Part of our General Ledger guide

What Is General Journal?

The general journal is the company’s journal in which initial record keeping of all the transactions is done which are not recorded in any of the specialty journals maintained by the company like purchase journal, sales journal, Cash journal, etc.

These journal entries are then used to form a general ledger, and the information is transferred into respective accounts of the general ledger. The ledgers are then used to make trial balances and, finally, the financial statements. However, these journals were more visible in the manual record-keeping days.

General Journal Explained

General journal accounting is called the book of original entry, where accountants record financial transactions of the business as per their date of occurrence. The pages are divided into columns where items like dates, serial numbers, debits and credits are recorded in the double entry book keeping system or format.

It is different from the specialized journals like sales, purchase etc, where only items related to them are recorded. It mainly keeps the details of five major accounting heads which are assets, liabilities, revenue, expense and capital.

Whenever an event or transaction occurs, it is recorded in a journal. Journal can be of two types – a specialty journal and a general journal.

A specialty journal records special events or transactions related to the particular journal. There are mainly four kinds of specialty journals – sales journal, Cash receipts journal, Purchases journal, and cash disbursements journal. The company can have more specialty journals depending on its needs and type of transactions, but the above four journals contain the bulk of accounting activities.

All other transactions not entered in a specialty journal account for in a General Journal. It can have the transactions related to Accounts receivables, Accounts payable, Equipment, Accumulated depreciation, Expenses, Interest income and expenses, etc.

With the advent of technology, record keeping has been easy, with all the information being stored in a single repository with no specialty journals in use. However, these general journal accounting were more visible in the manual record-keeping days.

Accounting

The accounting method of general journal entries are given below:

Double entry bookkeeping is the most common method of general journal accounting. An exchange between two accounts does every business transaction. There are two equal and opposite accounts for all the transactions: credit and debits. Hence, a transaction recorded in a journal debits one account and credits the other.

For example, A company purchases $5000 of inventory using cash. An entry in the journal would be made whereby the cash account is decreased by $ 5000, and the inventory account is increased by $ 5000.

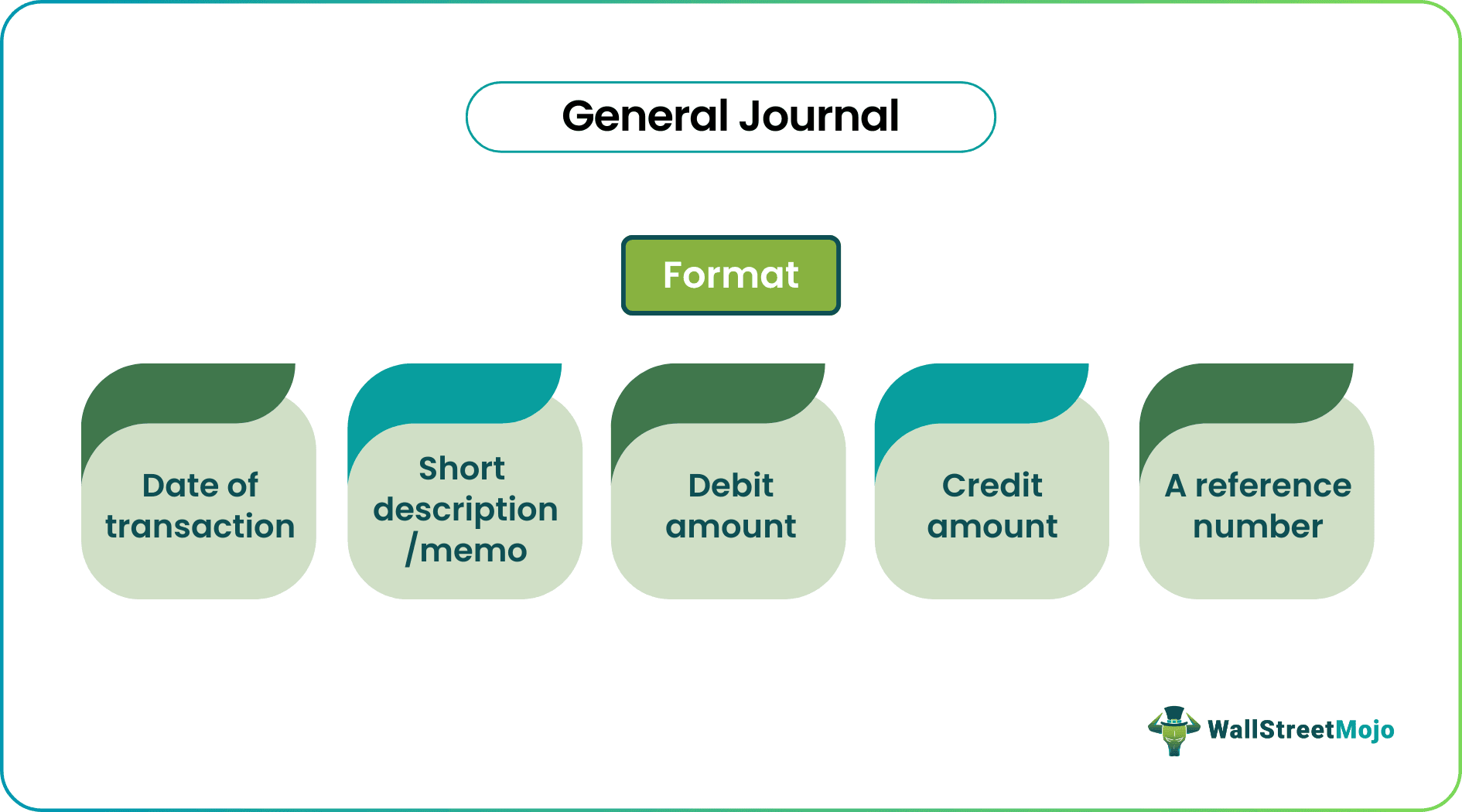

Format

Given below are the format for general journal entries.

It provides the chronological order of all non-specialized activities. It consists of 4 or 5 columns:

- Date of transaction

- Short description/memo

- Debit amount

- Credit amount

- A reference number (referencing to journal ledger as an easy indicator)

General Journal Video

Examples

Let us understand the concept with the help of some general journal sample.

| Date | Account Title and Description | Debit | Credit | Reference |

|---|---|---|---|---|

| 31/7/2018 | Depreciation Expense | 20000 | A2018-614 | |

| Accumulated Depreciation for July 2018 | ||||

| To record depreciation for July 2018 | 20000 | |||

| 1/8/2018 | Inventory | 5000 | A2018-544 | |

| Cash | ||||

| To record inventory purchase | 5000 | |||

| 2/8/2018 | Utilities | 1000 | A2018-125 | |

| Cash | ||||

| To record August 2018 utilities purchase | 1000 | |||

| 3/8/2018 | Cash | 15000 | A2018-687 | |

| Sales | ||||

| Collected the cash for sales to be recorded in sales account | 15000 | |||

| 4/8/2018 | Cash | 7500 | A2018-619 | |

| Capital | ||||

| Owner contributed capital to the business | 7500 |

In the above table of general journal examples, we can see each transaction as two lines- one debit and one credit account.

Flow Process

Let us look at the flow process of entries before and after it is recorded in the general journal. Before entry is made, the maker has to decide:

- the accounts which will be affected by the transaction

- which account to debit and which account to credit

After making entries in the general journal format in accounting, all the transactions are summarized and posted in the ledger.

A ledger is an account of final entry, a master account that summarizes the transactions in the Company. It has individual accounts that record assets, liabilities, equity, revenue, expenses, gains, and losses.

Some examples of accounts in the ledger:

- Accounts receivable (an asset account)

- Accounts payable (a liability account)

- retained earnings (an equity account)

- product sales (a revenue account)

- cost of goods sold (an expense account)

To summarise: every accounting transaction is stored in a journal that acts as an intermediary repository of information, which is then recorded in a general journal ledger. The ledger, in turn, is used to aggregate this information into the financial statements of a business, which are called an initial trial balance.

Uses

We discussed the use of journals in recording the Company’s transactions and its use in general journal accounting. A journal can also be used in investing. An individual trader or a professional fund manager can form a journal where he records the details of the trades made during the day. These records can be used for taxation, audit, and evaluation purposes.

These records can help traders evaluate their trading and investing performance over time and provide information about their failures and successes. The traders can learn from the past and improve in future trades.

Such a journal generally consists of profitable and unprofitable trades, watchlists, pre, and post-market conditions, and analysis and notes on each trade being bought or sold.

Technological Advances

While these have been in practice since record-keeping was done, with advances in technology, nearly all companies, and even small businesses are using general journal format software. This software’s simple data entry logs these transactions in the journal and ledger accounts. Many of these software provides simple drop downs to record the transactions, thus making complex and tedious tasks very easy.

Advantages

Some of the advantages of general journal sample are as given below:

- It gives all details about any kind of financial transactions of the business.

- It explains the details of the transaction.

- Since it is recorded in a chronological order, it is very easy to locate a business transaction using the date.

- Since recording is done immediately, there is less chance of transactions not getting recorded.

- There is less chance or error since recording is done in journal form with double entry.

- Ledger entries become easy due to details given in the general journal.

Disadvantages

- It has to be done everyday for every transaction, which becomes tedious and monotonous.

- If it is not kept in a secured place, it may result in information leak.

- Explanation requires writing skills that will explain the transaction clearly.

General Journal Vs General Ledger

Let us look at the basic differences between the above two topics.

- The former records the transactions in the form of journal with double entry format whereas the latter records the transaction in ledger format for items related to income, expense, assets, liabilities and capital.

- Any tansaction is first recorded in the journal, then in the general ledger.

- Transactions get transferred from journal to the ledger and next from general ledger to the trial balance.

Recommended Articles

This article has been a guide to what is General Journal. We explain it with example, accounting, format, differences with general ledger, uses & advantages. You may learn more about Accounting from the following articles –