What is Hedge Accounting?

Hedge Accounting is an accounting method that allows companies to recognize the gains and losses on the hedging instruments against the exposure of the derivative instruments in the same financial period to reduce the income volatility that would arise if both elements were accounted for separately.

The new standard which defines hedge accounting in a fresher perspective would reduce the time, effort, and expense of the businesses. At the same time, investors would receive accurate and timely financial reporting. Though there would be detailed initial assessments, disclosures, risk management assessment, financial impact assessment, and data requirements, it would help is to attain the real value of the information.

Hedge Accounting Explained

Hedge accounting is a practice in accounting where the value of a derivative is adjusted according to its fair value of the hedged derivative. In simpler terms, cash flow hedge accounting helps in identifying the gains and losses for the derivatives that are hedge by adjusting or modifying their normal basis.

Companies that are exposed to market risks say foreign currency volatility, are more prone to incurring losses due to abrupt change in the value of the currency they are dealing with. To hedge themselves, they use financial instruments, such as forward contracts, options, or futures.

As per the International Financial Reporting Standards, such instruments need to be reported at fair values in the financial statements, at each reporting date, using ‘mark-to-market’ value.

Purpose

As per IFRS 9, the objective is to present, in the financial instruments, the effect of an entity’s risk management activities that use financial instruments and to reflect how those financial instruments are used to manage risk.

Types

Cash flow hedge accounting is accounted in three major types. Let us discuss them to understand the concept in detail.

#1 – Fair Value Hedge

The risk being hedged here is a change in the fair value of asset or liability or an unrecognized firm commitment attributable to a particular risk.

#2 – Cash Flow Hedge

The risk being hedged here is the firm’s exposure to variability in cash flows, currency risk, unrecognized firm commitment, or a highly probable forecast transaction.

#3 – Net Investment Hedge

When an entity has overseas subsidiaries, associates, joint ventures or branches, then the currency risk that arises due to the translation of the net assets of these foreign operations into the parent entity’s functional currency, gives rise to Net investment hedge.

Examples

Let us understand the concept of hedge accounting policy with the help of a couple of examples.

Example #1

- On January 1, 2018, an entity purchased ten shares of Apple @ $10 each.

- The entity enters into market index futures @ $3 each to hedge its position against the downfall of the share prices;

- On December 31, 2019, the share price turned out to be $ 8 each, and the market index moves to $ 5 each.

The accounting would be done in the following manner-

January 1, 2018

| Particulars | Debit | Credit |

|---|---|---|

| Equity Investment in Apple | $100 | |

| To Cash | $100 |

December 31, 2018

| Particulars | Debit | Credit |

|---|---|---|

| Other Comprehensive Income | $20 | |

| To Equity Investment | $20 | |

| Derivative Asset | $20 | |

| To OCI | $20 |

We assume that the company used the fair value method to account for the transactions. OCI stands for Other Comprehensive income.

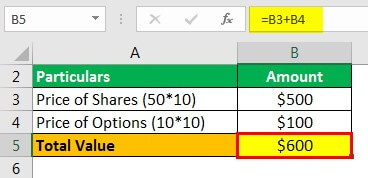

Example #2

Jack holds ten shares of Microsoft @ $50 each. To safeguard himself against the loss, if the share prices fall, he secures by taking a put option contract (right to sell the asset) at $ 10 per share for ten shares with a strike price of $ 45.

Under traditional accounting, they would have been accounted for separately, resulting in distortion of the company’s financial position. But in hedge accounting, they would be considered a bundle and accounted for.

Price of the shares (+) Price of the options contract

Therefore, the value of the contract would be

- =$500+$100

- Total Value = $600

Recording

Companies that are exposed to market risks say foreign currency volatility, are more prone to incurring losses due to abrupt changes in the value of the currency they are dealing with. To hedge themselves, they use financial instruments, such as forward contracts, options, or futures as a part of their hedge accounting policy.

As per the International Financial Reporting Standards, such instruments need to be reported at fair values in the financial statements, at each reporting date, using ‘mark-to-market’ value.

IFRS – 9

This Standard deals with accounting for financial instruments. It contains three main topics-

- Classification and Measurement of Financial Instruments

- Impairment of Financial Assets

- Hedge Accounting

This response has emerged as a response to the global financial crisis and, specifically, banks criterion of measuring impairment losses.

IFRS 9 improves the decision usefulness of the financial instruments by aligning hedge accounting with the risk management activities of an entity.

The definition remains the same with an option lying in the hands of the management, whether to implement the accounting in the organization, keeping in mind the costs and benefits associated with it.

Importance

The primary purpose of a cash flow hedge accounting is to match the recognition of the derivative gains or losses with the underlying investment gains or losses. It is an alternative to the traditional accounting method, where both are accounted for as separate line items. The recognition of both the transactions in the same accounting period is the real benefit of hedge accounting, which is lacking in traditional accounting.

Solutions

It has been made clear by analysts and experts in the market that there is surely a need to change the method of how the hedge accounting policy of a company or an individual functions. Let us discuss the need and solutions for the same through the explanation below.

The existing standard, IAS 39, was not pragmatic as it was not linked to standard risk management practices. The detailed rules had made the implementation of hedge accounting uneconomical, defeating the very purpose for which the same was created.

Another significant reason that called for a change in the rules was its lack of matching concept. A user was unable to grasp an entity’s risk management activities of an entity based on the traditional way of accounting.

Criteria

Following are the major criteria that need to be satisfied to qualify –

- Identification of derivatives

- Identification of hedged item

- Identification of the nature of the risk which is being hedged

- Assessment should be complete for how the derivative would hedge the exposure.

Recommended Articles

to what is Hedge Accounting. Here we explain Hedge Accounting IFRS – 9, along with its types, example, need, criteria and purpose. You can learn more about accounting from following articles –