Part of our Retirement Planning guide

Superannuation Meaning

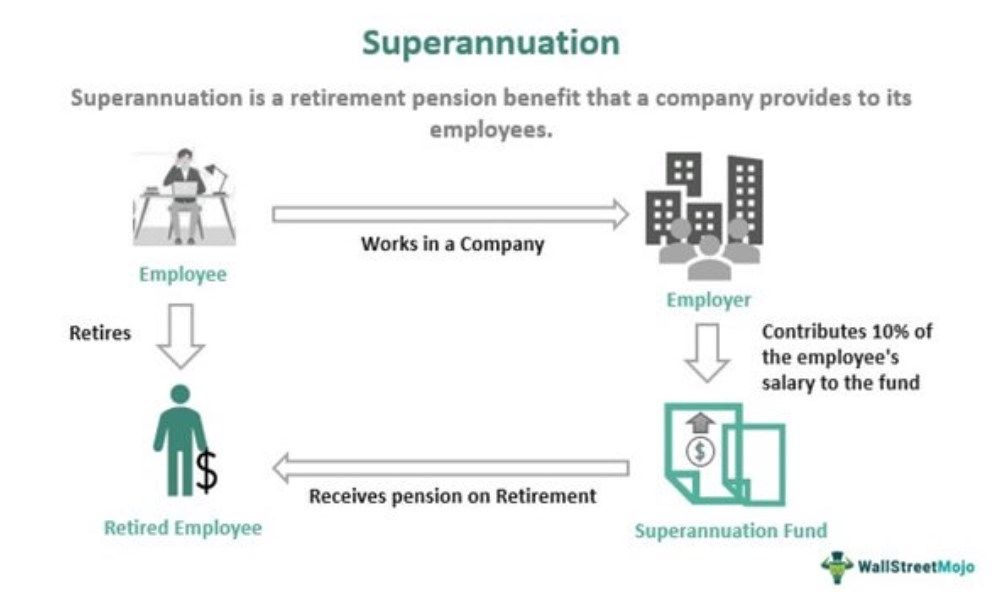

Superannuation (or super) is an employer-sponsored retirement pension plan mandated by the Australian government. Under the scheme, an employer must deposit a pre-determined percentage of employees’ salary in a superannuation guarantee (SG) account until retirement. It provides monetary benefits to employees post-retirement and secures them financially.

Super applies to employees above 18 years who work for more than 30 hours per week and earn beyond $450 per month in Australia. Under the plan, the employer contributes 10 percent of employees’ earnings to a super fund until retirement. The fund invests the amount to earn returns and increase the investment. Employees can withdraw it post-retirement or after attaining the preservation age. It provides tax benefits to both the employer and the employee.

- Superannuation is a retirement benefit that a company offers to its employees. It is primarily used to describe pension plans in Australia.

- In Australia, an employer must make a minimum superannuation contribution of 10% of an employee’s earnings to provide pensions to employees post-retirement.

- Superannuation offers financial security to employees in old age and tax benefits to both the employer and the employee.

- It is comparable to a defined benefit plan, defined contribution plan, or social security system in the US.

- Any person above 18 years, working more than 30 hours per week, and drawing more than $450 is eligible for an SG contribution from the employer.

Superannuation Explained

Superannuation is the benefit an employer provides to an employee upon retirement in the form of a pension every month. The employer deposits a small percentage of the employee’s salary into the SG contributions at regular intervals.

The employer offers it as a reward for the employee’s lifelong services to the company. This money set aside by the employer in the super account grows till the employee’s retirement or withdrawal. As a result, employees enjoy regular income post-retirement. Moreover, it ensures their well-being in old age.

Under Australian law, it is compulsory for companies to contribute to the super account of employees regularly till their retirement. Usually, the employer makes the SG contributions for employees. Thus, the take-home pay of employees remains unaffected. Nevertheless, employees too can make additional voluntary contributions to it.

Access to SG funds depends on an employee’s preservation age and retirement status. Preservation or access age starts at 55 and varies according to the employee’s date of birth.

Employees under 60 must retire permanently and reach their access age to use super funds. However, employees aged 60 to 64 can access the super fund on permanent retirement. At the same time, working employees aged 65 or above have part access to super before retirement.

Eligibility

Only those employees are eligible for SG contributions from employers who are:

- Above 18 years of age

- Gets $450 per month as salary (before tax)

- Employed full-time or part-time

- Temporary or permanent residents

Furthermore, employees under 18 and working 30 hours or more weekly are also eligible for superannuation contributions from the employer. Note that the employer must regularly contribute to the super account until retirement, even if the employee is working after 65 years of age.

Superannuation Rate

Currently, an employer must pay a minimum of 10% of an employee’s ordinary time earnings (OTE) as superannuation. OTE includes payments for an employee’s normal work hours, including commissions, incentives, shift bonuses, and casual loadings. However, it excludes overtime payments.

If a company fails to pay an employee’s minimum superannuation payments timely, it has to pay the superannuation guarantee charge (SGC) as a penalty. The minimum superannuation rate increases by 0.5 % every year. It increased by 0.5% from July 2021 and is likely to reach 12% by 2025-26.

There is a maximum limit to SG contributions by the employer. For the year 2021-22, it is $58,920 per quarter.

Superannuation in Australia and US

Unlike in the US, superannuation is a mandatory requirement in Australia. In the US, superannuation consists of defined benefit plans, defined contribution plans, and social security systems. The defined benefit plan provides a guaranteed fund as a payout to the retiree upon retirement, which is not the case with the super in Australia, where the employer uses the super fund to pay the pensions.

Under the defined contribution plan, employees are the primary contributors to the pension fund created by the government. Contrastingly, the super mandates a minimum 10% contribution by the employer. In addition, the employee in the US can take out retirement corpus before retirement, unlike the Australian rule of super which doesn’t allow doing so.

Calculation Examples

Here are a few superannuation calculation examples to understand the concept better.

Example #1

Suppose Christy, 30 years old, works in a cloth manufacturing company in Australia. She works for 40 hours per week. The following are the details of her wages:

Regular wage earned by Christy from January 2022 to March 2022: $900

Bonus received: $180

Shift loading: $70

Overtime received: $250

Let us calculate the SG contribution by her employer. The employer must include the regular wage, bonus, and shift loading to calculate her OTE and leave out overtime payments.

OTE = regular wage + bonus + shift loading

= 900 + 180 + 70

= $1150

Therefore, the SG contribution by the employer = 10% of OTE

= 0.1*1150

= $115

Hence, her employer would contribute $115 to her super fund account in the first quarter of the year.

Example #2

Let us suppose an Australian employee, Steve, has been working with his employer for the last five years. He is getting $4500 as salary before tax for his weekly 35 hours of duty at the office. He is 25 years of age. Hence, Steve is eligible for SG contribution from his employer.

Therefore, the employer deposits 10% of Steve’s OTE in his super fund account every month. It comes out to be $450. Thus, on retirement, Steve receives his total super fund balance, which is calculated as:

Monthly super fund contribution by the employer: $450

If the total length of his service is 35 years and his OTE remains the same, then

Super contribution by Steve’s employer = $12*450*35

= $189000

The super fund will invest Steve’s money and make it grow over time with investment returns. Depending on the super fund performance, the super account balance will increase. On retirement, Steve will receive the super account balance as a pension.

Benefits

There are numerous superannuation benefits for the employee as below:

- Employees have to pay less income tax.

- The tax on investment returns also gets reduced.

- The insurance coverage becomes cheaper.

- Employees get the total and permanent disability (TPD) insurance cover at no extra cost.

- The super fund is protected against any future bankruptcy of SG contribution.

- The total amount received from the super fund after retirement is tax-free if invested with an Australian retirement trust.

- The Australian government also contributes to the super fund of the employees.

- Many super fund handling companies offer free advice, discounts, rewards, and a venue to invest in valuable securities of big companies.

Frequently Asked Questions (FAQs)

How is superannuation calculated?

Every year the super fund rate is decided by the government of Australia, which is currently at 10%. It means superannuation has to be calculated at 10% of the employee’s ordinary time earnings (OTE). It excludes overtime paid to an employee. After calculating the amount, it has to be contributed to the super fund account of the employee by the employer regularly.

When did superannuation start in Australia?

Until 1976, the super arrangement was not mandatory under law. However, in 1983, the system of compulsory super fund for every Australian employee was conceptualized and enacted with a 3% contribution from the employee and employer upon the total salary. The SG contribution for the aging and retiring population came into existence in 1992 during the government led by Prime Minister Paul Keating.

When is superannuation withdrawal possible?

The super can be withdrawn if an employee is:

• 65 years old and is still working

• 60 years old and retired from service

• Under 60 and has reached access age and is permanently retired

Employees can also access the super in case of extreme financial difficulties or terminal disease.

Recommended Articles

This has been a guide to Superannuation & its Meaning. We explain superannuation guarantee, benefits, calculations along with examples in Australia/US. You can learn more about accounting from the articles below –

Recommended Articles

Continue with these closely related articles from the same guide.