What Are Income Statement Examples?

The income statement examples summarize all the revenues and expenses over the period to ascertain the company’s profit or loss. The example includes an income statement prepared by a company, XYZ Ltd. Every half-yearly to present the company’s different revenues and expenses during the period of half-year to present a financial picture of the company.

An income statement (also known as a profit and loss account) is one of the financial statement that shows the income and expenses of a company for a specified time. Investors and business managers use the income statement to determine the company’s financial health.

Income Statement Examples Explained

The income statement examples feature one of the three fundamental financial statements that aim at calculating net income from the organization’s operations. Generally Accepted Accounting Principle (GAAP) and International Financial Reporting Standards (IFRS) are the two major financial reporting methods based on which credentials, like balance sheet and income statement examples, are prepared. In addition, the income statement states the financial health of the organization.

Major parameters included in and showcased in the comprehensive income statement examples are :

- Revenue: The revenue of the company is the income from all sources.

- Expenses: Costs incurred by a company like the cost of goods sold, and operating expenses come under this.

- Gains/Losses: These are non-operating investment-related activities.

Video Explanation of Income Statement

Examples – GAAP

GAAP classifies the statement as single-step and multi-step, and hence both single-step and multi-step income statement examples are listed below:

Example #1 – Single-Step Income Statement

In this, the classification of all expenses is mentioned under this head. Then they are deducted from the total income to get net income before tax. Both small and large companies use such a format.

There is no implication that one type of revenue or expense item has priority over another. All are treated equally.

- Revenues: All income and revenues are totaled.

- Expenses: All expenses are totaled.

- Net Income: Net income is derived from subtracting Expenses from Income. It is also referred to as “the bottom line.”

Assuming 200000 outstanding shares;

Explanation

Suppose ABC is a USA-based company. In the above example, the single-step income statement is followed where all the incomes from various sources are totaled, and all the expenses to different requirements are totaled. Net income is derived from the difference between the two. None of the entities is given priority. All are treated equally.

Example #2 – Multi-Step Income Statement

The multi-step income statement format comprises a gross profit section where the cost of sales is deducted from sales, followed by income and expenses to reach an income before tax.

Compared to a single-step income statement, multi-step income statement examples are more complex.

It also provides a more detailed overview of the company’s financial position.

The sections of a multi-step income statement include:

- Sales: This section includes total sales, the cost of goods sold, and the difference between the two, gross profit.

- Operating Expenses: These are the expenses that are directly related to the Operations of the company, like selling, general, and administrative expenses.

- Operating Income: It is the income earned from operating activities. It is derived from the difference between gross profit and total operating expenses.

- Non-Operating Income or Expenses: Non-operating activities like investments involve expenses, revenue, gain, or loss. Such an entity comes under this category.

- Net Income: Any resulting profit or loss calculated as the difference between total income and total expenses is called net income.

Assuming the number of outstanding shares to be six lakhs;

Explanation

Suppose XYZ is a US-based company, and a multiple-step income statement is followed here. We can see that all entities are assembled in different categories based on their characteristics.

- Gross profit is derived by subtracting COGS from Sales.

- Selling and administration are operating expenses and are shown separately.

The difference between gross profit and operating expenses give operating income.

The same follows for non-operating expenses and income.

Examples – IFRS

Most companies follow IFRS the world for financial reporting.

The IFRS requires the following items in the income statement :

- revenue

- finance cost

- The share of post-tax results of associates and joint ventures

- after-tax gain or loss.

- profit or loss for the period

Under IFRS, a company that shows operating results should include all the items of irregular or unusual nature.

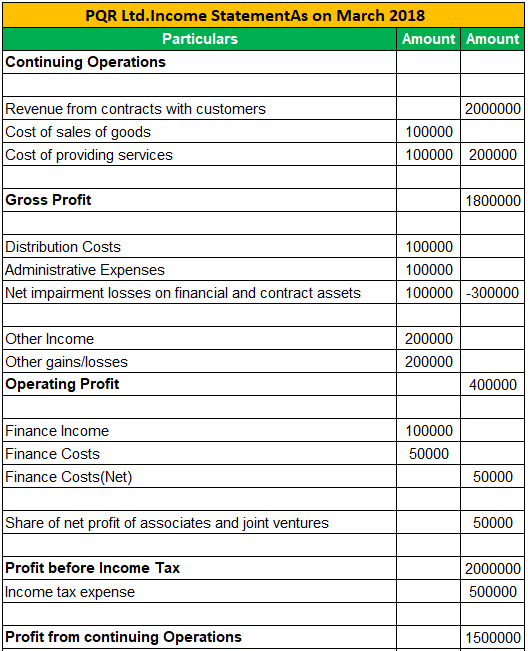

Example #1

Explanation

Suppose PQR is a UK-based company that follows IFRS for reporting. Then, in the above example, we can see that apart from normal entities, all the activities that are unusual and continuous are also taken into count.

Profit from joint ventures and associates is also considered.

So, IFRS is a more comprehensive and informative type of reporting income statement.

Example #2

Explanation

Suppose STU is a US-based company that follows IFRS for reporting. It is seen that apart from normal entities, other unusual and continuous activities are also taken into account. Expenses and transaction details from joint ventures and associates are also considered. Thus, this type of reporting gives a more comprehensive look at the income generated for a given period.

Recommended Articles

This article is a guide to what are Income Statement Examples. We explain examples using two methods – GAAP’s Single Step & Multi-Step Income Statement & IFRS. You may learn more about accounting from the following articles –