Cost Management Meaning

Cost management is the process of managing and controlling monetary resources while running a business. When effective strategies are implemented to manage expenses, it assures a business of having efficient cost control measures, helping them to have an appropriate budget to handle different business activities.

Cost management measures can be implemented either project-wise or for the overall company. The costs remaining well-managed help organizations keep their expenses in control and profits maximized to the best possible extent. In addition, when costs are monitored at every step, resource planning and allocation are more accurate.

- Cost management refers to the management and control of the business costs to ensure businesses spend less and earn more to reap more profits.

- The objective of the management process is not to reduce the costs but to reduce the cost only up to the stage where the quality of the product is not hampered.

- Planning, communication, motivation, appraisal, and decision-making are the features that make managing costs an important business procedure.

- Resource allocation, cost estimation, cost budgeting, and cost control are the major functions of the cost management process.

Understanding Cost Management

Cost management deals with managing costs associated with business activities. For example, from manufacturing goods to delivering them to consumers, businesses must spend on raw materials and shipment measures. All these costs add to organizations’ expenses to generate revenues through the sale of finished goods.

In an attempt to reduce the organization’s costs, businesses compromise the quality of materials used to produce the items. However, they must be aware that compromising on the quality of products will only incur a loss for organizations, be it in the form of reduced sales or hampered reputation.

Thus, cost management is a crucial effort, which should, in no way, affect the product’s quality. Professionals should opt for cost control and reduction while maintaining the quality of goods and services. Various factors affect the process, including:

- Growth in information technology

- Rising domestic and global competition

- Growth of service and manufacturing sectors

- Growth of the service sector

- Customer focus

- Research and development

The cost managing executives plan and set targets to ensure proper cost control. Then, they communicate the same to the higher authorities or the relevant divisions of the companies for implementation. Finally, businesses evaluate the plan for performance. Based on the performance, they make further decisions. These decisions include corrective measures to improve the plan’s performance and target setting.

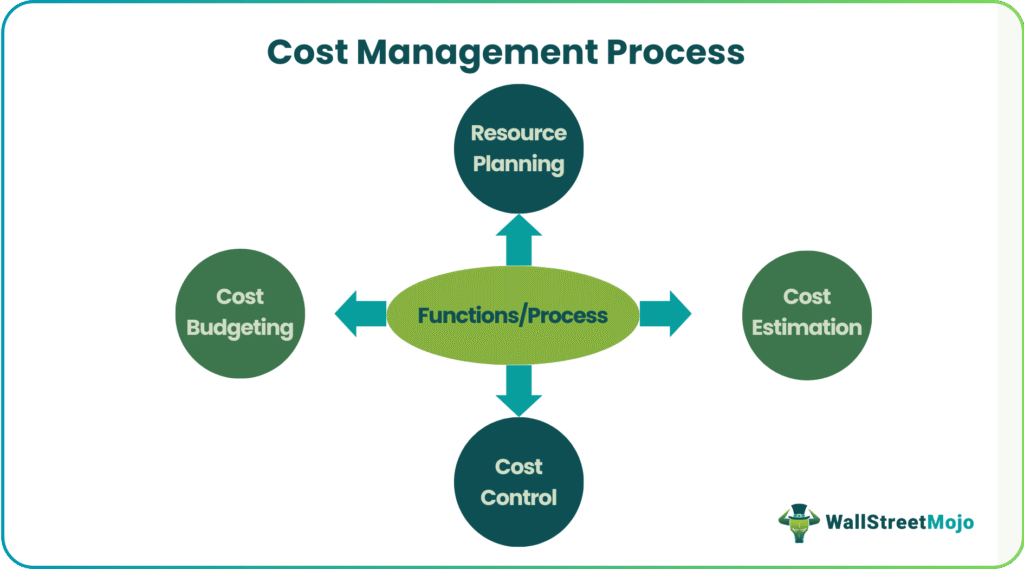

Process

Whether it is project cost management or managing the costs of the overall organization, there are processes or functions that ensure the achievement of the same. They are classified into four categories.

The first step is resource allocation. The process involves identifying resources and allocating and scheduling them. Next, the professionals list the resources required at every stage of project or product development. Besides that, they also take care of the costs associated with buying and providing those resources.

The next one is the cost estimation. It includes the prediction of quantity, cost, and the price of the resources for the project. It involves various techniques wherein companies convert the non-financial information about the project into financial information. Such outputs primarily become inputs for planning and analyzing the overall project cost.

Next is the cost budgeting, which is a part and parcel of cost estimation. In the process, the funding requirements of a project are identified, and the overall cost allocation is done to the cost accounts. Then, the cost accounts become a basis for cost control for comparison at a later stage. The budgeting includes everything from materials and labor costs to administrative and software costs.

Last but not least is the cost control, which involves cost accounts comparison and valuation. The businesses analyze the difference between the estimated cost and actual cost in this step. The variances help grab the least possible cost without hampering the quality of the organization’s end product. The companies monitor expenditures and performances in comparison with the project’s progress, and take corrective measures accordingly.

Strategies

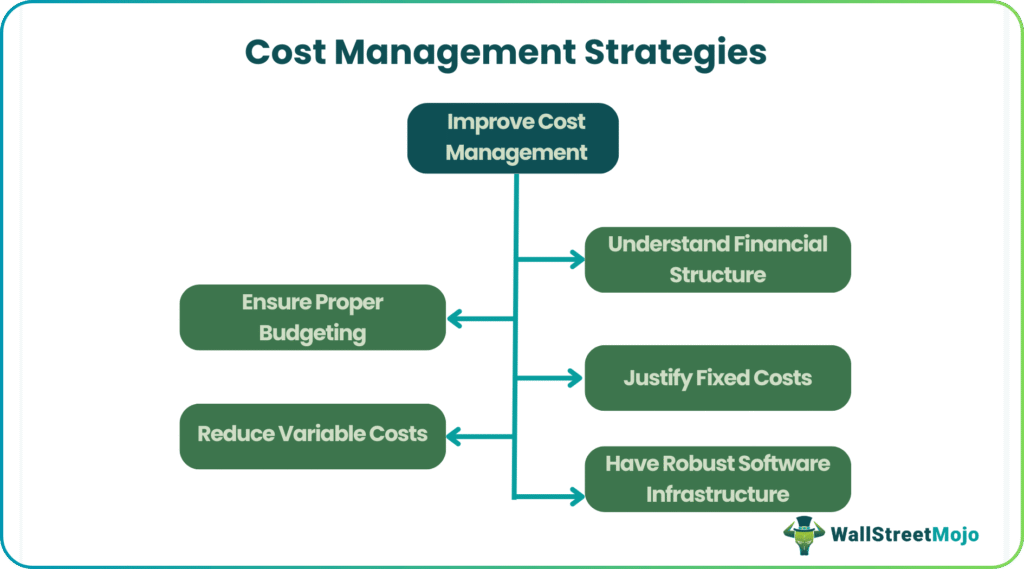

A strategic cost management approach fits when it comes to making the process of managing costs effective to the best possible extent. Considering the below-mentioned points helps improve cost control and management.

The first is to understand the financial structure. This deals with identifying how an organization spends its monetary and non-monetary resources. A company’s equity and debt define its capital structure, which must be studied. In the process, professionals assess the value of a business and the risks it is prone to, making cost management in accordance with that easier. As a result, preparing a proper budget with the help of the available financial information is possible. However, it is important for the companies to proceed according to the budget for effective cost control.

Costs are present in two forms – fixed and variable. Fixed costs, as the name implies, are the costs that remain unchangeable over a period. This includes the wages and salaries, the rents, the lease payments, etc. It is recommended that organizations rethink these costs. For example, paying more and terminating the employment contract, leaving someone jobless is of no use. It is, therefore, better to have a lenient compensation structure with reduced wages and salaries but incentives and rewards for people putting more effort into bringing business or executing sales.

As far as variable costs are concerned, these vary from time to time. However, the companies must ensure no cost reduction at the cost of quality compromise. Some vendors offer discounts on the materials used for production. The firms can look for such vendors to save on their expenses without quality compromise.

Above all, having a software infrastructure makes managing costs and expenses easy and error-free.

Example

Suppose a company wants to launch a new product named DD (franchisee). The company has to pay a royalty of 15% on the selling price to the franchise owner. The expected selling price is $100 per item, and the profit percentage is 25% of the selling price.

The cost details are as follows:

The company, therefore, calculates the target cost and the possible cost reduction.

Solution

- Calculate Target Cost

- Calculate Actual Cost Structure

- = 63-60

- = 3

Thus, per the target cost management technique, the company can reduce the cost by only reducing the manufacturing costs by $3.

Cost Management vs Financial Accounting

Let us quickly look at the differences between cost management and financial accounting.

| Category | Cost Management | Financial Accounting |

|---|---|---|

| Meant for | Finance professionals, business managers | Accountants |

| Considerations | Actual transactions and find their difference with the estimated costs | Actual transactions only |

| Target users/readers | Internal management | External people, including investors, creditors, regulatory agencies, etc. |

| Profit period | As per a particular project, product, or job | On a particular period for the entire organization as a whole |

| Regulation | The requirement is based on the specific situation or decision | Compliance is required |

| Costs measured | For a particular process, project, product, or job | For overall organization at once. |

Frequently Asked Questions (FAQs)

What is project cost management?

It is an integral part of business management that works based on estimations, wherein professionals carry out various activities so that the decision-makers can plan and control the organization’s budget requirements. Such activities include collecting, analyzing the data and mechanisms, evaluating the process, and reporting the events. This enables decision-makers to decide whether the project can be completed within the specified time and budget.

What is required to use azure cost management?

Azure is the software platform that makes automated management of costs easy and error-free. Users must accept the terms and conditions of the Microsoft Customer Agreement to enjoy the features of cost control and management in the Azure portal. The customers also agree to the Azure Plan first to experience how everything works on the platform.

What is cost management accounting?

Cost accounting is the process that offers the management a crystal clear view of the company’s financial structure, thereby listing all the expenses, equity, and debt. When the top officials understand how the finances are being used, it becomes easier for them to plan future cost reduction and cost control.

Recommended Articles

This is a guide to what is Cost Management. Here, we explain its role in project management and accounting along with its strategies and examples. You can learn more from the following articles –