What is the Contribution Margin Income Statement?

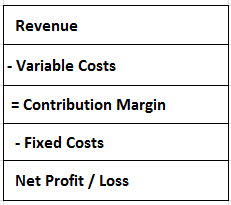

Contribution margin income statements refer to the statement which shows the amount of contribution arrived after deducting all the expenses that are variable from the total revenue amount. Then, further fixed expenses are deducted from the contribution to get the net profit/loss of the business entity.

It is a special income statement format that segregates the variable and fixed expenses involved in running a business. It shows the revenue generated after deducting all variable and fixed expenses separately. In simple words, this format expresses the revenue generated after paying all the variable costs.

Key Takeaways

- The Contribution Margin Income Statement format has fixed expenses as a part of overhead costs instead of production costs. To explain it better, fixed expenses occur even if the sales volumes go up or down. Hence they are independent of what the sales are. However, the variable expenses tend to shoot as the production increases.

- All we need to do is deduct the variable expenses from revenue, which would give a contribution margin as a result. When we deduct all fixed expenses from the contribution margin, it concludes in Net Profit or Net Loss.

- It cannot be used for Generally Accepted Accounting Principles (GAAP) statements and is used by managers internally. This format is handy in decision-making. It helps understand the cost behavior by separating the fixed and variable expenses.

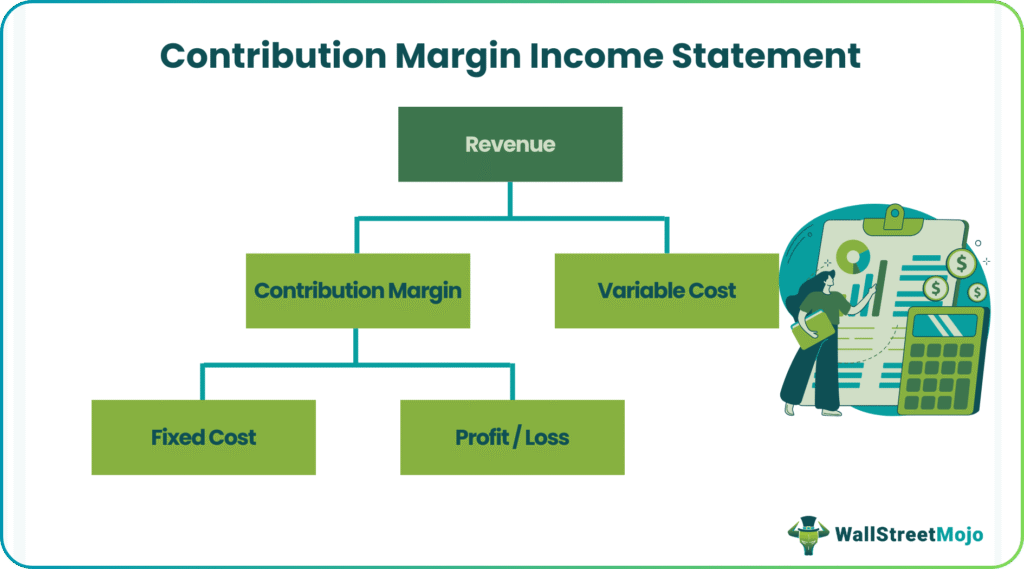

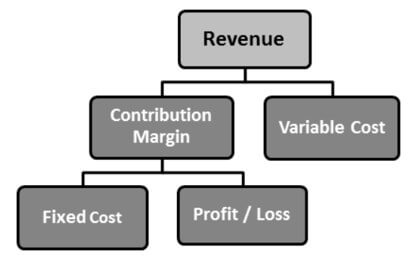

Contribution Margin Income Statement Format:

Every dollar of revenue generated goes into Contribution Margin or Variable Costs. What’s left in the contribution margin covers Fixed Costs and remains in the Net Profit / Loss.

Unlike a traditional income statement, the expenses are bifurcated based on how the cost behaves. Variable cost includes direct material, direct labor, variable overheads, and fixed overheads. It does not matter if your expenses are production or selling and administrative expenses. If they are variable, they must be included in variable costs. The same thing goes with fixed expenses; they must be included in fixed costs if they are fixed.

The contribution margin and the variable cost can be expressed in the revenue percentage. These are called the contribution margin ratio and variable cost ratio, respectively.

Contribution Margin Explanation in Video

Examples of Contribution Margin Income Statement

Example #1

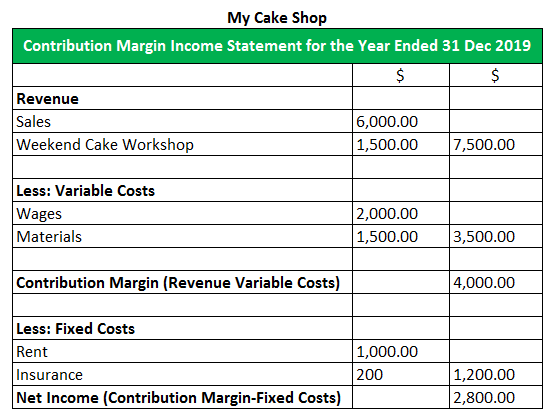

‘My Cake Shop’ is a cake and pastry business that you run. With the rising demand in customers asking for workshops for baking their cakes, you started weekend workshops for the same. The revenue generated for the month was $7,500, which included direct sales of $6,000, and income from conducting Weekend Cake Workshops was $1,500. Wages paid were $2,000, and the expense incurred in procuring materials summed up to $1,500. In addition, rent of $1,000 was paid, and the insurance premium payment of $200 was also made. Therefore, the contribution margin income statement would look like this:

Example #2

Last month, Vienna Inc. sold its product for $2,000 per unit. The fixed production costs were $3,000, and fixed selling and administrative costs were $50,000. Variable production costs were $1,000 per unit, and variable selling and administrative costs were $500 per unit. Vienna Inc. sold 500 units for the previous month.

Prepare a contribution margin income statement.

Calculation:

- Sales = Selling price per unit x No. of units sold =$2,000 x 500 =$1,000,000

- Cost of Goods Sold = $1,000 x No. of units sold =$1,000 x 500 =$500,000

- Selling and administrative costs = $500 x No. of units sold =$500 x 500 =$250,000

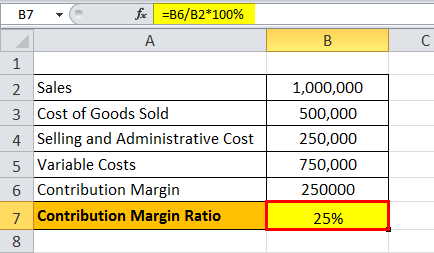

Contribution Margin Ratio

Contribution Margin Ratio = (250,000 / 1,000,000) x 100

Contribution Margin Ratio = 25%

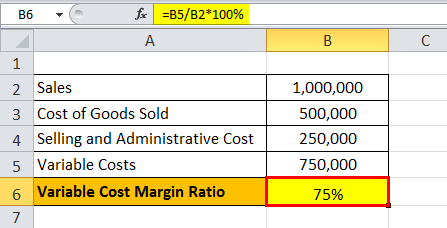

Variable Cost Margin Ratio

Variable Cost Margin Ratio = (750,000 / 1,000,000) x 100

Variable Cost Margin Ratio = 75%

Contribution Margin Income Statement vs. Traditional Income Statement

- It replaces gross margin.

- Fixed expenses are cached lower after the contribution margin.

- Variable expenses are a part of calculating the contribution margin.

Advantages

- Data is organized, which helps the management understand how changes in production and sales volumes will affect the profit.

- It helps identify variable expenses that are eating up too much of the revenue.

- Even though the numbers remain the same, it gives a different perspective of the current financial condition.

- Better analysis can be done as the fixed and variable expenses are bifurcated.

- It can be used for break-even analysis.

Disadvantages / Limitations

- The format is not recognized by GAAP and hence cannot be shared with the external consumers of the financial statements.

- It focuses only on the expenses side.

- The income statement is accessible only to the internal audience.

Important Points

- It depicts expenses based on its functional area.

- It distinguishes between fixed and variable expenses.

- The statement helps in decision-making for the management.

- With the help of the statement, we can conduct a break-even analysis.

Conclusion

The contribution margin income statement is a special format of the income statement that focuses on bifurcated expenses for better understanding. Looking at this statement, it can be easily understood which business activity results in a The contribution margin income statement is a special format of the income statement that focuses on expenses that are bifurcated for better understanding. Looking at this statement, it can be easily understood as to which business activity is resulting in a revenue leak.

Recommended Articles

This article has been a guide to what is a Contribution Margin Income Statement. Here we explain its format, examples, and advantages and disadvantages. You may learn more about finance from the following articles –