Part of our Accounting Concepts guide

What are the Steps in the Accounting Process?

The accounting process is the series of steps followed by the business entity to record the business financial transactions that include steps for collecting, identifying, classifying, summarizing, and recording the business transactions in the books of accounts of the company so that the financial statements of the entity can be prepared. The profits and the business’s financial position can be known after regular intervals of time.

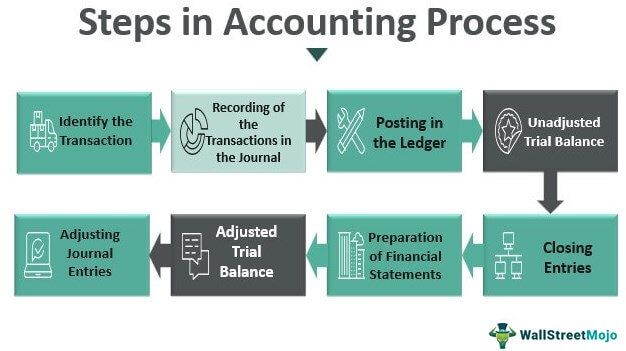

Steps in Accounting Process

The various steps of the accounting process are:

#1 – Identify the Transaction

Identifying the business transaction is the initial step in the process of accounting. The business entity has to identify financial and monetary transactions. Therefore, only those transactions that are monetary are recorded. Also, the transactions that belong to the business are to be recorded, and not the owner’s transactions are included in the books of accounts of the business.

#2 – Recording of the Transactions in the Journal

After identifying the transactions, the second step of the accounting process is to create the Journal entry for every accounting transaction. The point of recording transactions is based on the policy followed by the entity for accounting, i.e. accrual basis or cash basis of accounting. In the accrual basis of accounting, the revenues and expenses are recorded in the entity’s books in the period when they are earned and incurred, respectively, regardless of the actual cash receipt and payment. However, in the case of cash accounting, the transactions are recorded only when the actual cash is received/paid. In a dual entry system, every transaction affects at least two accounts, i.e., one account is debited, and another account is credited. For example, if the purchases are made in cash, the purchases account will be debited (purchases increase), and the cash account is credited (cash decreases).

#3 – Posting in the Ledger

After recording the transaction in the Journal, the individual accounts are then posted in the general ledger. t helps the owner/accountant know each account’s balance individually. For example, all the debits and credits of the bank account are transferred to the ledger account, which helps to know the increase and decrease in bank balance during a period. Finally, we can determine the ending bank balance from it.

#4 – Unadjusted Trial Balance

The company’s trial balance is prepared to check whether the debits are equal to the credits or not. The trial balance’s main purpose is to identify any errors made during the above process. The trial balance reflects all the accounts balances at the given time. After the preparation of the trial balance, it is checked that the total of all credits is equal to the total of all debts, and if the total is not the same, then an error is to be identified and corrected. There can be other reasons for the error, but firstly, an accountant tries to locate the error by preparing the trial balance. Also, trial balance helps to know the balances of all accounts in a summarized form.

#5 – Adjusting Journal Entries

When the accrual basis of accounting is followed, some of the entries are to be made at the end of the accounting year, such as entries of expenses that may have been incurred but are not booked in the Journal and entries of some income that may be earned by the business but are not yet recorded in the books. For example, the interest amount on a fixed deposit is earned each year, but it is accumulated in the fixed deposit amount. This interest income is to be recorded in the books of accounts yearly because the interest is earned yearly, no matter the amount will be received together after the maturity of the fixed deposit.

#6 – Adjusted Trial Balance

After all the adjusting entries are made, again, a trial balance is to be prepared before preparing the financial statements to check that all the credits are equal to the debits after the adjustment entries are made.

#7 – Preparation of Financial Statements

After all the above steps are completed, the financial statements of the company are prepared to know the actual financial position, the profitability position, and the cash flow position of the business. The statements that are prepared for knowing the above positions are a statement of profit and loss for knowing the profitability position, the balance sheet for getting the financial position, and the cash flow statement to know the changes in cash flows from the three activities of the business (operating, investing and financing activities).

#8 – Closing Entries

Finally, the accounting cycle ends with this step. These entries transfer the temporary account balances to a permanent account. The temporary accounts are the accounts whose balances end in a single accounting year, such as sales, purchases, expenses, etc. These balances are first transferred to the income statement and then to the permanent account, i.e., the profit/loss is transferred to the retained earnings account. It should be cleared that only temporary accounts are closed, not the permanent ones (accounts that are balance sheet accounts such as fixed assets, debtors, inventory, etc.)

After closing entries are made, the trial balance is again prepared to check that the debit equals the credit, and the accounting cycle starts again with the beginning of another accounting year.

Conclusion

Thus, the accounting process includes the steps that are to be followed for recording, classifying, summarizing, etc. the financial transaction of the business where the process starts with identifying the transaction and ends mainly with the preparation of financial statements that are finally used and evaluated by the users of the business.

Recommended Articles

This has been a guide to Steps in the Accounting Process and its definition. Here we discuss the eight important steps of the accounting process. You may learn more about financing from the following articles –

Recommended Articles

Continue with these closely related articles from the same guide.