists of individuals responsible only for cost control. A person responsible for a particular cost center is held accountable only for controllable expenses. Therefore, it is essential to differentiate this center’s controllable and uncontrollable costs. The performance of each center is evaluated by comparing the actual vs targeted price.

#2 – Revenue Center

The revenue center takes care of revenue, with the company’s sales teams being mainly responsible.

#3 – Profit Center

A profit center refers to a center whose performance is measured in cost and revenue. Generally, the company’s factory is treated as a profit center where raw material consumption is a cost and finished product sold to other departments is revenue.

#4 – Investment Center

A manager responsible for this center is responsible for utilizing the company’s assets in the best manner to earn a good return on capital employed.

Examples of Responsibility Accounting

Below are examples of responsibility accounting.

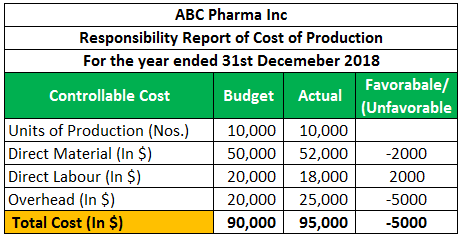

#1 – Cost Center

Below is the responsibility report on the cost of production.

ABC Pharma Inc. is engaged in the manufacturing of medicine. The company has decided to produce 10000 drugs in the year 2018. The company has defined the budget as $90,000 at the beginning of the year. However, at the end of the year, the actual cost incurred for the production is $95,000. Therefore, an excess expenditure of $5,000 over-budgeted fee was incurred. The responsibility manager is thus expected to be answerable.

It may be possible that the government has increased the electricity and water charges because overhead has increased.

The manager has used the superior quality of the material. Therefore, the cost of material has increased, but at the same time, it takes fewer workforce hours, due to which labor cost has decreased.

#2 – Revenue Center

Below is the responsibility report of the revenue center of Samsung Inc.

Samsung Inc. had targeted revenue of $95,000 from their electronic segment for 2018. But at the end of the year, they received $93,000. As a result, there is a decrease of $2000 in their revenue.

In the report below, it has been seen that the company has achieved its target in the television and washing machine division. In contrast, they have outperformed in the microwave and mobile divisions. However, their refrigerator and air conditioner division has not achieved the targeted revenue. Moreover, their electronic division target falls short by $2,000, for which the manager of their revenue center will be responsible, and he has to explain the underperformance of these two divisions.

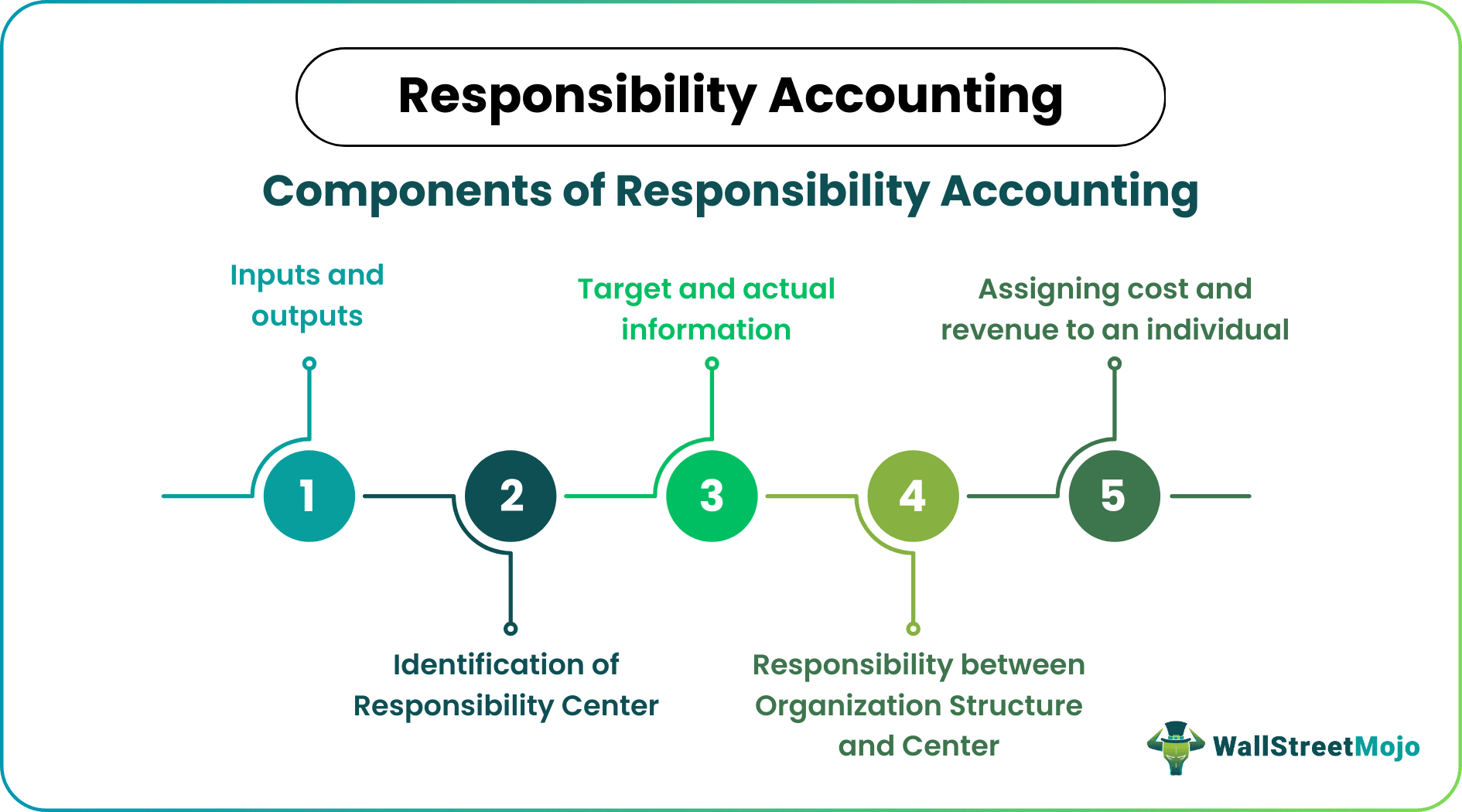

Components of Responsibility Accounting

Below are the Components of Responsibility Accounting:

- Inputs and Outputs – refer to the implementation of responsibility accounting based upon information relating to inputs and outputs. The resources utilized in an organization, such as the quantity of raw material consumed and labor hours consumed, are inputs, and the finished product generated is termed outputs.

- Identification of Responsibility Center – The whole concept of responsibility accounting depends on identifying the responsibility center. The responsibility center defines the decision point in the organization. Generally, in small organizations, one person, probably the firm’s owner, can manage the entire organization.

- Target and Actual Information – Responsibility accounting requires target or budget data and actual data for performance evaluation of the responsible manager of each responsibility center.

- Responsibility Between Organization Structure and Responsibility Center – A structure with apparent authority and commitment is required for a successful responsibility accounting system. Similarly, the responsibility accounting system must be designed per the organization’s structure.

- Assigning Cost and Revenue to an Individual – After defining the authority–responsibility relationship, cost, and revenue, which are controllable, should be given to individuals to evaluate their performance.

Advantages of Responsibility Accounting

Following are some benefits of responsibility accounting.

- It establishes a system of control.

- It is designed according to the organizational structure.

- It is anchored to the budget to compare actual achievements with the budgeted data

- It promotes the interest and awareness of in-office staff as they have to explain the deviation of their assigned responsibility center.

- It simplifies the performance report because it excludes items beyond the control of individuals.

- It is helpful for top management to make an effective decision.

Disadvantages/Limitations of Responsibility Accounting

- Generally, a prerequisite for establishing a successful responsibility accounting system like proper identification of the responsibility center, an adequate delegation of work, and good reporting are missing, making it difficult to establish this accounting system.

- It requires a skilled workforce in each department, which increases its cost.

- The responsibility accounting system applies only to controllable costs.

- If the responsibility and objective are not adequately explained, the accounting system will fail to give good results.

Conclusion

The responsibility accounting system is a mechanism by which costs and revenue are accumulated and reported to the top management to make an effective decision. In addition, it gives freedom to individuals to amplify their skills to reduce the cost and increase the organization’s revenue.

In a responsibility accounting system, organizations divide their departments into different responsibility centers, which help them focus on only those whose performance is not as per target.

At the same time, this accounting system is valid only for the big organization because it requires skill and more workforce for the responsibility center. For an effective responsibility accounting system, it is necessary all the managers must be aligned with the company objective and know their responsibility.

Frequently Asked Questions (FAQs)

What are the prerequisites for responsibility accounting?

This prerequisite of responsibility accounting necessitates an understanding of executive management’s goals by middle and operating management. Accepting responsibility for specific costs and expenses does not always follow the issuance of directives and orders.

Why is responsibility accounting important?

A type of accounting known as responsibility accounting associates expenses and revenues with the people in charge of controlling them rather than with particular goods or services. The system’s goal is to manage costs by establishing who is responsible for them.

What is social responsibility accounting?

The goal of social responsibility accounting is to manage business operations in a way that has a good overall influence on society. A business upholds its social responsibilities and informs its constituents, the public, and the government so everyone can form informed opinions. In short, it aims at social welfare.

Recommended Articles

This has been a guide to what responsibility accounting is. Here, we discuss the responsibility accounting critical components and examples and responsibility center types. We also discuss the advantages and disadvantages. You can learn more about accounting from the following articles –