Part of our Cash Flow Statement guide

What is Cash Flow?

Cash flow refers to the inflow and outflow of cash and cash equivalents. Cash-flow is generated by business operations, investments, and financing. It determines a business’s cash position and cash availability.

Analyzing a company’s cash-flow provides critical information about its financial health, business activities, and reported earnings. Based on the analysis, future cash flows are projected. Consequently, financial analysts plan short-term goals, long-term goals, working capital, and the optimum cash level required for business operations.

- Cash flow is an inward and outward movement of cash and cash equivalents during a specific period.

- The net money-flow is computed as:

Net Cash Flow = Total Cash Inflows – Total Cash Outflows, - A cash flow statement summarizes the transactions for a specified period—cash generating activities and activities requiring cash expenditure.

Cash-Flow Explained

Cash flow indicates if a business has enough money for its operation. Any transaction that a company does in cash or cash equivalent is penned down in a cash-flow statement to track the status of business funds and keep an account of the closing cash balance at the end of the accounting period.

Cash comprises currency, coins, petty cash, checking account balance, savings account balance, money orders, and bank drafts. Cash equivalents refer to securities that can be liquidated within three months. It includes short-term government bonds, marketable securities, treasury bills, commercial papers, money market funds, and other short-term investments.

The net cash-flow can either be positive or negative. A positive cash flow reflects that the company has enough money to meet its future expenses. However, if the money is surplus, then the firm is not utilizing its liquid funds efficiently. On the contrary, a negative cash flow represents a company unable to pay off its liabilities.

Certain payments made by a company do not reflect in the profit and loss account statement, whereas the same is present in the cash flow statement. For Example, if a company has a loan and is paying off the principal amount back to the bank, this transaction is not shown in the Profit and loss statement. But it will be mentioned in the cash flow statement. Sometimes, such companies show profits but do not have funds to pay off loans and obligations. Such situations can be identified using the cash flow statement.

Types

A business entity accrues profits via the following activities:

#1 Cash-Flow from Operations

Operating activities include a company’s regular business operations. Inflows are generated by selling goods or rendering services, including the collection of sundry debtors.

However, money outflows stream through various monetary payments like the purchase of inventory, releasing salaries, taxes, and miscellaneous operating expenses (OpEx). It also includes the purchase and sale of trading securities.

#2 Cash-Flow from Investing

Investing activities refer to the funds contributed or acquired from purchasing or selling securities or investments. In such a case, money outflow results from the purchase of property, plant, equipment (PPE), and other investment instruments.

Money inflow is generated by selling the possessed securities. Such exchanges exclude securities held for dealing and trading activities.

#3 Cash-Flow from Financing

Financing activities primarily include any receipts and payments related to capital. The inflow from financing refers to the raising of capital from equity or long-term debts. It involves cash receipts from issuing common stock, preferred stock, bonds, and various short-term and long-term borrowings. Thus, there are two significant sources of finance—shareholders and creditors.

In contrast, money outflow comprises repayment of borrowings, the redemption of bonds, treasury stock repurchases, and payment of dividends. However, indirect borrowing from accounts payable is classified as cash flow from operating activities and not from financing activities.

Video Explanation Of Cash Flow

Analysis

The analysis helps furnish vital information concerning the company’s business earnings and helps predict future cash flows. Following are some of the crucial ratios that help check major sources and uses of cash:

- Free Cash–Flow (FCF): It is the excess money left after paying capital expenditure. It defines the business efficacy of making money from the capital employed.

- Operating Cash–Flow (OCF): It is money generated by a company’s primary business operation. A higher OCF signifies a good liquidity position of the company.

- Comprehensive Free Money-Flow Coverage: A percentage value is calculated by computing a fraction of FCF and net operating cash flow and multiplying it by 100. A positive percentage is better in this case as well.

- Current Liability Coverage Ratio: This ratio is computed as the fraction of cash-flow from operations and current liabilities. It determines the company’s ability to pay off its current liabilities with the cash flow from operations. Therefore, a ratio below 1:1 is not acceptable.

- Price to Money-Flow Ratio: To determine this ratio, the operating cash flow per share is divided by the stock price. It thus ascertains a company’s worth from the shareholder’s perspective.

- Money-Flow Margin Ratio: It is a ratio of cash flow from operations and sales. It, therefore, equates to sales generated per dollar.

- Cash Flow to Net Income Ratio: It is the ratio of a firm’s net cash-flow and net income. It represents the amount of cash and cash equivalents consumed for providing a certain net income. A ratio of 1:1 is considered ideal.

Cash-Flow Formula

Net cash flow indicates the increase or decrease in the cash and cash equivalents within an accounting period. The formula is as follows:

Or

Example

Let us assume that XYZ Ltd. made the following money-flow statement for the year ending December 31, 2018:

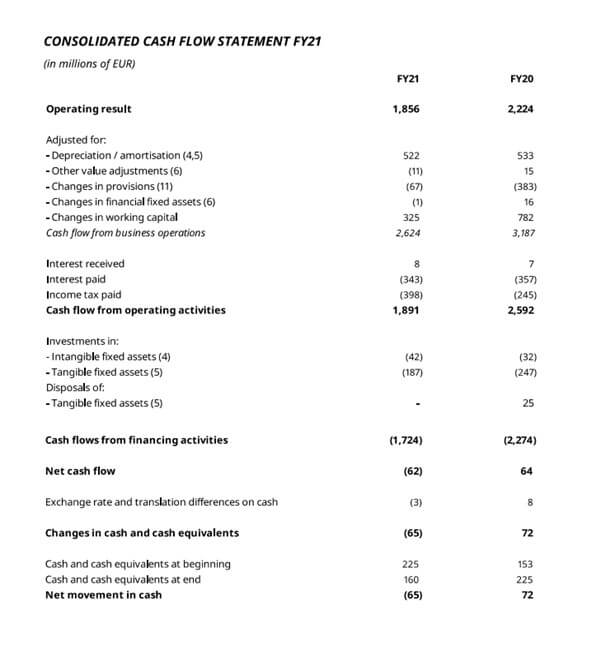

Inter Ikea Group

Furniture giant IKEA’s cash flow for the financial year 2021 ending on August 31, 2021, is as follows:

Profit vs. Cash-Flow

The business’s profit or net income is the money earned by the company during a specific accounting period—as recorded in the book of accounts. It is the value acquired by deducting all the expenses from the revenue. On the contrary, cash-flow is the inward and outward movement of money from the business. It provides the closing cash balance of the firm after deducting all money outflows from money inflows.

Profits give an overview of the business performance in terms of sales; cash flowrepresents the efficiency of handling money. These two metrics don’t need to provide similar results. It can be possible for a company with a positive cash flow position to have low profitability. Similarly, a company with higher profits can generate a negative cash flow.

Moreover, the purposes of these two metrics are significantly different. On the one hand, profits are essential for attaining business goals. Money-flow on the other hand helps smooth operations without capital crunch in the short term—a measure of liquidity.

Frequently Asked Questions (FAQs)

How is cash flow calculated?

The formula used for computing the net cash flow of a company is as follows: Net Money–Flow = Total Cash Inflows – Total Cash Outflows,

or,

Net Money–Flow = CFO + CFI + CFF.

What is the purpose of the cash flow statement?

A cash flow statement mirrors the company’s efficiency in managing its cash and cash equivalents—pertaining to a particular accounting period. It represents the incoming and outgoing money from the business and the net cash balance at the end of the period.

How to manage cash flow?

Following are some of the best cash-flow management practices:

• Prepare a cash flow budget;

• Maintain cash reserves;

• Monitor money outflows;

• Reduce expenses.

• Increase sources of money inflows;

• Keep a check over excess inventory; and

• Streamline the process of cash flow.

Recommended Articles

This article has been a guide to what is cash flow and its meaning. Here we explain cash flows along with its formula, examples, calculations and its differences from Profit. You can learn more about financing from the following articles –