Part of our Accounting Concepts guide

What Are Accounting Methods?

Accounting methods refer to the different rules the different companies follow for recording and reporting the revenues and expenses incurred by the company over an accounting period. The two primary methods include the cash method of accounting and the accrual method of accounting.

In simple words, it refers to the set of rules that determine when the revenues and expenses of a company are recognized in its books of accounts. Different methods lead to a diverse representation of a company’s financials, and which method to choose is a vital decision. The two major types of accounting methods are the accrual method and the cash method.

Accounting Methods Explained

Accounting methods are a set of guidelines used for the purpose of curating the financial reports of the company. The two major ways in which accounting documentation is carried out are cash and accrual accounting methods.

Cash accounting is based on cash values received and paid. It is the more straightforward method but is advisable only for small-scale businesses.

Accrual accounting, along with the matching principle, is based on earned revenues and incurred expenses. It reflects business performance, making it more reliable and widely accepted by users. Under the IRS rules, qualifying small businesses can use either of the two methods. However, it is important to stick to one method as it is more convenient to maintain the accounts consistently and make scrutinizing and reviewing these documents easier as well.

Accounting Methods Types

Depending on the size and structure of the company’s business, the accounts can be maintained in two major ways- the accrual and the cash accounting method. Let us understand them in detail through the discussion below.

#1 – Accrual Accounting

Under the accrual method, all revenues and expenses are recognized based on their occurrence, regardless of receiving/paid. Revenues are thus recognized when earned, while expenses are recognized when incurred. For example, a car servicing company would record revenue when it provides car services to a customer, whether or not it receives payment against the service by then.

- As for expenses, if the company uses a rented garage for its operations, the rent cost would be recognized in the period the garage is rented. For a year’s rental, 12 months’ rent would be recorded as an expense, even if less than 12 months have already been paid.

- The accrual method is based on the ‘matching principle’ which means expenses are matched (reported together) with the revenues for which they are incurred.

- Expenses that are not directly tied to any portion of revenue are to be recognized as and when they are incurred.

#2 – Cash Accounting

Under this accounting method for small businesses, transactions are recorded when money changes hands. As a result, revenues are recognized when received, while expenses are recognized when paid.

- This method does not follow the matching principle due to the differences in the timings of receipts and payments.

- For example, a gymnasium would record revenues when its members receive fee payments. As for expenses, the gymnasium would record rent costs equivalent to the rent payments made to the landlord during the year.

Examples

As mentioned earlier, it is important for companies to stick to one type of accounting for their long-term documentation. Let us understand how small businesses use cash accounting method to record their transactions with the help of a couple of accounting methods examples.

Example #1

Fabrix Inc. is a clothing manufacturer that maintains its accounts under the accrual method. On selling garments worth $10,000, Fabrix Inc. would record sales revenue of $10,000, regardless of whether it is a cash or credit sale.

Following the matching principle, any expenses incurred to gain the $10,000 revenue would also be recorded in the same period.

Say, 30% of sales commissions are to be paid to agents who sold the garments on behalf of Fabrix Inc.

In this case, Fabrix Inc. would record revenue of $10,000 and commission expense of $3000 (30% of $10,000) together in the sale period.

Example #2

Silks Inc., that uses the cash method. In a similar sale like the above example, Silks Inc. would record only that portion of the $10,000 sales against which it has received payment.

In case of a 60% credit (40% cash) sales policy, Silks Inc. would recognize revenue to the extent of $4000 only, i.e., 40% payment received on the $10,000 sale.

Even if directly tied to this sale, any commissions or other expenses would be recorded when Silks Inc. makes its payment.

Advantages

Both cash and accrual accounting method have their own set of advantages based on their usage in a particular set up. Let us understand them in detail through the explanation below.

#1 – Accrual Method

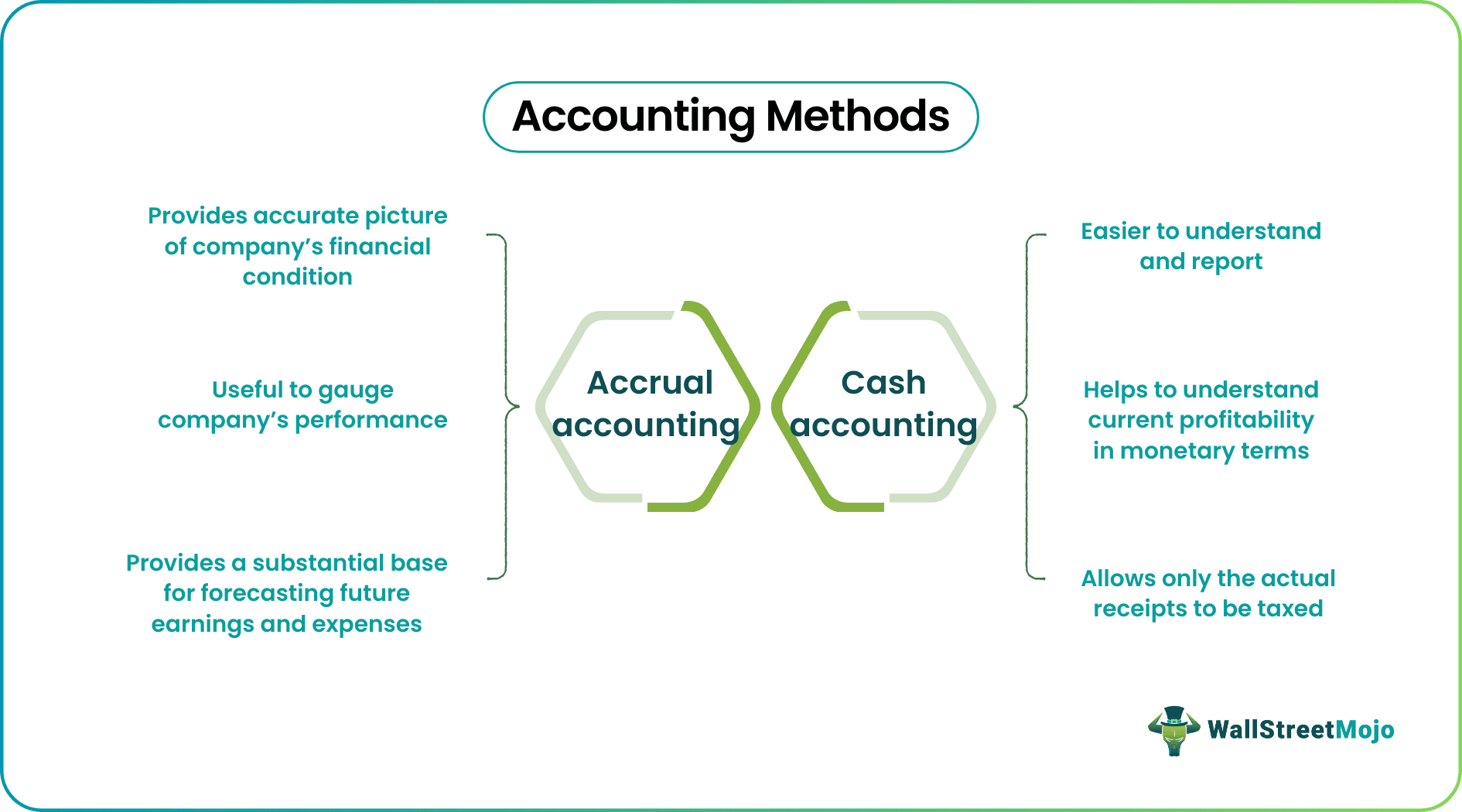

- The accrual method provides a more accurate, clearer picture of a company’s financial condition in a particular accounting period.

- Most investors and analysts find financials reported using the accrual method more useful in gauging a company’s performance.

- The accrual method also provides a more substantial base for forecasting future earnings and expenses and related decision-making.

- Large, well-established businesses and publicly listed companies generally use the accrual method. In the U.S., the Internal Revenue Service (IRS), the government agency that administers and enforces U.S. federal tax laws, has laid out specific criteria for companies required to use the accrual method.

#2 – Cash Method

- The cash method requires less effort and is easier to understand and report. It does not require much accounting staff and, in most cases, can be handled solely.

- It directly reflects the value of cash inflows and outflows, which helps understand the current profitability in monetary terms.

- It allows only the actual receipts to be taxed rather than the total earnings. This may help the company in tax planning and avoid a significant tax burden in periods of cash crunch (lower net inflows).

- Smaller businesses with no/low inventory, start-ups, and individual taxpayers generally prefer the cash method to ease accounting.

Change in Methods

Even though the Internal Revenue System (IRS) requires companies or individuals to maintain a consistent system of accounting. However, they can be changed with the permission of IRS, provided they are eligible for the shift.

- Companies are generally encouraged to use any one of the above methods consistently. This practice avoids the manipulation of accounts for representation and tax purposes.

- The accounting method may be changed depending on the rules and policies prevailing in the relevant jurisdiction/regulator of the company.

- The IRS, for instance, requires all taxpayers to use a consistent accounting method, one which accurately reflects their financial affairs. It requires the taxpayer to seek special approval should they wish to change the method after the first year. It also allows for a hybrid accounting, a combination of the accrual and cash methods; however, it is subject to certain restrictions.

Accrual Vs Cash Accounting Method

Two of the most widely used methods of accounting are often discussed alongside one another but it is important to understand their differences before choosing the right one as shifting to another method would involves a lengthy procedure.

Below is the list of differences between cash and accrual accounting method.

- The accrual method recognizes revenues and expenses entirely during one period, i.e., when earned/incurred.

- On the other hand, the cash method may result in transactions about a single sale/expense spreading across several periods, based on the timing of payment. This leads to the accounts not accurately reflecting the financial performance in any given period.

For instance, a period showing higher revenues may not necessarily mean improved sales performance. It could rather only mean that more cash was collected from customers against sales made.

Recommended Articles

This has been a guide to what are Accounting Methods. We explain its types- accrual & cash along with examples, and advantages. You can learn more about accounting from the following articles –