Part of our Types of Shares guide

What Is A Phantom Stock?

Phantom stock is incentive compensation or an employee benefit where the employee receives the benefit of owning a stock without the company giving them the stock. It is an amount that the employer promises to pay its employees shortly.

They are a type of financial instrument known as shadow stocks. They increase the shareholders’ ownership without the actual transfer of the same. It is a type of compensation plan for the employees of the organization. Therefore, in a way these shares provide the employees with a part of the financial success of the company.

- Phantom stock refers to an incentivizing mechanism or employee bonus wherein employees gain ownership benefits without the company issuing them shares. It represents a financial sum that the organization commits to providing its employees in the near future.

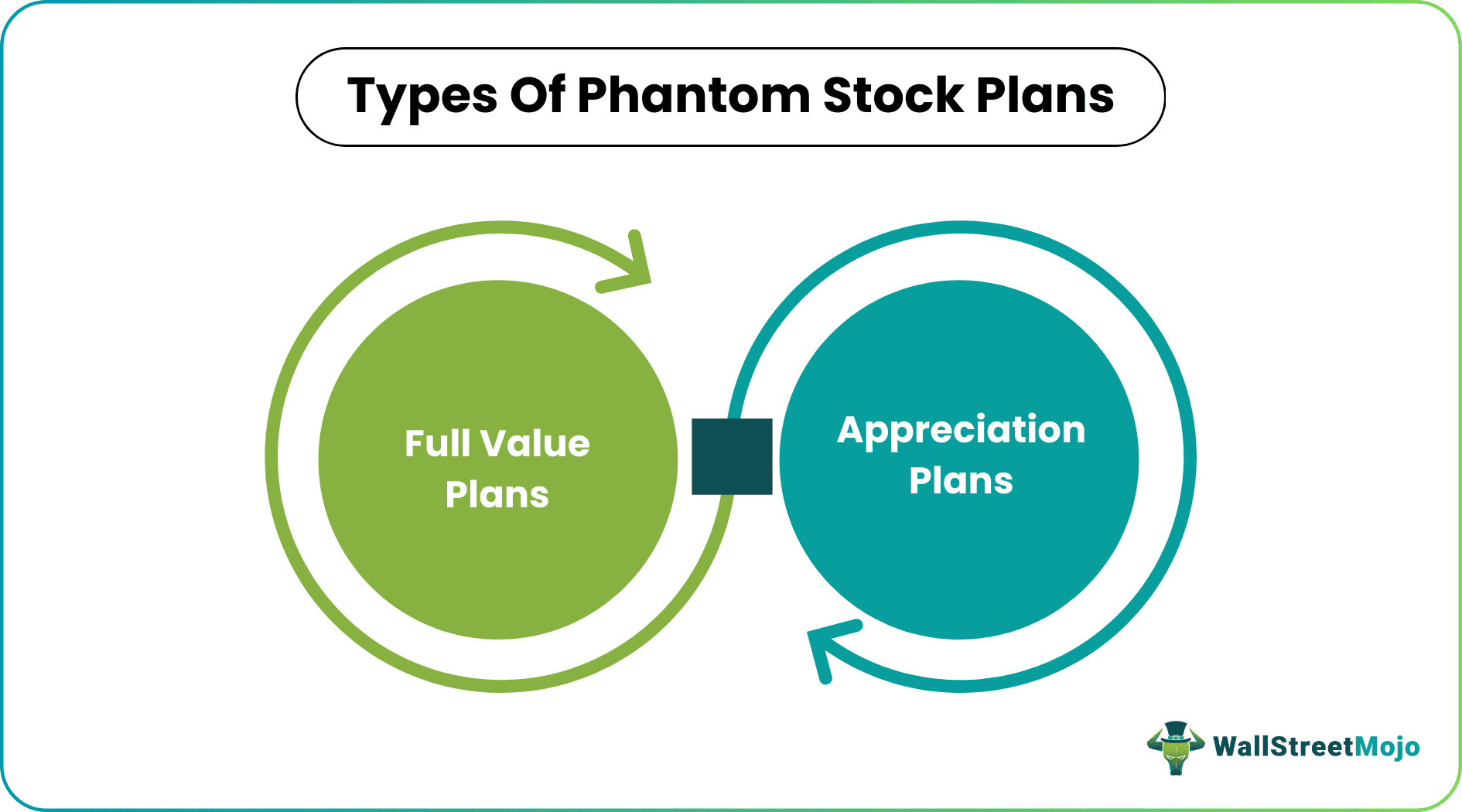

- There are two main types of phantom stock: appreciation plans and full-value plans.

- Phantom stock can serve as a valuable cash incentive program for employees, offering a way for companies to motivate their workforce.

- One of its significant advantages is that, even if the company’s stock price does not experience an increase, participants do not incur any financial losses through this arrangement.

Phantom Stock Explained

Phantom stock plan can be a good employee motivation tool for the company and a solid cash incentive plan for employees. Even if an event goes otherwise and the stock price doesn’t appreciate, neither employer nor employee loses any money directly in the deal.

It provides more upside than downside for phantom stock plans, an increasingly valuable financial tool at a time when employee retention is vital and when the stock market is on a general upward trend.

The near future can be treated as a certain number of years or retirement of an employee, an employee attaining a certain age, or changing the company’s ownership. These stocks are similar to actual stock, where their value rises and falls as compared to that of actual stock of the companies; Companies use phantom stock plan as a motivational tool for retaining its employee or their top-level executive by promising a cash benefit to the employee at some point in the future, where it is subject to a substantial risk of forfeiture.

Types Of Phantom Stocks Plan

#1 – Appreciation Plans

Companies use this particular plan of phantom stock scheme when the employee doesn’t receive the stock’s current value. Instead, they receive the appreciated value of the stock. Therefore, companies can negotiate with the employee for their working tenure in this particular plan.

#2 – Full Value Plans

Full Value phantom stock agreement pay out the exact value of the share, i.e., the exact worth. Whereas an appreciation plan of phantom stock payout the difference between the initial shares and their current value.

Phantom Stocks Accounting

For the purpose of accounting of these phantom stock agreement, they are treated in the same manner as a deferred cash compensation. As and when the liability amount keep changing every year, the accrued amount is entered in the books of accounts. Any fall in the amount will lead to reduction in the liability and vice versa, ue to fluctuations in the company’s stock prices. The adjustment in compensation expense and liability is done accordingly.

It is important to recognize the expense and spread the value of the share over the vesting period. Then the Phanton Stock Compensation Expense Account is debited, and Phantom Stock Liability Account is credited.

When cash settlement has to be done in a phantom stock scheme, the payments are made to employees based on the increase in value. The compensation expense is reported in the company’s financial statement, which include the terms of the plan, fair value calculation and vesting schedule.

Examples

Let us understand the concept with the help of some suitable examples.

Example#1

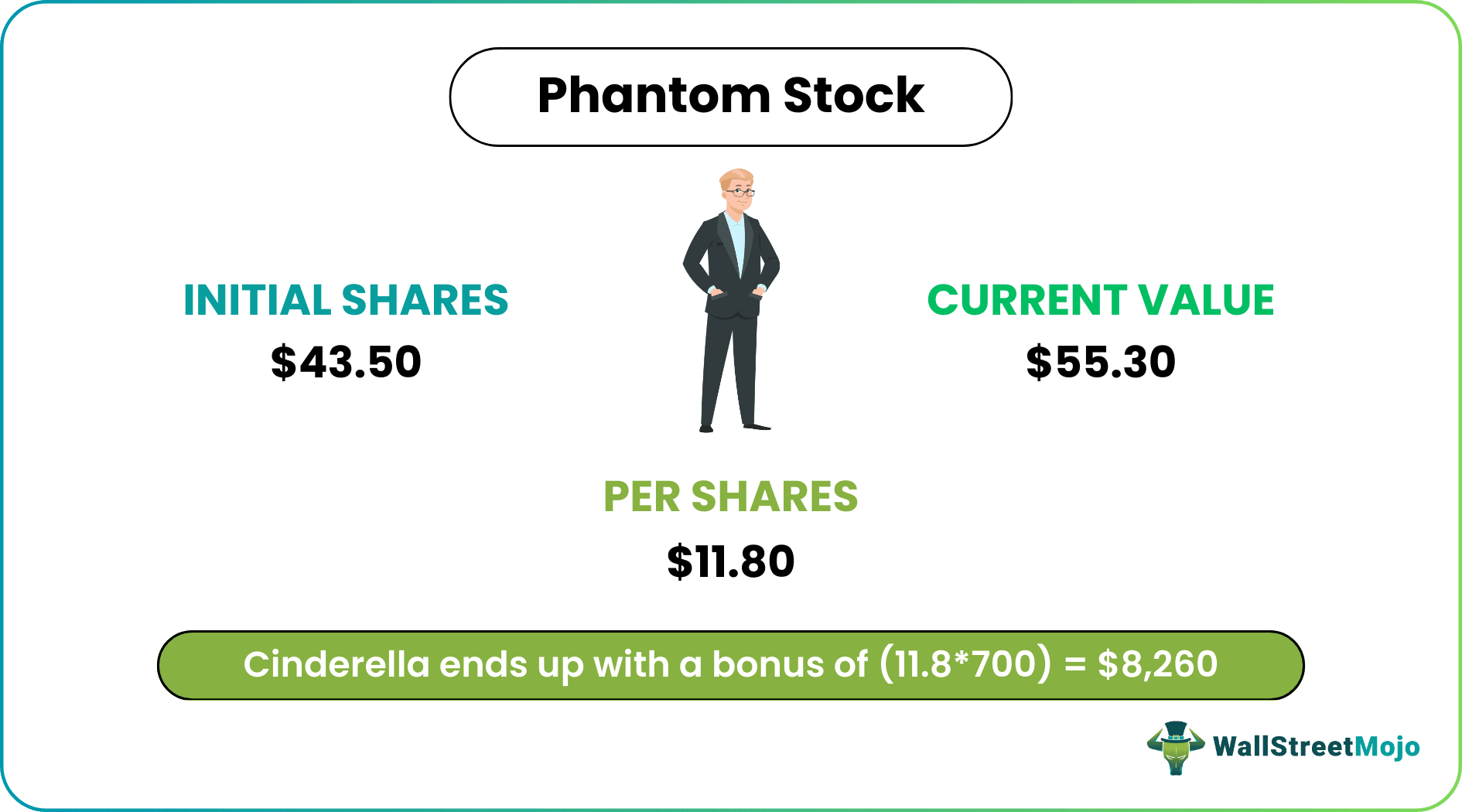

Consider the following Example:

Let’s say Aindrilla was granted 700 shares on May 5, 2013. These shares were worth $43.50 each. Cinderella was asked to stay in the company for the next six years. Thereby she will be able to rip the benefits of these shares. On May 5, 2019, these shares were $55.30 each. For each share of Cinderella, she will get the difference between the current value ($55.30) and the initial share value ($43.50), which is $11.8 per share. Multiply the difference with 700 shares. So Cinderella ends up with a bonus of $8,260.

Example#2

Alex was granted 700 shares on May 5, 2013, from the company where he works. The value of the stock was $43.50 per share. Alex was asked to be with the company for five years. After Alex completed his tenure with the company as the five years passed, the share value rose to $55.30 each. The amount that Alex holds now in full value phantom will be $33,180 as he is paid the full amount.

Advantages

The financial instrument like phantom stock units is very useful for any organization. But it also has its own advantages and disadvantages. Let us point out the advantages first.

- It is a motivational tool and fosters retention as well as there is no investment needed for the employee’s side.

- The ownership of shares for the employer is not diluted.

- It is inexpensive to implement and administer and is structured to meet any number of company needs.

- If necessary, plans may contain a conversion feature that enables employees to receive actual shares of stock instead of cash.

- Companies can control the equity participation of employees through dividends paid out to employees from phantom stock units. Companies can have a “forfeits” agreement towards the stock allotted through the phantom stock plan to the employee if they depart early before the agreement.

Disadvantages

Some important disadvantages of the financial concept are given below.

- During due time employers must have sufficient cash on hand to pay benefits.

- Employers can incur an additional cost if the overview of stock valuation is needed to be completed by an outside company.

- To all true shareholders and the SEC, if the company is publicly traded, employers must report the status of the phantom stock plan at least annually to all participants.

- All benefits are taxed as ordinary income to employees – as the benefit is paid in cash, capital gains treatment is unavailable.

- Participants in “appreciation-only” plans may not receive a thing if the company stock does not appreciate it at a price.

- Participants in “appreciation-only” plans may not receive a thing if the company stock does not appreciate it at a price.

- Companies need to make sure that they comply with Internal Revenue Code Section 409A.

- A phantom stock plan is a costly form of long-term incentive requiring a charge against the company’s income statement.

- It is potentially an “uncapped liability” to the company.

- For executives, phantom stock rights do not represent a true ownership position in privately held companies that do not have publicly traded shares.

- Phantom equity shares do not carry voting rights or similar rights associated with stock ownership.

It is important to understand the pros and cons of any concept in detail so that it the investors, who in this case are the employees of the organization, can understand whether the process is beneficial for them or not and take investment decisions accordingly.

Phantom Stocks Vs Stock Options

Both the above are two different forms of compensation in the form of equity and is used for rewarding the employees. However their differences are as follows:

- The former does not give actual ownership of stocks to the employees but the latter gives the right to purchase the stocks at a predetermined price within a time period.

- Fir the former, if the performance criteria is met, employees get a cash payout equal to the increase in the share value. But for the latter, employees purchase the stocks at the strike price or in case of rise in price, they buy at a discount and sell at higher price.

- The former offer a financial reward without transfer of ownership, whereas for the latter the employees benefit from the stock prices if the company performs well.

- The former is taxed as regular income on salary but in case of the latter, the tax treatment depends when the options are exercised.

Frequently Asked Questions (FAQs)

1. What is the importance of phantom stock?

Phantom stock offers an innovative way to reward and retain key employees without diluting equity. It aligns employee efforts with company growth, enhances retention, and provides a sense of ownership. Phantom stock can bolster company performance and talent retention while minimizing some of the challenges associated with traditional equity plans.

2. Is phantom stock taxable?

Yes, phantom stock is typically taxable for employees. When phantom shares vest or are paid out, they’re subject to taxation as ordinary income. Employers often withhold taxes at the time of payout, similar to regular wages, making it important for employees to plan for the tax implications.

3. What happens to phantom stock when a company goes public?

When a company goes public, phantom stock can be affected. Its value may become linked to the publicly traded stock, impacting potential payouts. The company might need to adjust the program’s terms to align with the new public status, ensuring continued motivation for employees.

Recommended Articles

This article has been a guide to what is a Phantom Stock. We explain the differences with stock options, with examples, disadvantages, accounting & types. You can learn more about accounting from the following articles –