What Is Convertible Preferred Stock?

Convertible preferred stocks are a special class of stocks issued by the company, giving the investor the right to convert its preferred stock holding into fixed shares of company common stock after the predetermined period. Convertibles preferred are hybrid instruments with bond and equity-like features, equivalent to bonds with fixed dividend payment plus the option to acquire common stock.

Thus, due to the above feature, these stocks allow investors to earn a better return than any fixed-income security. The conversion is primarily based on the shareholder’s request but may sometimes be on a compulsory basis, enforced by the organization itself. These stocks give shareholders a fixed income and preference over common stockholders.

How Does Convertible Preferred Stock Work?

The convertible preferred stocks are an impoertnat metd in which companies raise funds to finance their daily operations, investment opportunities, growth and expansion. The convertible preferred stock list is a very widely used method when a business wants to avoid taking debt which put a repayment obligation on the business. This method ensures fund is raised, without being too much leveraged at the same time, not diluting the comm stock holdings all at once.

It is ultimately a type of preference share, that gives a fixed return to shareholders in the form of dividend on a preferencial basis. So, company consistently paying dividend will find it easy to use this kind of financing opportunity because investors tend to get more attracted to such organizations which has good financial condition.

These type of convertible preferred stock list have the following characteristics as mentioned below:

- Interest rates affect the pricing of Preference shares. Higher rates make them unattractive, whereas low interest makes them attractive.

- Like bonds, most convertible shares are rated by large organizations such as S&P, Moody, and Fitch.

- Investors must consider whether a higher yield will compensate them with higher risks like equity security when exercising the convertible option.

Most important part of the working of convertible preference stocks is that it give sthe opportunity to its investors to convert their preference holdings into common stocks and a particular ratio and price. Sometimes the convertion may happen at the discreson of the shareholers, where they choose when they want to convert their stocks. However, the business can also force them to do so as and when they need to be done.

It is to be noted that in case of valuation of convertible preferred stock, investors will only be interested in such conversion, provided the price of common stock has exceeded the price of the preference shares, because only then it will be profitable for them.

Example

Let us understand the concept of accounting for convertible preferred stock through an example.

An investor bought 100 shares of convertible preferred stock in ABC Company @ 500 per share on June 1, 2007. So, the initial investment made by an investor is $50000 (100 shares * $500). It offers a fixed dividend yield of 5%, i.e. $25 per share along with a special conversion right wherein 1 share of preferred stock can be converted into 50 shares of common stock (known as conversion ratio), i.e., if an investor opts for conversion, he will be entitled to 5000 common shares (100 preferred stock * 50 common shares). This right can only be applied after June 1, 2008 (the conversion date).

Applying the below formulae can give the total cost per common share after conversion is applied:

Par Value of Convertible Preferred Stock/No. of Common Stock Entitled as a Part of the Conversion.

In this case, it’s $10 (500/50) which is termed as the conversion price.

Case #1

Now let’s assume on June 1, 2008, the stock price was trading at @7 per share in the market. If the investor decides to convert his holding into common stock, the total value of his investment will be $35000 (5000 common shares * $7) on that day. It will fetch him a total loss of $15000 after considering his initial investment of $50000.

Case #2

Now let’s assume that the stock price increased to $30. He would exercise his conversion right as he can get the same stock at ten compared to the market price of $30. The difference between $30 and $10 is called the conversion premium. Post conversion, the total value of his investment will increase to $150000 from $50000, giving him a net realizable gain of $100000.

Advantages

The financial instrument has both advantages and disadvantages. Let us look at the advantages as given below.

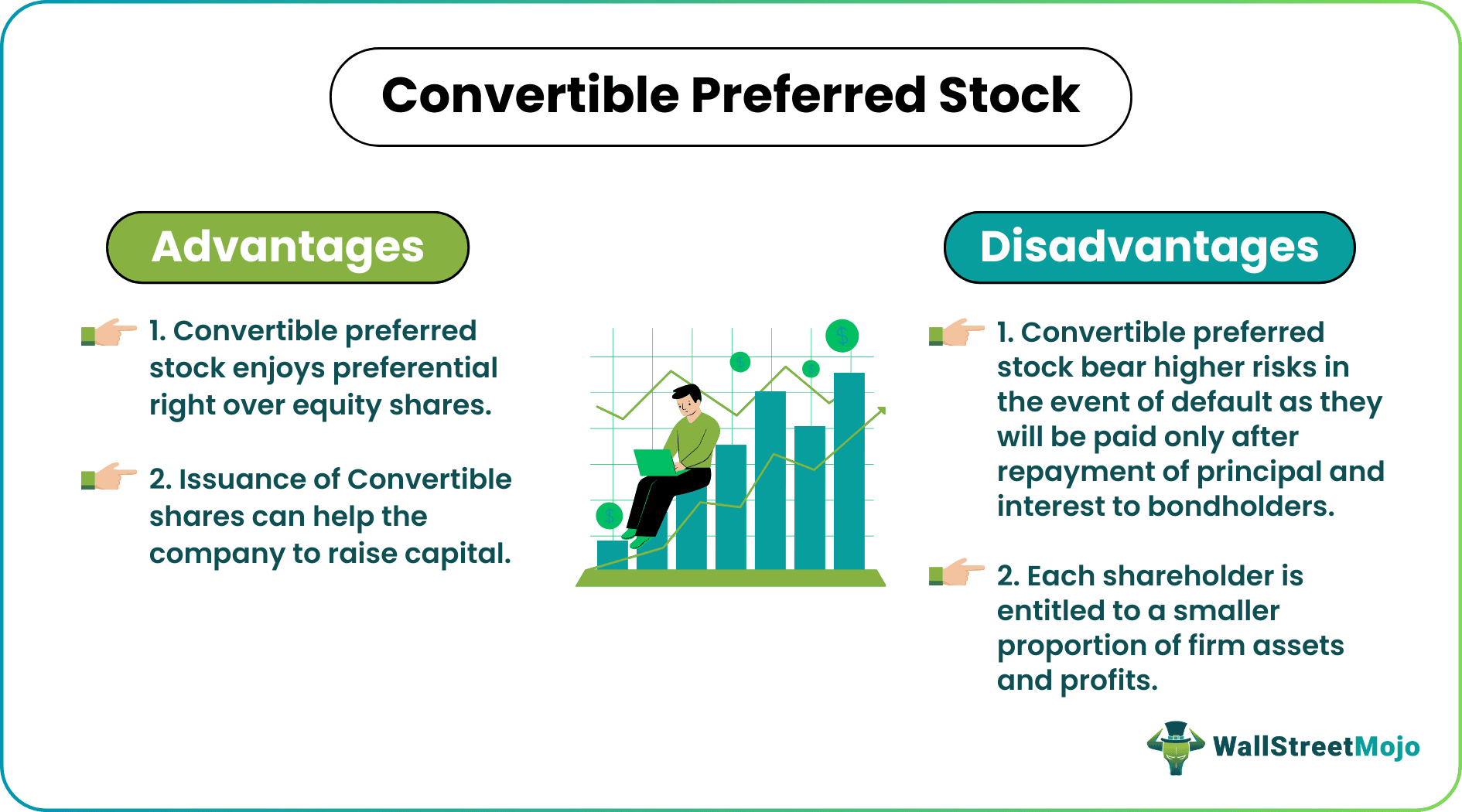

- Convertible preferred stock enjoys preferential right over equity shares regarding the dividend payment and capital repayment in case of winding up.

- If the stock prices appreciate, investors can choose to convert their preferred stock to common stock. They can realize again in the form of capital appreciation from company success while still protected from failure. On the other hand, if the company’s poor performance, it can choose not to exercise the conversion right and keep its convertible stock.

- In the event of bankruptcy, if the conversion feature is not exercised, they are given priority in dividend payment and asset distribution of remaining assets before equity shareholders.

- Before conversion, the issuance of preference shares do not lead to dilution of control, i.e., they do not carry voting rights nor interfere in company decisions.

- The relatively low dividend yield on convertible stock may provide convenience to rapidly growing firms facing heavy capital expenditures. Corporates may be willing to provide a conversion option to reduce immediate cash requirements for dividend payments. Without this option, investors might demand an extremely high dividend to compensate for the probability of default, further increasing the risk of financial distress.

- Issuance and accounting for convertible preferred stock or Convertible sharescan help the company to raise capital on better terms and conditions as compared to traditional equity and bond financing, especially if the company has a poor credit rating and borrowing from the market will involve a huge cost in the form of high-interest rates or if company stock is already trading at a lower value.

Disadvantages

The disadvantages are as follows.

- The dividend yield on Preferred stock is much lower than other classes of preferred stock due to additional features provided, which is conversion right.

- Convertible preferred stock bear higher risks in the event of default as they will be paid only after repayment of principal and interest to bondholders, i.e., they will be par to other equity shareholders.

- When the conversion feature is exercised, the preference shareholder will be treated as another equity shareholder who enjoys no priority in either dividend or asset distribution.

- The exercise and valuation of convertible preferred stock ofrconvertible options increases the number of outstanding shares and creates dilution of control from the perspective of equity shareholders. Therefore, each shareholder is entitled to a smaller proportion of firm assets and profits. This problem never arises with traded options. If an investor buys an exchange-traded option and subsequently exercises it, there is no effect on the number of shares outstanding.

Thus, it is necessary to have a clear idea about the pros and cons of these type of irredeemable or redeemable convertible preferred stock to that investors can take informed decisions and invest their money in financial securities that best suits their own risk appetite and return expectations.

Convertible Preferred Stock Vs Common Stock

Both the above are two different types of financial instruments which have many characteristics in common but at the same time there are some important points of differences between them Let us study them in details.

- As the name suggests, the former has a preference over the latter. The former has the right to get the dividend on a preferential basis before the latter. The latter will get dividend only after the former is paid and there are still fund left for further dividend payment.

- From the previous point it can be derived that the former has the right to get fixed payment whereas the latter may or may not get it.

- Another key difference is that the former has the option to convert their preference holdings to common stock as per ther own discretion of as per the policy of the company. This does not apply for the latter because they already exist in the form of common stock.

- The former typically does not get any right to vote or has very limited right to do so, in relation to corporate matters like management decisions, election of directors, etc. The latter has a right to vote on all important matters relate to the company.

- Even in case of liquidation, or bankruptcy of the business, the former has the preferencial right to claim their part from the liquidated assets of the business, whereas the latter can get their claims only after the former has been paid completely.

- The risk in case of the former is lesser than the latter because the former gets a fixed payment as return, which is not applicable in case of the latter.

- But the investors will be ready to convert the preference shares into common stock only when the latter’s price increases. Therefore it can be said that the former is dependent on the latter.

Recommended Articles

This has been a guide to what is Convertible Preferred Stock. We explain it with example, differences with common stock, advantages and disadvantages. You can learn more about it from the following articles –