What Is The Enron Scandal?

The Enron Scandal involves Enron duping the regulators by resorting to off-the-books accounting practices and incorporating fake holding. The company utilized special purpose vehicles to hide its toxic assets and large debts from the investors and creditors.

The Enron corporation was formed to merge Houston’s natural gas company and inter-north incorporation. After the merger, it grew rapidly and was regarded as the most innovative company. However, it resorted to bad accounting practices. It was involved in the creation of special purpose vehicles, utilized to hide the rising debt of the Enron incorporation, which led to the business’s failure and downfall.

Key Takeaways

Enron Scandal Explained

The Enron corporation and its management resorted to an evil scheme and malpractice of the off-balance-sheet mechanism. It created a special economic vehicle to hide the massive debt from its external stakeholders, namely creditors and investors. The special purpose vehicle was utilized to conceal the realities of accounting rather than focus on the operating results.

The corporation transferred some portion of assets that had rising marketable value to the special economic vehicle, and in return, it took cash or notes. The special purpose vehicle then utilized such stock to hedge an asset present on its balance sheet of Enron. It ensured that a special purpose vehicle reduced the counterparty risk.

The formation of the special purpose vehicles cannot be termed illegal, but compared with the securitization techniques relating to debt, it could be termed as bad. Enron disclosed the existence of special purpose vehicles to the investors and the public, but few people understood the complexity of transactions done using the special purpose vehicles.

Enron assumed that the stock prices would continue to appreciate and that they would not deteriorate or fail as hedge funds. The primary threat was that the special economic entities were capitalized with only the corporation’s stock. If the corporation is compromised, then the special economic entities won’t be able to hedge the deteriorating market price of such stocks. Additionally, the Enron corporation had held significant conflicts of interest concerning the special purpose vehicles.

Causes

Though every step that the Enron Corporation took went against it, there were specific reasons that made it worse for the business.

Let us have a look at them:

- The creation of a special purpose vehicle for concealing financial losses and a pile of financial debt;

- Mark-to-market accounting as an accounting concept is an excellent method to value securities, but such a concept becomes a disaster when applied to the actual business.

- Lapse of corporate governance in Enron Corporation.

Mark To Market (MTM)Accounting in Enron Scandal

The CEO of Enron corporation Jeffrey Skilling transitioned the accounting practice of the Enron corporation from a historical cost accounting method to a mark to market accounting method. Mark to market accounting is a practice that reports the fair market value of the liabilities and assets for a given duration or financial period. The transition of the accounting practice received approval from the securities and exchange commission in 1992.

The mark to market gives insights into an institution and is regarded as a legitimate practice. The method, however, is also exposed to some form of manipulation. The Mark to market is based on fair value rather than taking up the actual value. It caused the business to fail miserably as they reported the expected profits as the actual profits.

Rise

The scandal began with Enron’s misdeeds in the video rental chains. The business collaborated with a blockbuster to penetrate the VOD market. After entering the market, the business overstated the earnings basis for the growth of the VOD market.

The business executed $350 billion in trades, but it did not last long as the dot com bubble came in. It spends a significant amount on broadband projects, but the business could not recover costs from the spending made. The company was exposed to massive exposures, and investors lost money as market capitalization deteriorated.

In 2000, the business started to crumble. CEO Jeffrey Skilling concealed all financial losses resulting from the trading business and broadband projects by applying the accounting concept of mark-to-market accounting. The company kept building assets. It reported profits that were yet to be earned. If the actual profit earned were less than the reported earnings, the loss was never reported. Additionally, the business transferred the asset to the off-the-books corporation. Like this, the corporation concealed its losses

To add to the agony, the chief financial officer of the business Andrew Fastow deliberately resorted to the plan that displayed that the business was in good financial shape even though its subsidiaries lost many investors’ money.

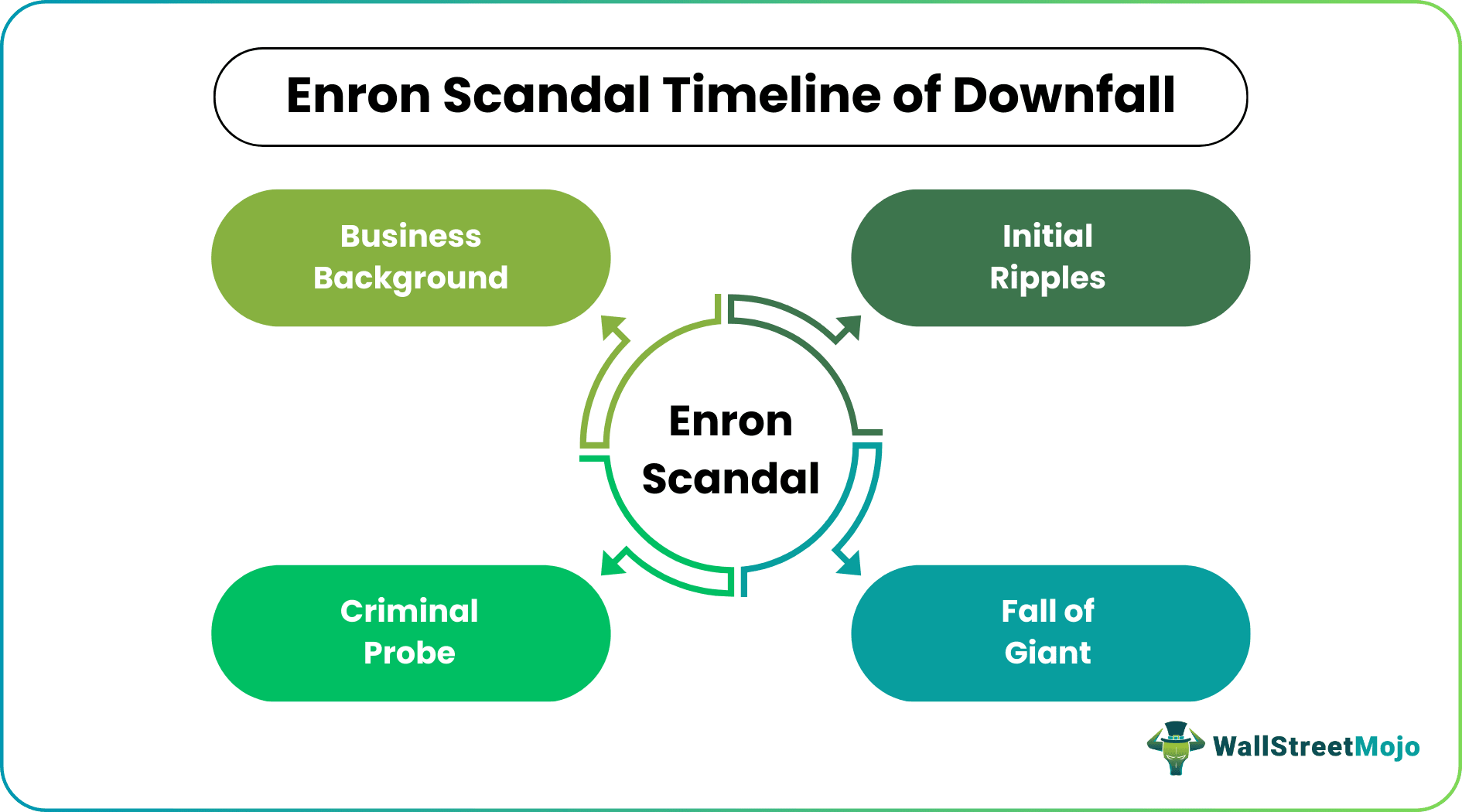

Summary With Timeline

The Enron corporation was regarded as a corporate giant. The corporation had massive debts in its name. It tried to conceal these with the help of special economic entities and special purpose vehicles. But after a good run, it failed miserably and ended up as a bankrupt business. The failure and bankruptcy of the Enron Corporation jolted Wall Street and put several employees on the verge of a financial crisis. Enron traded at the highest market price of $90.75 on December 2, 2001. And when the accounting scandal emerged, stock prices went down to a record low of $0.26 per share.

The summary along with the timelines is as follows:

#1 – Business Background

The year was 1985, and Enron was incorporated as Houston Natural Gas company, and Internorth Ince merged. In 1995, the business was recognized as the most innovative business by Fortune, and it made a successful run for the next six years. In 1998, Andrew Fastow became the CFO of the business, and the CFO created SPVs to conceal the financial losses of Enron. During the period 2000, the shares of Enron traded at the price level of $90.56.

#2 – Initial Ripples

On February 12, 2001, Jeffrey Skilling came in place of Kenneth as a chief executing officer. On August 14, 2001, Skilling abruptly resigned, and Kenneth took over the role again. Same period, the broadband division of the business reported a massive loss of $137 million, and the market prices of stock fell to $39.05 per share. In October, the CFO’s legal counsel instructed auditors to destroy the files of Enron and asked to maintain only the utility or necessary information. The business reported a further loss of $618 million and a write-off of $1.2 billion. The price of the stock deteriorated to $33.84.

#3 – Fall of Giant

On October 22, the business got under a probe by the securities and exchange commission. With this news, the stock of Enron further deteriorated and was reported at $20.75. In November 2001, the business, for the first time, admitted and made the revelation that it had inflated its income levels by $586 million. Also that it has been doing so since 1997. On 2nd December 2001, the business filed for bankruptcy, and the stock prices ended up flat at $0.26 per share.

#4 – Criminal Probe

On January 9, 2002, the justice department ordered a criminal proceeding against the business. On January 15, 2002, the NYSE suspended Enron, and the accounting firm, along with Arthur Andersen, was convicted of obstruction of justice.

Importance

The Enron scandal is significant in learning perspectives for both new financial professionals and experienced professionals. The scandal tells us why strong corporate governance is the key to success for any business to sustain and drive profitable business. Additionally, it draws insights into how accounting policies should not be used and applied. Any misuse can have drastic results or impacts on the business’s health.

Due to the bankruptcy, employees lost several perks and pension benefits. Many came on the verge of a financial crisis. The crisis was so deep that the business shareholders lost an estimated value of $74 billion. Such corporate fraud should be taken as learning, and an understanding should be drawn as to why regulations and compliance are necessary.

Recommended Articles

This article has been a guide to what is the Enron Scandal. Here, we explain the concept with its causes, rise, importance, and summary with timeline. You can learn more about it from the following articles –