Part of our Accounting Concepts guide

What Are Accounting Errors?

Accounting Errors refer to the common mistakes made while recording or posting accounting entries. These discrepancies are not fraudulent or intentional. . Companies can easily identify these mistakes while tallying accounts and can rectify them as soon as they are detected.

Accounting errors arise out of mistakes related to accounting principles or clerical errors. These are different from the accounting records tampered with to serve individual interests or selfish motives. These errors are usually noticed while discrepancies are observed in the data recorded or being tallied.

Accounting Errors Explained

Accounting errors definition refers to unintentional mistakes that occur while accounting professionals record or account for data. It does not arise because of the selfish motives of the employees or the company itself. It just happens because of clerical mistakes or any recording error.

These errors are not counted as frauds, which occur due to intentional tampering with the data. In fact, these mistakes are identified as and when a discrepancy is noticed in the financial statements or account books. As soon as the error is identified, the accounting professionals take care of it then and there.

Sometimes, there is a missing entry or a duplicate entry that results in accounting errors. Apart from these, there are other forms of common errors that arise. However, identifying and rectification of these errors is easy when accounting professionals are a bit careful while recording the transactions.

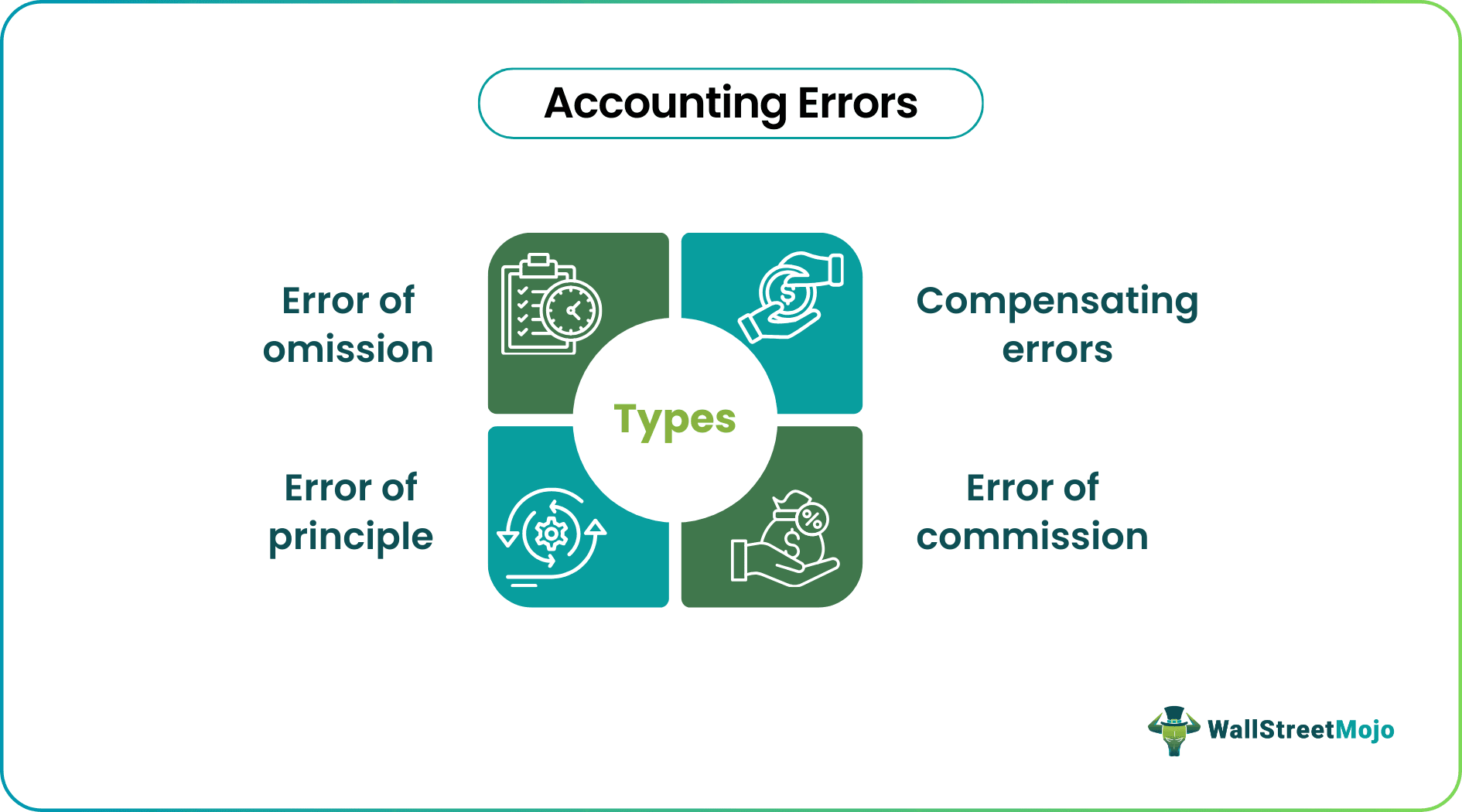

Types

Based on the causes, the accounting errors are divided into following categories:

#1 – Error of Omission

An error of omission is a business transaction or event not recorded in the books of accounts by mistake. Further classifications of Error is Omission are:

a) Error of Full Omission

Where a transaction is not recorded in Journal or not at all posted in the respective ledger accounts.

b) Error of Partial Omission

However, a transaction recorded in the primary book or Journal omitted to post in either one of the ledgers is called Partial Omission.

#2 – Error of Principle

An error of Principles happens when a fundamental accounting principle is violated while recording financial transactions. This error occurs when:

- Revenue expenditure / Incomes are treated as Capital Expenditure / Incomes or vice versa;

- Operating Expenses / Incomes classified as Non-operating expenses / Incomes or vice versa;

- Personal Expenses are considered as Business Expenses or vice versa;

#3 – Error of Commission

This error refers to the transaction recording with the wrong amount or in the wrong account.

#4 – Compensating Errors

These errors occur when the effect of one transaction offsets the effect of another and nullifies the final effect on the Trial Balance.

Causes

Some of the common causes of accounting errors include the following:

- The lack of knowledge of the accounting professionals or those recording the data may be the cause. There are instances where the professional is not sure where to enter the data in the book of accounts.

- Being careless makes even the minutest errors to go unnoticed.

- The system or server errors may restrict the data to be recorded, which might lead to missing entries.

- Internal checking may have been delayed or ignored, leading to such errors.

How To Find?

before rectifying these errors, it is important to detect these errors. Listed below are some of the ways to identify these accounting errors. Let us have a look at them:

- It is important to have an audit trail whereby firms can narrow down the transactions and check for mistakes.

- Have a consistent process of detecting accounting mistakes that might occur from time to time.

- After recording the transactions/data, double-checking the same is recommended.

- Regular reconciliations are a must.

Examples

Let us consider the following instances to understand the accounting errors definition in detail and also check the way to rectify it:

Example 1 – Error of Omission

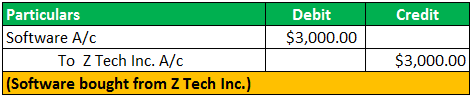

For example, ABC Inc. bought a new software worth the US $ 3000.00 from Z Tech Inc. for business purposes but accidentally forgot to enter it in the books of accounts.

Or, ABC Inc. posted the following entry to record the above transaction in the Journal.

However, the company forgot to post the recorded amount in respective ledgers, i.e., Software A/c and Z Tech Inc. A/c by the US $ 3000.00, classified as an error of complete omission.

In the above example, however, Partial Omission happens if the software purchase from Z Tech Inc. is posted in Software Ledger A/c but forgotten to post in Z Tech Ledger A/c. This exemplifies partial omission instance.

Example 2 – Error of Principle

For instance, ABC Inc. is in the business of trading Furniture. The company bought new furniture for US $ 5000.00 to resell. However, the accounts executive at ABC Inc. accidentally debited the Furniture A/c (as an asset – capital expenditure) instead of Purchases A/c (as an inventory – Revenue Expenditure).

As the company is in the business of trading furniture, the purchase of furniture is a revenue expenditure. It should be debited in the Purchase A/c instead of the Furniture account.

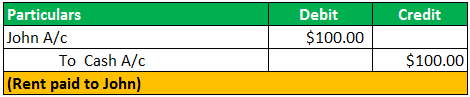

Example 3 – Error of Commission

The following examples are the occurrence of the error of commission:

- Recording the wrong amount in the correct books of accounts

Rent of US $ 100.00 paid to John gets recorded as

- Posting the wrong amount in the correct ledger account

Rent of US $ 100.00 paid to John gets recorded in the credit side of cash A/c as

- Posting the correct amount in the wrong account

Say Rent of US $ 100.00 paid to John gets recorded as:

- Posting the correct amount on the wrong side

Salary paid of US $ 1,000 gets recorded in the credit side of the salary account for the US $1,000. - Posting the same amount twice in the Ledger

Commission of US $ 200 received from Tony gets recorded twice in the commission account. - The wrong casting of the subsidiary books accounts

This accounting error happens in the totaling of the subsidiary books.

Example: The total of the debit side of the Machine Account, which is the US $ 5,050.00 gets recorded as the US $ 5,005.00 - Wrong balancing of the ledger accounts

This error may cause the short or excess balance in ledger accounts

Example 4 – Compensating Error

For instance, ABC Inc. received the US $ 10,000 from Mark and paid US $ 1,000 to Jim. Now, if Mark A/c got credit by the US $1000 and Jim’s A/c got debit by the US $ 10,000, in such a case, an excess debt of US $ 9,000 will get nullified by short debit by the US $ 9,000. In this case, the trial balance will agree.

Example #5

According to a report published in June 2026, Hub Group, a leading provider of transportation services, faced a securities class action lawsuit alleging accounting-related issues in its financial reporting. According to the lawsuit, the company made false or misleading statements regarding its financial health during the period from April 28, 2023, to May 11, 2026. Following these developments, the company’s stock price declined significantly.

This example highlights the importance of regularly reviewing financial records and maintaining strong internal controls to identify and correct accounting errors before they escalate into significant legal, financial, or reputational issues.

Impact

If the trial’s total debit and credit side do not agree in bookkeeping, some accounting error might occur, leading to disagreement. However, some errors do not affect the trial balance agreement yet may have been incurred. Thus it is important to understand the impact of accounting errors on Trial Balance.

| Accounting Errors | Impact on Trial Balance (Total will Agree or not) |

|---|---|

| Error of Principle | Agree, as both the debit and credit side gets recorded in the books of accounts; however, the nature of the transaction has altered. |

| An error of Complete Omission | Agree, as both the debit and credit balances are not recorded |

| An error of Partial Omission | Disagree, as either debit or credit transaction is omitted |

| Compensating Errors | Agree, as the effect gets nullifies |

| Error of Commission | |

| Recording the wrong amount in the correct books of accounts | Agree, as the same wrong amount is entered on both sides |

| Posting the correct amount in the wrong account | Agree, as the correct amount is recorded on the correct side (debit/credit) but in the wrong Ledger a/c |

| Posting the wrong amount in the correct ledger account | Disagree due to a mismatch of the amount in either of the Ledger |

| Posting the same amount twice in the Ledger | Disagree, due to dual reporting |

| The wrong casting of the subsidiary books | Disagree, due to a mismatch in totaling and balancing |

| Wrong balancing of the ledger accounts |

How To Correct?

Accounting errors and corrections should be a consistent affair. So, if the error has already occurred, here are the ways to correct and prevent it:

- Undergo regular checks and reconciliation to make sure there is no discrepancy. Internal checking helps rectify issues before they come to the notice of the external audit team.

- Deployment of sound software solution that eradicates the chances of human errors.

- Be careful while recording transactions and data. A little carelessness leads to major errors.

Recommended Articles

This has been a guide to what are Accounting Errors. We explain its types, how to correct it, causes, examples, and how to prevent & impact the trial balance. You can learn about accounting from the following articles –

Recommended Articles

Continue with these closely related articles from the same guide.