Part of our Cost Control and Management guide

What are the Controllable Costs?

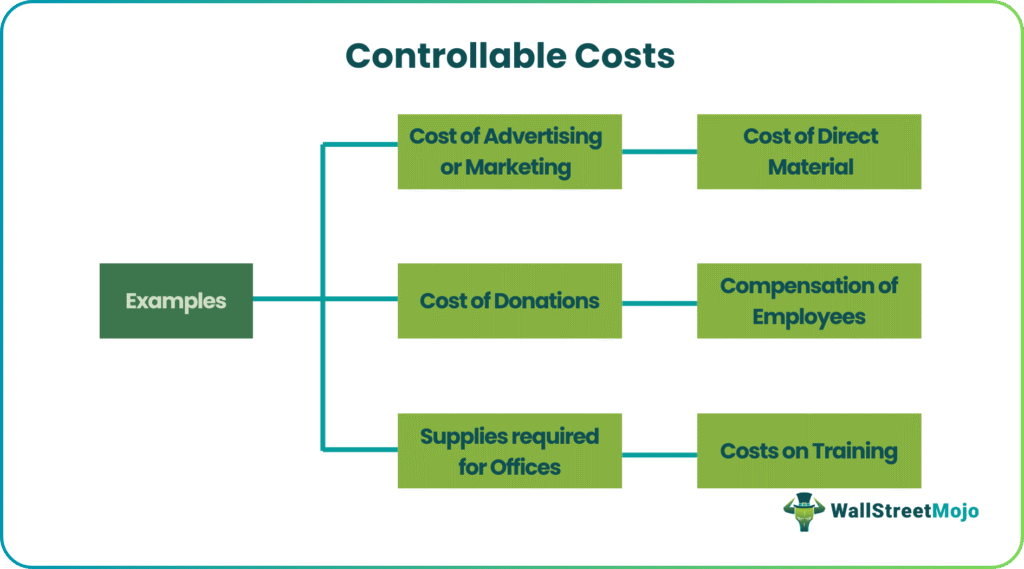

The controllable costs are the costs that can be managed and changed in the short-term horizon based on business requirements and needs. Examples of such costs include advertisement, direct material, donations, compensation, etc.

Controllable Costs Examples

#1 – Cost of Advertising or Marketing

The cost of marketing and advertising are the costs that the business bears to market its product to the outside world. Such costs comprise public relations costs, which tend to vary with the size of the business.

#2 – Cost of Direct Material

The cost of direct materials is the cost that the business must bear in procuring raw materials. The raw materials are the building blocks of the business as they are the input for the finished products that come out from the production process.

#3 – Cost of Donations

At times each business unit is prescribed to perform corporate social responsibility-related activities within the business. Such goals are passed onto the top management with the prescribed budgets on costs. Therefore, the business may donate such amounts to incorporate social activities, and the proportion they are distributed is generally controlled.

#4 – Compensation of Employees

The management generally hires individuals as employees to meet up a job. Therefore, management can hire more or fewer people to get the job done. Hence such costs are an example of controllable costs as such costs can be controlled by either revising their salaries or removing them from the job.

#5 – Supplies Required for Offices

The supplies are generally procured from the vendor market to meet the daily usage for the business requirements of the offices. Hence such costs are generally regarded as controllable, and the management has the power to establish budgets for such supplies and reduce them at the most reasonable time.

#6 – Costs of Training

Each year management allocates a budget that focuses on the training of its employees, wherein the magnitude of such costs can be controlled per the organization’s goals. The business that hires employees for a specific job may require them to be trained for that specific job. Therefore, such costs are born as training costs.

Factors

The factors that always ensure that the costs are controllable are as follows: –

- Management with High Efficacy and Efficiency: The management has to be proactive and make quick strategies on cost management and allocation once they disclose information on the financial statements.

- Strategic and Effective Monitoring of Costs: The financial statements are generally regarded as the financial terms of the business scorecard. They are not raw numbers, so the segregation of costs as presented by the statements should be studied and monitored. Effective bifurcation of costs in terms of controllable and uncontrollable should be done. This allows the costs to be more controllable and monitored effectively, wherein the management could perform comparisons on such segregations on either a monthly or yearly basis.

- Incentive Packages: The management is generally paid in accordance with the profitability they achieve. Therefore, the management is provided with incentives to curb and account for the controllable costs, and they are also penalized if such costs are not handled properly. Based on the expense report as presented in the financial statements, such incentives are chalked out.

Recommended Articles

This has been a guide to What is Controllable Costs & its Definition. Here we discuss the examples of controllable costs and their factors. You can learn more about budgeting from the following articles –