Part of our Journal Entries guide

What Is Unearned Revenue?

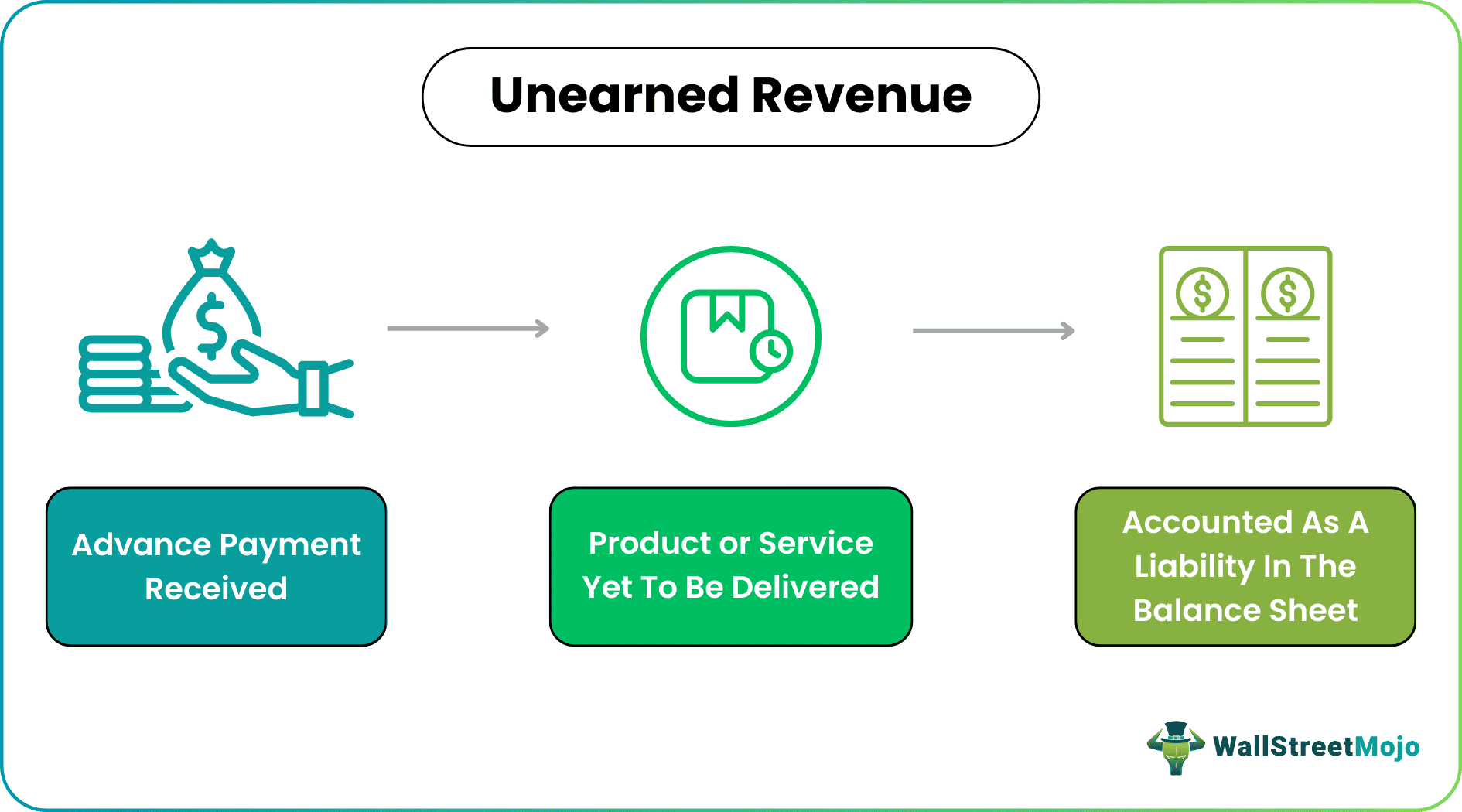

Unearned revenue is the income received by an individual or an organization for a product or service that is yet to be delivered. It is documented as a liability on the balance sheet as it represents a debt or outstanding balance that is owed to the customer. It is also referred to as deferred revenue or even advance payment.

The pending goods are recorded as current liabilities. Once the products or services are delivered, the unearned revenue balance sheet entry is converted into revenue as the value in return for the payment received is delivered. Advance payments help companies and individuals with cash flow and other immediate payments which makes the production process faster.

Unearned Revenue Explained

Unearned revenue refers to the compensation or payment received by an individual or an organization for products or services that are yet to be delivered or produced. These prepayments help companies to better their cash flows and produce the product or service with lesser hassle.

Unearned revenue entry is a common feature in various industries. In fact, a lot of common items consumers purchase are based on this payment system such as subscription-based products, airplane tickets, prepaid insurance, retainers to attorneys, and so on.

The deferred payments are recorded as current liabilities in the balance sheet of a company as the products or services are expected to be delivered within the current year. Once the goods or services are delivered, the entry is converted to a revenue entry through a journal.

Unearned Revenue (Sales) Explained in Video

Journal Entries

The following unearned revenue entry example provides an understanding of the most common type of situations where such a Journal Entry accounts for and how one can record the same as there are many situations where the Journal Entry for Unearned Revenue passes, it is not possible to provide all the types of examples. Unearned Revenue is where the money is received, but the goods and services are yet to be delivered. As per the revenue recognition concept, it cannot be treated as revenue until the goods or services are provided.

Therefore, it is treated as a current liability.

Steps

Let us understand the steps involved in theunearned revenue balance sheetentry through the detailed step-by-step process below.

- Divide the amount received for providing goods or rendering services by the number of months of services/goods for which the amount is received. For example, professional fees of $6,000 are received for six months. Therefore $6,000 divided by 6, which is $1,000, would be recognized as monthly income.

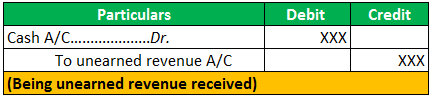

- Debit the cash/bank account with the total amount received, i.e., $6,000, and create a current liability of unearned revenue by crediting the same amount. The revenue is yet to be earned by the business, and hence the same is credited as a liability. Since the cash is received, it is the creation of the asset. Therefore, the corresponding debits.

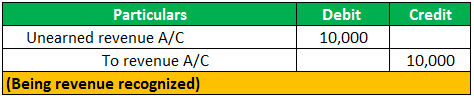

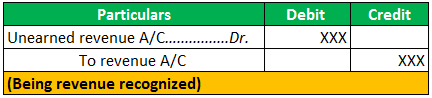

- At the end of each month, the liability of unearned revenue would be reduced by $1,000 by debiting the amount, and revenue would be increased by crediting the same amount.

Examples

Let us understand how unearned revenue balance sheet documentation is carried out with the help of a few examples. These examples will give us more relevance as they have been curated keeping daily situations in mind.

Example #1

On 1st April, a customer paid $5,000 for installation services, which will render in the next five months. The amount received would be recorded as boo’s unearned income (current liability). Subsequently, unearned revenue liability would decrease, and revenue would be recognized monthly.

Following journal entries will be recorded:

Example #2

On 1st March, the landlord receives rent 12 months in advance, amounting to $12,000. The rent received would be recognized in books as advance rent, and $1,000 would be treated as rental income each month. Following journal entries will be recorded:

Example #3

On 31st May, a contractor received $100,000 for a project to be executed over ten months. The $10,000 would be recognized as income for the next ten months in the contractor’s books. The total amount received would be recorded as unearned income as the project is yet to be completed.

Example #4

On 5th June, an insurance company received a premium of $24,000 from Mr. XYZ for 12 months. Since the period covered is 12 months, the initial amount received would be recorded as a liability in the books of insurance providers. Subsequently, every month $2,000 would be recognized as income. The following journal entries will be recorded:

Example #5

On 10th June, a chartered accountant received $20,000 to fill half-yearly returns for the year. Since the amount pertains to two returns to be filled every six months, the revenue ($10,000) would be recognized at the end of each six months in the books. The following journal entries will be recorded:

Example #6

On 10th August, a trader received advance payment for goods worth $2,000 to be delivered in a subsequent month. The amount received would be treated as unearned revenue until goods are delivered. Post the delivery. The amount would be recognized as income in books. The following journal entries will be recorded:

The above entries are recorded following revenue recognition. The revenue recognition concept states that the revenue should be recognized when the goods are delivered or services are rendered, and there is a certainty of payment realization. Therefore any unearned income should not be recognized as revenue and should be treated as a liability until the mentioned conditions are fulfilled.

How to Record?

According to the situation and the agreement between the parties, the unearned revenue entry might be different. Let us take different scenarios and discuss how to record them through the discussion below.

- When the unearned revenue is received – In this situation, cash is received, and a current revenue arises. It is recorded as under:

- When the unearned revenue is earned –In this situation, the liability of unearned revenue decreases, and revenue increases, the entry is recorded as under:

The unearned revenue concept is common in industries where payments are received in advance. Some common examples of unearned income are service contracts like housekeeping, insurance contracts, rent agreements, appliance services like refrigerator repair, tickets sold for events, etc.

Recommended Articles

This article has been a guide to what is Unearned Revenue. Here we explain its journal entries, examples, and how to record Unearned Revenues in detail. You can learn more about accounting from the following articles –