Journal Entry of Deferred Revenue

The following Deferred Revenue Journal Entry outlines the most common journal entries in Accounting. In simple terms,, Deferred Revenue means the revenue that has not yet been earned by the Products/Services are delivered to the Customer and is receivable from the same.

- It is not revenue for the company since it has not been earned.

- It is an advance payment received from Customers for the Product/Services delivered and is the company’s liability.

- It is reflected as “Advance from Customers” on the Liability side of the Balance sheet and considered revenue when earned. For Example, If a Company receives $100,000 from a Customer for a Product to be made and delivered. In this case, $100,000 was recorded as Liability on the Balance Sheet. The same shall be considered income by writing off the liability only when the product is delivered to the Customer.

Examples of Deferred Revenue Journal Entry

The following are examples of the deferred revenue journal entry.

Example #1

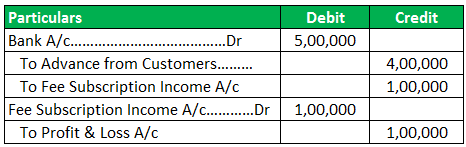

Suppose Company A has sold Software to another Company B and received the Subscription Fees for the same $100,000 per year for the next 5 Yrs.

- In this case, Company A will show$100,000 as yearly revenue and $400,000 on the liability side of the Balance sheet as “Advance from Customers,” which subsequently be recorded as revenue every year for the next 4 Years

- Journal Entries:

Example #2

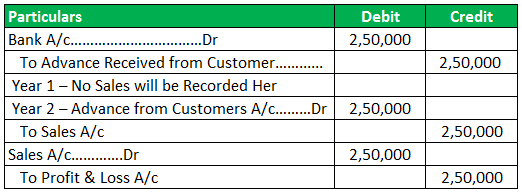

Suppose Company A has supplied goods to Company B and received the advance payment of 250000 for the same on the agreement to supply goods next year.

- In this case, the Entire Money would reflect on the Liability Side of the Balance Sheet, and nothing will be recorded as Sales since no goods are supplied to the Customer in Year 1.

- Journal Entries:

Example #3

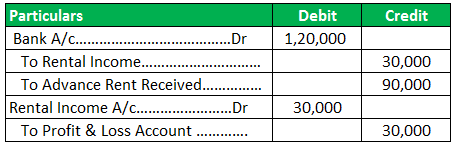

Suppose Mr.A pays Rent to MrB. For the living in the former house. Rentals are 10,000 per month. Mr. A started living in the house in December 2018 and paid 120000 as Rentals to Mr. B.

- In this case, If Mr. B prepares his Annual Financial Statements as of 31st March 2019, he will record 30,000 as Rental Income from Mr.A, and the balance of Rs 90,000 will be deferred to next year since the same is not earned in the current Financial Year.

- Journal Entries in B’s Books:

Example #4

Suppose a Pest Control Company receives a Contract from a Multinational Company for the full year to offer Pest Control Services at the Corporate Office @ 1200000 annually.

- In this case, the Pest Control Company will recognize the revenue as 1 lac per month since the services are to be rendered every month to the MNC.

- Journal Entries :

While preparing the monthly Financials of the Company, the 12 lakh money received will be apportioned as 1 lakh per month, and 11 lac would be recorded as advance from the Customer in the Monthly Balance Sheet prepared by the company.

Example #5

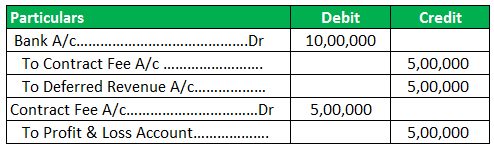

Suppose Company A is allotted a Contract to complete a project for the next 5 yrs, and 10,00,000 is the advance given for the same by company B.

- In this case, Company A will recognize the revenue as per the Completion of the Project. If 50% of the project is completed at the end of Year 1, 5,00,000 will be recorded as revenue, and a Balance of 5,00,000 will be shown as Deferred Revenue and recognized when the balance of 50% of the project gets Complete.

- Journal Entries:

Example #6

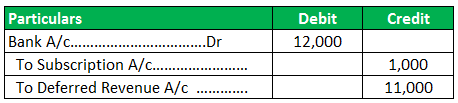

Suppose Company A sells magazines online to customers @ 1000 per magazine per month. Once the Customer Subscribes for the same online and pays 12,000 annually for the magazine, the company will start recognizing revenue monthly for 1000, and 11000 would be recorded as Unearned Revenue, and the same would be transferred to Income A/c as and when the magazines are actually delivered to the Customer.

- Journal Entries for Monthly Accounting:

- Next Month :

- Every Month:

Example #7

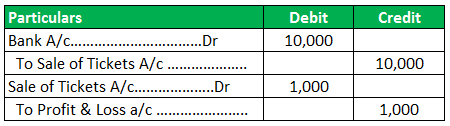

Suppose Company A sells Tickets for IPL Series. The Customer buys 10 Tickets Online for different matches. Ticket Cost = 1,000

- In this case, Company A will recognize the revenue as soon as one match ends, and the balance amount will be deferred.

- Journal Entries:

- The Balance in the Sale of Tickets Account will be reflected in the Liability side of the Balance Sheet and will be utilized when the IPL Match ends. If all nine matches are concluded and one match gets canceled, the balance in the Account, i.e., 1,000, would continue to be a part of the Liability Side of the Balance Sheet unless the same is repaid to the Customer as a Refund.

Revenue vs Income Explained in Video

Conclusion

Hence Deferred Revenue refers to the advance Revenue the Company receives for the Sale of Products/Services for a particular period. Only a small portion of it is recognized as Earned Revenue. The balance is shown on the Liability side of the Balance Sheet as Deferred.

Recommended Articles

This article has been a guide to Deferred Revenue Journal Entry. Here we discuss the Top 7 examples of deferred revenue journal entries and detailed explanations. You may learn more about accounting from the following articles –