Part of our Accounts Payable & Receivable guide

What Is The Cash Receipts Journal?

The cash receipts journal is that type of accounting journal that is only used to record all cash receipts during an accounting period and works on the golden rule of accounting – debit what comes in and credits what goes out.

Credit sales are not recorded in this accounting journal because there isn’t any cash collected in those credit sales transactions. Cash sales work on the cash basis of accounting, and credit sales on the accrual basis of accounting.

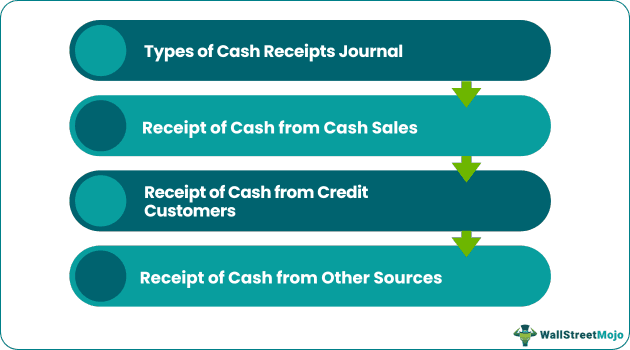

Types of Cash Receipts

They can be further divided into three different parts as well which are broken down below:

- Receipt of Cash from Cash Sales: All cash received from cash sales of goods and services to customers is recorded in the cash receipts journal, mentioning the counterparty’s name in the narration.

- Receipt of Cash from Credit Customers: All cash subsequently collected after making credit sales to the customer basis the credit period advanced.

- Receipt of Cash from Other Sources: All other sources of cash such as Bank Interest, Maturity of investments, sale of non-inventory assets, sale of fixed assets, etc.

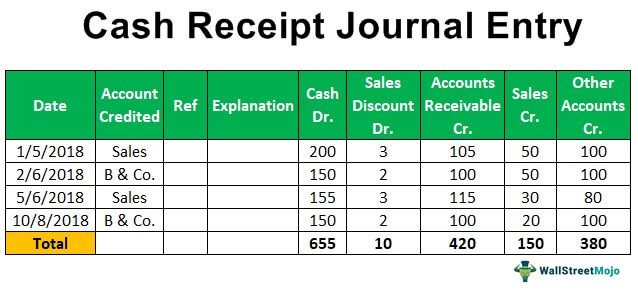

Example of Cash Receipt Journal

When a retailer/wholesaler sells goods to a customer, and it collects cash, this transaction is recorded in the cash receipts journal.

Investment of capital by the owner of a business is recorded in cash receipts, sale of an asset for cash is recorded in cash receipts, all kinds of collections from credit customers are recorded in cash receipts, collection of bank interest,, dividend or rental income is also recorded in cash receipts journal.

Another Loan taken by an individual from any bank or financial institution is also recorded in the cash receipts journal. Any fee and commission received the maturity of an investment or an insurance policy, tax refunds for direct and indirect taxes, Donations received also form part of this journal and help keep track of liquidity inflow and cash flow analysis for an organization periodically, which ultimately forms part of IFRS reported financial statements and various disclosures made to other stakeholders and government authorities.

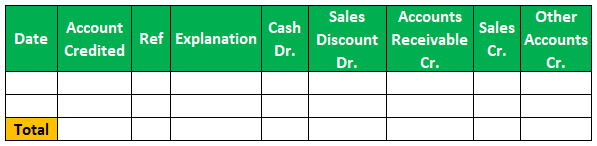

Cash Receipts Journal Format

The format usually looks like the below:

Explanation of Columns Used in Cash Receipts Journal

- Date (Column 1): The date on which the cash is received is entered in the date column.

- Account Credited (Column 2): This is the account name that is credited due to the receipt of cash in the books of accounts.

- Ref (Column 3): The reference column is used to enter the internal reference number of the account to which the journal entry belongs.

- Explanation (Column 4): The explanation or narration of the cash receipt is briefly explained in this column.

- Cash Dr(Column 5): The amount of cash received is entered in this column. The cash in the general ledger account is debited by the amount coming in this total.

- Sales Discount Dr(Column 6): Sellers allow a discount to buyers who make payment within credit period allowed. The total amount of discount allowed to buyers is entered in this column.

- Accounts Receivable Cr (Column 7): When a credit customer/buyer makes the payment, his account is credited in the accounts receivable ledger. The amount by which a customer’s/buyer’s account is credited is filled in this column.

- Sales Cr (Column 8): This column records cash sales. Every time a cash sale is made to a customer, the amount received is entered in this particular column.

- Other Accounts Cr (Column 9): This column is used to record the receipt of cash from other sources, including cash for interest, rent, the sale of fixed assets, etc.

Video Explanation of Journal vs Ledger

Practical Example

The following example shows how cash receipt journal accounting works and is recorded in accounting ledgers:

List of Transactions

Highlight

- 07/08/2019 – Cash Sales made of £5,000.

- 12/08/2019 – Cash received from credit customer Douglas of £490 after-sales discount of £10.

- 14/08/2019 – Cash Sales made of £7,000.

- 17/08/2019 – Cash received from credit customer Rob of £990 after-sales discount of £10.

- 20/08/2019 – Loan from Bank £1,500.

- 21/08/2019 – Cash Sales made of £6,500.

- 22/08/2019 – Interest received on Bank account of £350.

- 23/08/2019 – Cash received from credit customer John of £741 after-sales discount of £9.

- 25/08/2019 – Cash received from credit customer Amanda of £345 after-sales discount of £5.

- 28/08/2019 – Cash Sales made of £9,000.

Advantages

- Helps in keeping track of all cash received during the period.

- Helps in preparation of cash account ledger and cash flow statement for the period.

- Helps in keeping track of trade receivables and aged receivables.

- Helps in keeping track of all outstanding and aged supplier payments by matching the cash received with cash paid during the period.

Disadvantages

A single disadvantage of the cash receipts journal is that it only considers the cash basis of accounting. It doesn’t consider the accrual basis of accounting which is the principal basis of doing double-entry bookkeeping and prudent accounting.

Post Posting Checks

There are two post posting checks which can be made following the posting of the cash receipts journal at the end of an accounting period to ensure that the transactions during the period have been correctly entered and presented in ledgers and the financial statements of an organization:

- The total of all the customer sub-ledger balances appearing under the account heading accounts receivables should always be equal to the balance on the sub-ledger control account in the general ledger trial balance.

- Also, the general ledger trial balance should always be in balance, which means that the total debits in the general ledger should equal the total credits so that the balance sheet also matches at the end.

Recommended Articles

This has been a guide to what is a cash receipts journal and its definition. Here we discuss its types, example, format, advantages, and disadvantages. You can learn more about economics from the following articles –

Recommended Articles

Continue with these closely related articles from the same guide.