Part of our Statistical Concepts guide

What Is Stochastic Process?

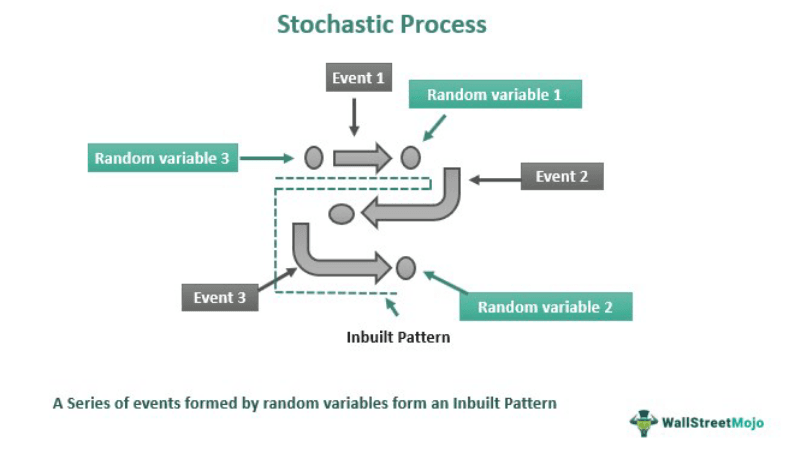

Stochastic process (random process) refers to a series of events where each event through random occurrence has an inbuilt pattern. For example, in the financial world, one uses stochastic models to estimate outcomes in uncertain situations concerning returns on investment, inflation rates, and market volatility.

It is a key tool for traders, planners, portfolio managers, and analysts deciding on investment decisions. One can also use it to know about the performance of an individual security portfolio using probability distributions. The random process showcases data to estimate results that account for a specific degree of randomness or ambiguity. It contains multiple factors to give a variety of outcomes about different situations so that dynamic effects can get recorded.

Key Takeaways

- A stochastic process in finance or a random process is defined as a collection of random variables, with each variable arranged using an inbuilt set of indices representing time.

- Traders apply it to know about the performance of an individual security portfolio using probability distributions on a random basis.

- It has four main types – non-stationary stochastic processes, stationary stochastic processes, discrete-time stochastic processes, and continuous-time stochastic processes.

- It finds various uses in the financial world, which has uncertain nature like securities performance, market volatility, inflation rates, epidemic modeling like in coronavirus, understanding the disease transfer, traffic simulations.

Stochastic Process Explained

A Stochastic process meaning refers to a probability model that describes a set of time-ordered random variables representing the potential impact of a dynamic process in a single instance. Researchers use it to explain all those phenomena that contain random variables of huge amounts but show collective effects like Bernoulli’s or capillary effect.

A stochastic model has the following certain features that separate it from other probabilistic models:

- It must comprise more than one input that reflects the ambiguity of the predicted situation.

- The model must represent comprehensive aspects of a circumstance to predict distribution correctly.

As the model of stochastic contains uncertainty, the results rendered by the model give a good forecast of possible and probable outcomes. Moreover, for estimating all probable outcomes, more than one input should facilitate random variation during a period. Hence, in such situations, various outcomes are shown as a result of a probability distribution based on mathematical functions.

In probability theory, this process is one where chance plays a role. For instance, in the stock market, each stock has a predetermined probability of giving profit or loss at any given time. On the other hand, a stochastic process is more broadly defined as a family of random variables indexed against another variable or group of variables. Thus, it is one of the most broadly applicable areas of probability study.

In an analysis of portfolio investment returns, the stochastic model could estimate all the probability of different returns based on market volatility. It happens because the random variable utilizes time-series data showing contrast observed within historical data during a period. Therefore, multiple stochastic estimations contribute to the final probability distribution reflecting the randomness of inputs.

Types

One can categorize it based on stochasticity or how random variables are generated. Let us discuss the four different types of stochastic processes below:

#1 – Non-Stationary Stochastic Processes

As the name suggests, the random variables have dynamic statistical properties over time.

#2 – Stationary Stochastic Processes

Under it, the random variables have constant statistical properties with time.

#3 – Discrete-Time Stochastic Processes

It comprises random variables in a sequence that contains individual variables with a limited set of values.

#4 – Continuous-Time Stochastic Processes

Under it, a sequence of random variables gets to take values that remain in a continuous range.

Markov processes, Poisson processes, and time series, where the index variable is time, are some fundamental stochastic process types. It doesn’t matter if this indexing is discrete or continuous; what matters is how the variables change over time.

Applications of Stochastic Process

Stochastic programs or processes are dynamics that form as a result of probabilistic variations or fluctuations. It has many applications in the financial sector, characterized by uncertainty in several areas, including securities performance, market volatility, inflation rates, epidemic modeling for diseases like coronavirus, comprehension of disease transmission, traffic simulations, and electrical engineering communications and signal processing. More stochastic processes and their applications are discussed below:

- Many financial planners and managers use it to predict security and market behavior.

- Traffic simulations are done using it.

- One also uses it in epidemic modeling, like in coronavirus.

- It also gets applied in mobile cellular networks, communications, and signal processing of electrical engineering.

- Finding the present guidelines for when and how much to order would be a stochastic process. The corporation would have to modify and reevaluate these procedures until they produce a more favorable result if they are not successful—if a company frequently had too much or too enough inventory.

- In condensed physics, one uses it to describe a phenomenon accurately.

Examples

Let’s take the help of some Random process examples to understand the concept of stochastic processes and their applications.

Example #1

Here, the first example would be those Random Processes with discrete parameters and continuous state space in the securities market. For example, let us take the DOW-Jones Index values after the nth week. Here one has the discrete-time random process having the continuous state space, namely (0, ∞).

When analyzed using probability, such a process gets wide use in making a reasonable decision regarding securities trading. As a result, traders use a random process for ascertaining the best time to trade securities.

Example #2

The second example comprises a bus BlueCouch which takes students to and from the dormitory complex, allowing the student’s union to arrive many times during the day. Bus BlueCouch has an intake capacity of 50 students at one go. If the student’s number is fifty or little lesser, then the bus makes them board it. However, when the number of students exceeds 50, then only fifty students will get to board the bus, and the remaining will wait for the next round of the bus.

One can see that the number of students waiting for the empty bus to board its destination takes the form of a random process. Moreover, when one counts the time of bus arrival, then the number of students in a queue for bus arrival also forms a random process. Furthermore, when one considers the number of students in the queue for a bus at any given the time of day has the continuous space parameter. Hence, in this case, also, the process describes a distinct state of the random process concerning continuous time.

Lastly, in this example, the nth student reaching the bus stop has a certain time associated with them. Thus, the nth student waiting time also forms a continuous-state random process.

Frequently Asked Questions (FAQs)

Is stochastic processes hard?

The random process has wide applications in physics and finance, as the model represents multiple phenomena interestingly. However, the entire random process model gets extremely difficult for a commoner to use in their business or other works.

How does stochastic process work in securities?

In the securities market, it measures price movement momentum as the security price changes before the momentum of the price change its direction. Therefore, it becomes a key trading indicator tool for trend reversal prediction.

What is the difference between random and stochastic processes?

Random does not differ from random process literally. But random means a technique that allows the handling of a random process.

Recommended Articles

This article has been a guide to what is Stochastic Process & its meaning. Here, we explain it in detail with its types, applications, and examples. You may also find some useful articles here –