Part of our Accounting Concepts guide

Accounting Scandals Meaning

Accounting scandals refer to instances of fraudulent or unethical financial practices within a company’s accounting and reporting systems. These scandals often involve the manipulation of financial statements, concealing liabilities, inflating revenues, or misrepresenting the financial health of a business. Such misconduct can have severe consequences, including misleading investors, creditors, and regulatory authorities.

Some major accounting scandals in the past, such as the Enron scandal, have led to corporate bankruptcies and significant financial losses for stakeholders. These incidents underscore the importance of transparent and ethical financial reporting, as well as the need for robust regulatory oversight to prevent such malpractices and maintain trust in the financial markets.

Accounting Scandals Explained

Accounting scandals are events marked by fraudulent or unethical financial activities within a company’s accounting and reporting processes. The biggest accounting scandals involved the deliberate manipulation of financial records, with the aim of concealing debts, exaggerating revenues, or distorting the actual financial health of an organization. They can have far-reaching consequences, both for the companies involved and the broader financial landscape.

Accounting scandals erode trust in financial reporting, and they can severely impact investors, creditors, and the market as a whole. For instance, the Enron scandal in the early 2000s resulted in the bankruptcy of a major corporation and substantial financial losses for its shareholders, shaking confidence in corporate accounting practices.

Several factors can contribute to accounting scandals, including a lack of transparency, weak internal controls, pressure to meet financial targets, and, in some cases, unethical leadership. Regulatory bodies and financial standards organizations, like the SEC and FASB in the United States, have since implemented more stringent regulations and accounting standards to prevent such malpractices and improve financial transparency.

Public awareness of accounting scandals underscores the importance of ethical financial reporting, accurate record-keeping, and the necessity for a robust system of checks and balances in the corporate world. The consequences of such scandals are a stark reminder of the need for ongoing vigilance and regulatory oversight to maintain the integrity and trustworthiness of financial markets.

Causes

Major accounting scandals can result from various factors, often stemming from a complex interplay of financial, ethical, and organizational issues. These include:

- Pressure to Meet Financial Targets: Companies may face immense pressure to meet revenue and profit targets, leading to a temptation to manipulate financial statements to achieve these goals.

- Weak Internal Controls: Inadequate internal control systems can create opportunities for financial irregularities to occur without detection.

- Unethical Leadership: A corporate culture that tolerates or even encourages unethical behavior, starting from top management, can contribute to accounting scandals.

- Complex Accounting Rules: The complexity of accounting standards can provide a cover for fraudulent activities and make it challenging for stakeholders to detect irregularities.

- Incentive-Based Compensation: Compensation structures that tie executive pay to financial performance can incentivize unethical practices to boost earnings and share prices artificially.

- Lack of Transparency: A lack of transparency in financial reporting can obscure the true financial health of a company, making it easier to manipulate financial statements.

- Auditor Conflicts of Interest: Conflicts of interest between external auditors and the companies they audit can compromise the independence and thoroughness of audits.

- Inadequate Regulatory Oversight: Weak regulatory oversight and enforcement can create an environment where companies feel they can engage in unethical practices without significant consequences.

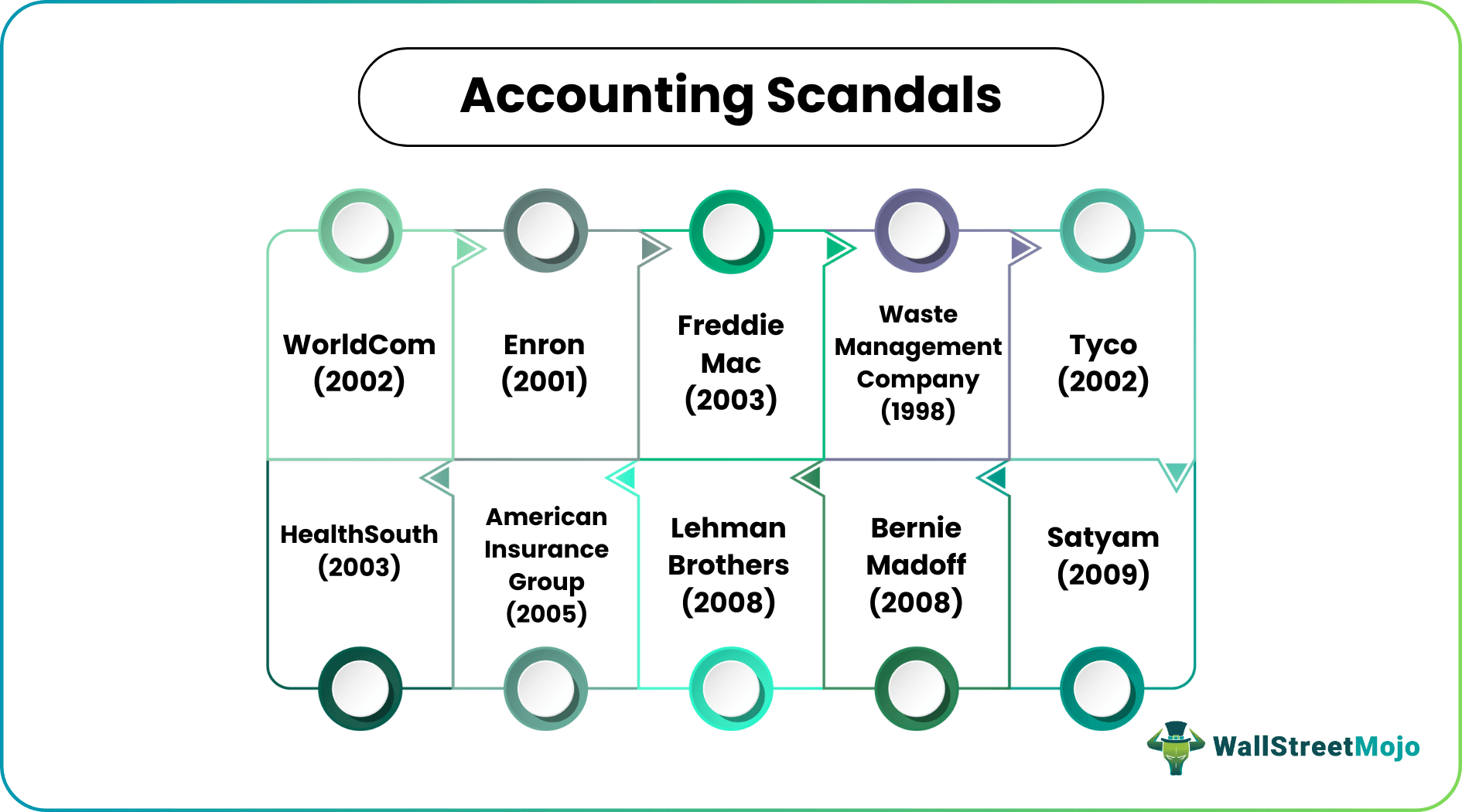

List of Top 10 Scandals

The world’s biggest accounting scandal is of Enron, once one of the largest companies in the world, which faked its accounting statements by using the mark to market strategies, and it took down Arthur Andersen with it (which is now Accenture)

Let us discuss the top 10 such scandals of all time and how these companies manipulated their financial statements.

- WorldCom (2002)

- Enron (2001)

- Waste Management CompanyCompany (1998)

- Freddie Mac (2003)

- Tyco (2002)

- HealthSouth (2003)

- Satyam (2009)

- American Insurance Group (2005)

- Lehman Brothers (2008)

- Bernie Madoff (2008)

Let’s discuss each one of them in detail –

#1 WorldCom (2002)

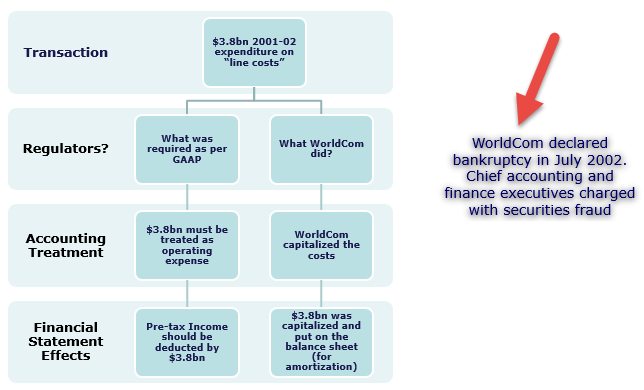

This accounting scandal occurred in the year 2002. WorldCom was a telecommunication company. The name of WorldCom has not changed; it is MCI, Inc. now. The fraud happened due to the inflated assets of the company. Then CEO Bernie Ebbers didn’t report the line costs by capitalizing,and he also inflated the company’s revenues by recording fake entries. As a result, 30,000 people lost their jobs, and investors lost around $180 billion. The internal audit team of WorldCom found out $3.8 billion fraud. After the fraud was discovered, WorldCom filed for bankruptcy, and Ebbers got a sentence of 25 years.

#2 Enron (2001)

source: nytimes.com

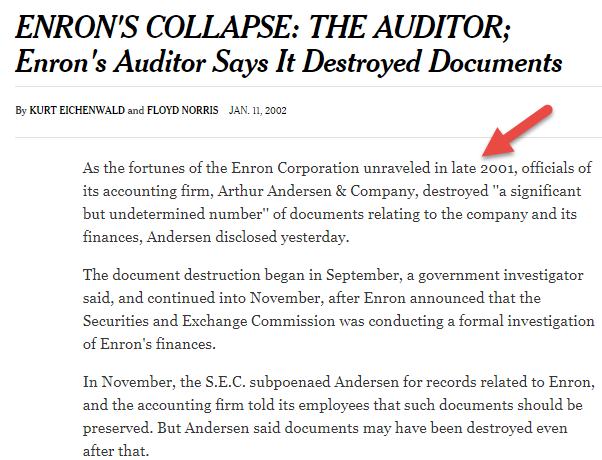

This accounting scandal happened in the year 2001. Enron, a commodity and energy-based service company, was in trouble for removing a massive amount of debt from its balance sheet. As a result, the shareholders of Enron lost $74 billion. Many employees lost their jobs. Many investors and employees lost their retirement savings. It is one of the most cited accounting scandals of all time. It was the work of then CEO Jeff Skilling and former CEO Ken Lay. Ken Lay died even before serving time. Jeff Skilling was imprisoned for 24 years. Enron filed for bankruptcy and found that Arthur Anderson was also guilty of falsifying Enron’s accounts. Sherron Watkins had acted as an internal whistleblower. And the suspicions increased as Enron’s stock price increased.

Do have a look at this article on Capitalization vs Expensing to learn more

#3 Waste Management Company (1998)

source: nypost.com

This accounting scandal happened in the year 1998. Waste management company reported around $1.7 billion in fake earnings. They deliberately increased the time period of depreciation period of their plant, equipment, and property. While the new CEO, A. Maurice Meyers, and his team members went through the books of accounts, they found out about this unprecedented scenario. Arthur Anderson had to pay $7 million as a penalty to the Securities and Exchange Commission (SEC), and the shareholder class-action suit settled for $457 million. After all was settled, the CEO, A. Maurice Meyers, started an anonymous hotline so that the employees could spread the word about any dishonest or improper matter happening in the organization.

#4 Freddie Mac (2003)

source: nytimes.com

This accounting scandal occurred in 2003. It was a mortgage finance giant, and it had massive backing from the Federal Reserve. The scandal was enormous. The earnings of $5 billion were intentionally understated. The whole plan was executed by the CEO, COO, and ex-CFO of the company. While investigating, the SEC found out the fraud. Freddie Mac needed to pay $125 million in fines, and the CEO, COO, and ex-CFO were fired from the company. After a year, the most surprising thing is that another federally backed mortgage finance company was caught in a similar sort of scandal.

#5 Tyco (2002)

source: nytimes.com

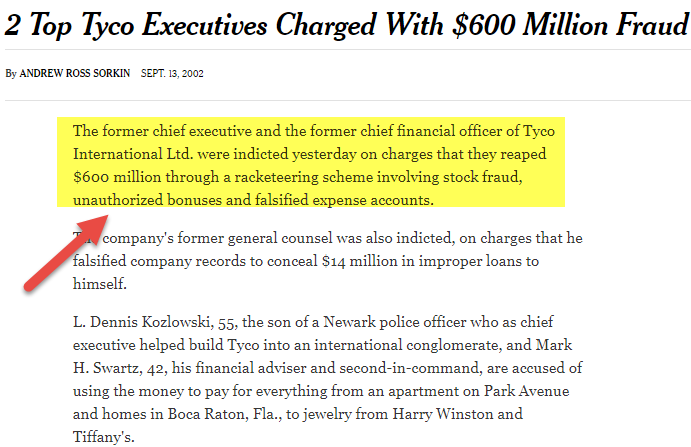

This accounting scandal occurred in the year 2002. Tyco was a Swiss security systems company. The CEO and CFO inflated the company’s income by $500 million so that they could steal $150 million. They did this through fraudulent stock sales and unapproved loans. Securities and Exchange Commission (SEC) and Manhattan D.A. found out about questionable practices in accounting,and that’s how the whole thing got attention. The CEO and CFO got a sentence of 8 to 25 years, and Tyco had to pay $2.92 billion to investors due to the lawsuit.

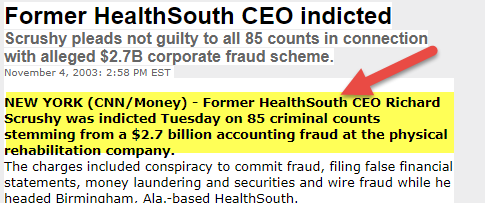

#6 HealthSouth (2003)

source: money.cnn.com

This accounting scandal happened in the year 2003. It was the largest publicly traded healthcare by then. The income was inflated by a whopping $1.4 billion so that they could meet the shareholders’ expectations. The main culprit behind this accounting scandal was the CEO, Richard Scrushy. The SEC found out that the company sold $75 million of shares in a single day after a huge loss. The penalty was 7-year imprisonment. The fascinating thing about Richard Scrushy is that he now works as a motivational speaker!

#7 Satyam (2009)

This accounting scandal occurred in the year 2009. It was an Indian IT and back-office accounting services firm. The fraud was of a huge $1.5 billion. The Founder & Chairman of the company, Ramalinga Raju, was the main player behind this fraud. He inflated the revenue and reported the same in his letter to the board of directors. The CBI couldn’t file charges on time, and he was not charged. A hilarious part is that in the year 2011, his wife published his book on poetry on existentialism.

#8 American Insurance Group (2005)

This accounting scandal occurred in the year 2005. As the name suggests, the American Insurance Group was a multinational insurance company. The fraud was massive. The fraud was about $3.9 billion. The complaints were that this huge sum of money was alleged, and there was also manipulation of the stock price and bid-rigging. The person responsible for the fraud was the CEO, Hank Greenberg. The CEO was fired, and AIG had to pay $10 million to SEC in 2003 and $1.64 billion in 2006. It was unknown how the SEC found out, but possibly a whistleblower hinted it to the SEC.

#9 Lehman Brothers (2008)

source: nytimes.com

This accounting scandal happened in the year 2008. It was another most cited scandal in the history of accounting fraud. Lehman Brothers was a global financial service provider. The actual fraud was done by hiding the losses of around $50 billion in sales. When the company went bankrupt, the actual scenario got public. The key players were the executives of Lehman Brothers and also the auditors of Ernst & Young. They sold toxic assets to Cayman Islands banks to showcase that they had $50 billion more in cash. The SEC couldn’t prosecute them due to a lack of evidence.

#10 Bernie Madoff (2008)

This accounting scandal happened in the year 2008. It was a Wall Street investment firm. The fraud was one of the largest frauds in the history of accounting frauds. They tricked the investors out of $64.8 billion via the most prodigious Ponzi scheme ever. The main players were Bernie Madoff himself, his accountant, David Friehling, and Frank DiPascalli. The investors received payouts from their own money or from other investors’ money, not from the company’s profits. Madoff’s sons informed the SEC about the scheme after he told them, leading to his capture. The court sentenced Madoff to over 150 years in prison and ordered him to pay $170 billion in restitution. His partners also got imprisonment.

How To Avoid?

To avoid major accounting scandals, organizations should implement a range of preventative measures. Let us discuss a few of them through the points below.

- Ethical Leadership: Cultivate a culture of ethical behavior starting from top leadership, emphasizing integrity in financial reporting.

- Transparency: Maintain transparency in financial reporting, providing stakeholders with clear, accurate, and complete information.

- Strong Internal Controls: Implement robust internal control systems to prevent unauthorized access and manipulation of financial data.

- Independent Audits: Engage independent external auditors who are not influenced by the organization’s management to perform thorough and unbiased audits.

- Regulatory Compliance: Adhere to all relevant financial regulations and accounting standards, ensuring compliance in both letter and spirit.

- Whistleblower Protection: Establish channels for employees and stakeholders to report concerns about unethical practices without fear of retaliation.

- Regular Training: Provide ongoing training to employees on ethical conduct, financial reporting procedures, and the consequences of fraudulent activities.

- Risk Assessment: Continuously assess financial and operational risks, addressing them proactively to prevent potential issues.

- Audit Committee Oversight: Appoint an effective audit committee to oversee the financial reporting process and provide an additional layer of accountability.

Recommended Articles

This has been a guide to Accounting Scandal and its meaning. Here we explain its causes, list of top 10 scandals across the world, and how to avoid them. You may also have a look at the following articles to learn more about Financial Analysis