Part of our Journal Entries guide

What Is Special Journal?

Special Journals are all accounting journals in an organization except the general journal. All the transactions of similar transactions are recorded in an organized form that helps the company’s accountants and bookkeepers keep track of all different business activities properly.

They record some particular types of journals like purchase and sales. It saves time and helps avoid the monotonous task of recording the account names and amounts in the general ledger. Instead of posting each entry separately, the total of each column is posted during the end of an accounting period.

- All accounting journals inside an organization—aside from the general journal—are classified as Special Journals. The company’s accountants and bookkeepers can correctly track all business operations since all transactions and comparable transactions are grouped and documented in a structured manner.

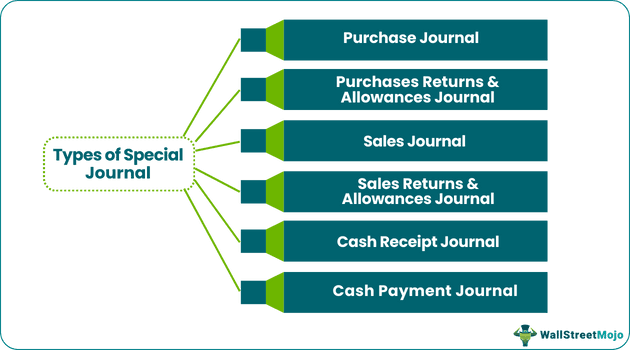

- Special journals are of the following types: Purchases Journal, Purchases Returns & Allowances Journal, Sales Journal, Sales Returns & Allowances Journal, Cash Receipt Journal, and Cash Payment Journal.

- In that specific special journal, all accounting transactions of a comparable sort will be documented. The bookkeepers and accountants will be better able to keep track of all the various company operations since they will be able to record all the connected transactions in an orderly manner.

- The majority of small transaction firms don’t keep a particular diary. Instead, they just record all business transactions in the general journal before posting them to relevant general ledger accounts.

Special Journal Explained

Special journal entries are any journal except the general journal, which records a special type of information that has a high volume and would be tedious to record in the general journal.

They record the specific transaction of the company by categorizing them into different types or groups. Special journal accounting helps the company maintain the accuracy of the transactions in an organized form. It can also be reviewed by the company later. In case the company does not use this journal, all the transactions would be recorded in the General journal only, and at a later stage, it would become difficult to look at the specific types and nature of transactions.

They record transactions of a similar nature under one journal and do not include the general journal. It helps monitor all the transactions during a period in an organized form. It ensures that the company takes the necessary actions for those transactions.

The companies where small numbers of transactions are involved generally do not maintain special journal entries. Instead, they record the entire transaction in the business in the general journal only and then post them to related accounts in the general ledger.

Generally, companies maintain this type of journal only for those types of transactions that frequently occur in the business or are repetitive.

Types

There are different types of special journal accounting, where some of the commonly used in accounting include the following:

#1 – Purchases Journal

Purchase Journal records all the transactions related to the purchase of the goods on credit from the suppliers.

#2 – Purchases Returns & Allowances Journal

Special journal books include all the transactions related to the return of goods to the supplier, purchased on credit, or allowances received from the supplier.

#3 – Sales Journal

Sales Journal records all the transactions related to the sales of goods by the company to its customer on credit.

#4 – Sales Returns & Allowances Journal

It records all the transactions related to the return of goods back by the customers sold on credit and allowances given to the customers.

#5 – Cash Receipt Journal

Cash Receipt Journal records all the transactions in which the company receives cash, like transactions involving the sale of goods for cash, sale of the company’s assets for cash, and capital investment by the owner of the company in the form of cash, etc.

#6 – Cash Payment Journal

It records all the transactions involving the outflow of cash from the company and includes the transactions such as cash paid to suppliers, cash paid for expenses, etc.

Examples

There is a company A ltd which has a large scale business. It maintains the record in special journals to keep the records organized and in better form. One of them is the sales journal, which the company uses to record all the transactions related to the sales of goods on a credit basis.

When the company sells the goods to its customer on a credit basis, there will be a debit to the account receivable account and a credit to the sales account. So, this transaction will be recorded in the sales journal by debiting the accounts receivable account. When the company receives the payment against accounts receivable, the same will be recorded in the cash receipt journal. If there is any return from the customer, then the same will be recorded in the sales returns and the allowances journal.

Journal vs Ledger Video Explanation

Advantages

Some of the advantages are as follows:

- All the accounting transactions of a similar nature will be recorded in that particular special journal. As they record all the related transactions in an organized form, this will help the accountants and the bookkeepers keep track of all the different business activities properly.

- Generally, in large companies, each special journal format is handled by separate persons, which makes the person specialized in that area, thereby increasing its efficiency of working and reducing the chances of errors in bookkeeping.

- Companies, where such journals are maintained internal control, are better. With such a division of work, the employee’s conflict concerning their responsibilities decreases, and the quality of work increases.

Disadvantages

Some of the disadvantages are as follows:

- If an error occurs while maintaining and recording the transactions in the special journal by the person responsible for the same, it can show the wrong balances of that journal.

- If the company does not use special journal format, then all the transactions would be recorded in the general journal only. It would become difficult to look at the specific types and nature of transactions at a later stage.

- As separate persons may handle each of these journals, the company needs to appoint various employees, thereby increasing the employee cost of the company.

Special Journal Vs General Journal

Special journal books include all records of a particular type of transaction whereas general journals record any type of transaction. The basic difference between them is as follows:

| Special Journal | General Journal |

| Records special types of journals. | Records all journals. |

| Records transaction that are repetitive. | Records transactions that are not repetitive. |

| Useful for large and medium sized businesses. | Useful for small businesses. |

| Transactions are recorded in one entry. | Transactions are recorded in two or more entries. |

Frequently Asked Questions (FAQs)

What is a special journal used for?

They do not contain the general journal and instead group related transactions under one journal. Additionally, they provide structured monitoring of all transactions during a given period. It guarantees that the business makes the appropriate moves for such transactions.

What is the advantage of preparing a special journal?

Better businesses keep internal control through customized journals. With such a division of labor, the employee experiences less disagreement over their duties and produces higher-quality work.

What are the limitations of having a special journal?

All transactions would only be recorded in the ordinary journal if the business did not employ the special journals. It will be challenging to analyze the precise nature and sorts of transactions in the future.

Recommended Articles

This article has been a guide to what is a Special Journal. Here we explain it with examples, types, advantages, vs general journal, and its disadvantages. You can learn more about accounting & bookkeeping from the following articles –