Part of our Retirement Planning guide

Provident Fund Meaning

Provident funds function as retirement savings for private-sector employees and public-sector employees. In many countries, it is mandatory. Both the employer and employee contribute a certain amount to a PF account. When employees retire at 58, they can withdraw savings from their PF accounts.

The government imposes various PF regulations on employers. PFs are further classified into four categories—public, statutory, recognized, and unrecognized. Up to a certain limit, the PF fund is exempt from taxation.

- A Provident fund is a retirement account; the employee and the employer make monthly contributions. Therefore, it is also referred to as EPF (Employee Provident Fund).

- The PF primarily offers retirement benefits to employees. However, it can also act as an emergency fund or a reserve during financial crises. Some firms even allow employees to take a loan against the PF amount.

- In India, new EPF rules were initiated by the Central Board of Direct Taxes (CBDT) on April 1, 2022. By the 2022 regulations, EPF contributions above 2,50,000 Rupees per year will be taxed.

Provident Fund Explained

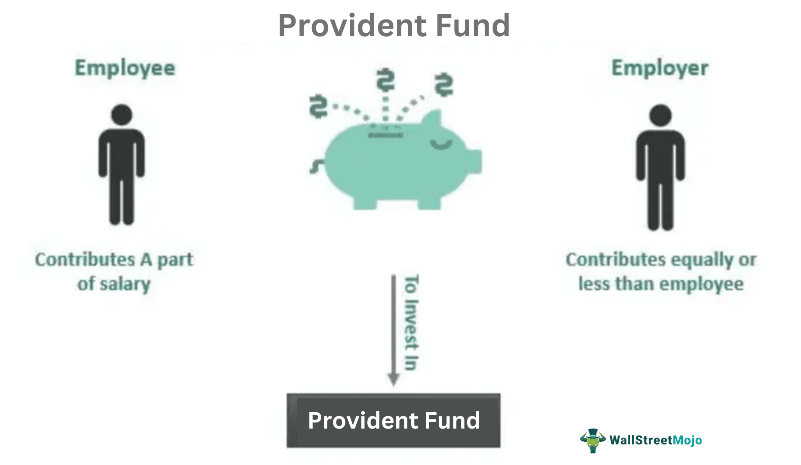

Provident funds (PF) are retirement funds created by employers where employers and employees contribute a certain amount. It is also referred to as EPF (Employee Provident Fund) or PPF (Public Provident Fund).

A portion of an employee’s salary is allocated to the retirement fund, and the employer matches the contribution and allocates an amount from the company’s account. Employees rely on PFs when they retire—at the retirement age of 58.

To receive the PF payout, the employee must show legal documents proving they are of retirement age. In addition, if an employee resigns from a company and joins another, the PF account money is redirected to the new PF account.

For women, EPF deductions are only 8% of the salary for the first three years (instead of 12%). In India, employee contribution towards PF is capped at 15,000 rupees per month.

Types

There are four types of provident funds.

#1 – Recognized

By the income tax act of 1952 and the PPF Act of 1968 in India, PF is considered ‘recognized’ if the firm facilitates PF for a minimum of 20 employees. In addition, the firm requires approval from the PF commissioner of income tax. If the employer contributes more than 12%, PF savings are taxable.

#2 – Unrecognized

Unrecognized PFs do not have any legal backing from the government. The firm completely manages unrecognized PFs.

#3 – Public

The principal target of the PPF is to ensure that the principal amount is secure. It is designed for long-term wealth creation plans; it offers stable returns to investors with a low-risk appetite. PPF is backed by the government and not linked to the market.

#4 – Statutory

It is offered only to government employees working in government or public sector offices; it comes under the purview of the PF Act of 1925.

Statutory PF is offered to employees working in government universities, railways, public sector banks, etc. No private sector employee is eligible for this scheme. The government regulates statutory PF interest rates. And the government regulates its interest rate from time to time.

Example

Now let us look at a provident fund example to understand its real-world applications.

Janet joined a company when she was 20; her initial salary was $90000 per annum. That is, she was paid $7500 every month.

Now, let us assume that Janet works for the same firm till she retires—at age 58. Her monthly remuneration also remains unchanged. In addition, both Janet and her employer make regular contributions toward her PF.

According to the rules, Janet contributes 12% of her salary, and the employer contributes another 12%.

Now, 12% of $7500 = $900

So, Janet’s PF account receives a total contribution of $1800 every month.

After 38 years, the PF principal amount becomes $820,800; interest rates are also accrued. An interest rate of 8.10% is applied to the principal and gets compounded periodically.

Taxation

Now let us look at provident fund taxation:

- In India, new EPF rules were initiated by the Central Board of Direct Taxes (CBDT)—they came into effect on April 1, 2022. As per new rules, EPF contributions above 2,50,000 rupees per year will be taxed.

- If there is no employer contribution to the EPF, the tax-free threshold is set at 5,00,000 rupees per year (beyond that, EPF is taxed).

- From April 2022 onwards, the office of CBDT mandates companies to maintain two separate PF accounts: one for taxable contributions and another for tax-free contributions.

- The excess PF contribution is deposited in a separate account if the tax-free threshold is surpassed. In addition, taxation is applied to accrued interests.

Benefits

The following are the benefits of a provident fund:

- First, it accumulates retirement savings for employees—it is a long-term investment.

- It also doubles up as an emergency fund or reserve. The accumulated savings can be used during financial crises.

- Some firms even allow employees to take a loan against PF savings.

- PF is applicable once an employee surpasses the minimum duration of employment (at the same firm).

Difference Between Provident Fund And Gratuity

- A PF account receives contributions from both the employer and the employee. But, on the contrary, the gratuity does not include any contribution from the employee. Instead, the gratuity is a token monetary amount offered to an employee as an appreciation.

- PF is accounted for tax, but gratuity is exempt from taxation.

- An employee may use the PF for several reasons. In contrast, a gratuity is offered only when an employee retires, suffers a physical injury, or passes away.

Provident Fund vs Pension Fund vs Retirement Annuity

- A PF account receives contributions from an employee and an employer. In contrast, the government pays a pension to public sector employees (as a monthly compensation). A retirement annuity is similar to an IRA. Investors pay a lump sum amount and receive a monthly payment for the rest of their lives.

- Both private and government employees receive PF. In contrast, the pension fund is offered only to government employees. Moreover, unlike PF, retirement annuities are personal savings plans; employers do not play a part.

- EPFs function as retirement accounts, pensions are monthly payments, and the retirement annuity works like an insurance contract.

- The pension scheme is based on the duration of employment. In contrast, the EPF and annuity are based on total contribution.

Frequently Asked Questions (FAQs)

1. How is a provident fund calculated?

The employee contributes 12% of a company, and the employer matches it with another 12%. However, this 12% is subject to the employee’s basic pay. This contribution is made monthly, and the employee only receives the deducted salary.

2. How to claim provident funds?

To claim the PF amount, the employee has to declare unemployment. Employees who serve only one month can withdraw up to 75% of the PF balance. The remaining 25% is added to the PF contribution made by the next employer. The Employee PF Act of 1952 states that employees can withdraw 100% of PF savings upon retirement.

3. Are provident funds taxable?

PF taxation varies for each country. For example, in India, new EPF rules were initiated by the Central Board of Direct Taxes (CBDT) on April 1, 2022. By the 2022 regulations, EPF contributions above 2,50,000 Rupees per year will be taxed.

Recommended Articles

This article has been a guide to Provident Fund and its meaning. Here, we explain its example, benefits, taxation, and comparisons with gratuity and pension funds. You can learn more about it from the following articles –