Part of our Management Reporting & Analysis guide

What is the Variance Analysis?

Variance analysis refers to identifying and examining the difference between the standard numbers expected by the business and the actual numbers achieved. This helps the company analyze favorable or unfavorable outcomes. In simple words, variance analysis budget studies the deviation of the actual outcome against the forecasted behavior in finance.

It is essentially concerned with the difference between actual and planned behavior and how business performance is impacted. Businesses can often improve their results if they first plan their standards for their performance, but sometimes, their actual result doesn’t match their expected standard results. When the actual result comes in, Management can focus on variances from the standards to find areas needing improvement.

Variance Analysis Explained

Variance analysis is a crucial financial management tool used by businesses to assess the difference between planned financial outcomes and actual results. It involves the systematic examination of the variances, or differences, between budgeted or expected figures and the real financial performance. This analysis provides valuable insights into the effectiveness of financial planning and assists in decision-making processes.

At its core, variance analysis involves comparing actual financial outcomes to the predetermined budget or standard. Variances can be categorized as favorable or unfavorable, depending on whether the actual results surpass or fall short of the expected figures. By breaking down these variances into specific components, such as price, quantity, or efficiency, businesses can pinpoint the root causes of deviations from the budget.

Variance analysis statistics is commonly employed across various financial aspects, including revenues, expenses, and operational metrics. For revenue-related variances, businesses may assess changes in sales volume or pricing strategies. On the expense side, analysis might focus on cost overruns, changes in input prices, or shifts in production efficiency.

This analytical approach aids management in understanding the factors influencing financial performance, facilitating timely adjustments to strategic plans. By identifying the drivers of variances, businesses can refine budgeting processes, enhance operational efficiency, and ultimately improve overall financial health. Variances serve as key performance indicators, offering a comprehensive picture of a company’s financial resilience and highlighting areas for potential optimization.

Formula

The formula for variance analysis budget involves calculating the difference between the actual and budgeted or standard figures. For revenue, expense, or operational variances, the formula typically takes the form of:

Variance = Actual Amount – Budgeted/Standard Amount

Types of Variance

Let us understand the types of variance to understand the concept of variance analysis with respect to budgets through the points below.

- Controllable variance can be controlled by taking necessary action.

- Uncontrollable Variance (UV) is beyond the control of the Departmental head.

- If UV is standard and persistent, the standard may require revision

- Knowing the cause of variance analysis is vital to approach corrective measures.

Types of Variance analysis

Now that we understand the types of variances, it is essential to take it a step further and discuss the types of variance analysis statistics through the explanation below. It also includes practical examples to dive deeper into the concept further.

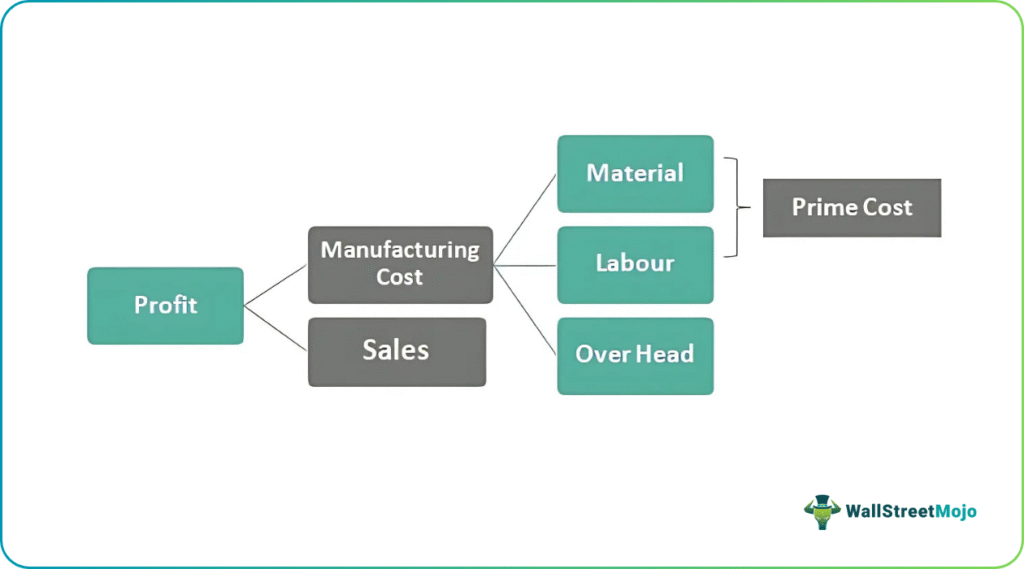

#1 – Material Variance Analysis

- If you pay too much, then the purchasing cost increases

- If you use too many materials, then the production cost increase

Both purchasing and production costs depend on each other, so we have to look into not only the purchasing cost but also the Production Cost to know the total variance.

Example of Material Variance Analysis

Given below is an example of material variance.

Cost Variance

A: (Standard Quantity: 800 Kg)* (Standard Price: Rs.6/-) – (Actual Quantity: 750kg)*(Actual Price: Rs.7/-)

B: (Standard Quantity: 400 Kg)* (Standard Price: Rs.4/-)– (Actual Quantity: 750kg)*(Actual Price: Rs.5/-)

The Impact of the variance of Cost of Material is due to Price and Quantity.

Impact of Price on Material Variance Analysis

The Variation of Price for Type A is (Rs.7/- minus Rs.6/-) for 750 Kg

- Impact of Price on Material A : ( Rs.1/-)*(750Kg) = Rs.750 (A)

The Variation of Price for Type B is (Rs.5/- minus Rs.4/-) for 750 Kg

- Impact of Price on Material B : ( Rs.1/-)*(500Kg) = Rs.500(A)

Total impact of Price = Rs.750 (A) + Rs.500 (A)= Rs.1250 (A)

- *F stands for Favourable

- *A stands for Adverse.

Impact of Quantity on Material Variance analysis

Variation of Quantity Used in Type A material is (800 Kg- 750Kg)*6

- Price due to change in Quantity or Type A is: 300(F)

Variation of Quantity Used in Type B material is (400 Kg- 500Kg)*4

- Price due to change in Quantity or Type A is: 400(A)

Impact of Quantity on Cost Variance is 300(F)-400(A) = 100(A)

Quantity further can be analyzed into two categories, i.e., Yield and Mix. Yield occurs due to the use of inferior material or excess material. In comparison, Mix is due to using a combination of two materials in a different proportion during the production process.

#2 – Labour Variance Analysis

Labour Variance occurs when the actual labor cost differs from the projected labor Cost.

- If you paid too much, that would be personal.

- If you use too many hours which is called efficiency of the Labour that will affects the production.

Example of Labour Variance Analysis

Standard (4 pieces production for 1 Hour)

- Skilled: 2workers@20/

- Semiskilled: 4 workers@ 12/-

- Unskilled: 4 Workers@ 8/-

Actual Output

- Skilled: 2workers@20/

- Semiskilled: 3 workers@ 14/-

- Unskilled: 5 Workers@ 10/-

- 200 Hours Work

- 12 Hours Idle time

- 810 Pieces Production

- Actual Time for Skilled Worker: 200*2(No .of Employee) = 400 Hours

- Actual Time Work for Skilled Worker: (200 Hrs- 12(Idle Time)*2(No of Employee) = 376 Hours

Standard Time for Skilled Worker

- To produce 4 Pieces (Standard time) a skilled worker needed 2 Hours so to produce 810 pieces standard time required

- 4/2 *(810)= 405 Hours

Direct Labour Cost Variance

- (Standard time* Standard Rate)- (Actual Time*Actual Rate)

Direct Labour Rate Variance Analysis

- (Standard Rate- Actual Rate)*Actual Time

Hence, the Direct Labour Efficiency Variance

- Standard Rate*(Standard Time – Actual Time)

Reasons for Labour Variance

- Time-Related Issues.

- Change in design and quality standards.

- Low Motivation.

- Poor working conditions.

- Improper scheduling/placement of labor;

- Inadequate Training.

- Rate-Related Issues.

- Increments / high labor wages.

- Overtime.

- Labour shortage leads to higher rates.

- Union agreement.

#3 – Variable Overheads (OH) Variance Analysis

Variable overheads include costs such as

- Patents that have to be paid on units produced

- Power Cost per unit produced

The total overhead variance is the difference between

- The actual Variable Overhead incurred for the actual output of the business

- The standard variable overhead we should have incurred for the actual output

- Variable OH Variance=(SH*SR)-(AH*AR)

Example of Variable Overheads Variance

Reasons for Overheads Variance

- Under or over absorption of fixed overheads;

- Fall in demand/ improper planning.

- Breakdowns /Power Failure.

- Labour issues.

- Inflation.

- Lack of planning.

- Lack of cost control

#4 – Sales Variance Analysis

- Sales Value Variance = Budgeted Sales – Actual Sales

Further Sales Variance is due to either change in sales price or a Change in Sales Volume.

- Sales Price Variance = Actual Quantity (Actual Price – Budgeted Price)

- Sales Volume Variance = Budgeted Price (Actual Quantity – Budgeted Quantity)

Reasons for Sales Variance

- Change in Price.

- Change in Market Size.

- Inflation

- Change in Market Share

- Change in Customer Behaviour

Thus, Variance analysis helps minimize the Risk by comparing the actual performance to Standards.

Importance

Let us understand the importance of variance analysis budget through the points below.

- Variance analysis serves as a critical tool for evaluating the performance of a business by comparing actual results with budgeted or standard expectations.

- It helps identify and quantify the deviations between planned and actual financial outcomes, offering a clear picture of where the business succeeded or fell short.

- By breaking down variances into specific components (such as price, quantity, or efficiency), businesses can pinpoint the root causes of discrepancies, facilitating targeted improvements.

- Understanding the reasons behind variances enables management to make informed decisions, adjust strategies, and implement corrective actions to enhance future financial performance.

- Variances highlight areas where operational processes can be optimized, leading to increased efficiency and cost-effectiveness.

- Continuous variance analysis allows for the refinement of budgeting processes, ensuring that future financial plans are more accurate and reflective of actual operating conditions.

Advantages and Disadvantages

Almost all concepts and phenomena have factors from both sides of the coin. Let us discuss both of them through the advantages and disadvantages of variance analysis statistics below.

Advantages

- Variances provide a quantitative measure for evaluating the performance of a business, helping assess how well actual outcomes align with planned expectations.

- It enables informed decision-making by identifying areas of strength and weakness, allowing management to allocate resources effectively and adjust strategies.

- Variances, particularly in expenses, allow businesses to control costs by highlighting areas where actual spending deviates from budgeted amounts, facilitating timely corrective actions.

- By analyzing variances related to production and efficiency, businesses can optimize operational processes, reduce waste, and enhance overall efficiency.

- Variance analysis supports a culture of continuous improvement by encouraging businesses to learn from past discrepancies and refine future planning and decision-making.

Disadvantages

- Variance analysis is subject to interpretation, and different analysts may have varying opinions on the significance and causes of variances.

- The process of collecting and analyzing data for variance analysis can be time-consuming, particularly in large organizations with complex operations.

- Focusing solely on financial variances may lead to a narrow perspective, overlooking non-financial factors that contribute to overall business performance.

- Variances may be influenced by external factors beyond a company’s control, such as economic conditions or unforeseen market changes, making it challenging to attribute all variances to internal factors.

- Strict adherence to budgeted figures may lead to rigidity, hindering adaptability in dynamic business environments where flexibility is essential.

Recommended Articles

This has been a guide to what is the Variance analysis. Here we explain the types of variance analysis, examples, importance, advantages, and disadvantages. You may also take a look at the following articles:-