Part of our Accounting Concepts guide

Accounting for Convertible Bonds & Debt

→ Explore all 63 Bonds articles

Accounting for Convertibles refers to the accounting of the debt instrument that entitles or provides rights to the holder to convert its holding into a specified number of issuing company’s shares where the difference between the fair value of total securities along with other consideration that is transferred and the fair value of the securities issued is recognized an expense in the statement of income.

Explanation

Convertible Bonds entitle the bondholders to convert their bonds into a fixed number of shares of the issuing company, usually at the time of their maturity. Thus, convertible bonds have features of both equity as well as liability. Convertible notes do not mandate conversion. They give an option to the bondholders at the time of conversion, and it is at their discretion whether they want to convert and get equity shares or opt out and get cash against these bonds. Since the convertible bonds have features of both liability (debt) and equity, it makes more sense to account for the liability and equity portions separately.

It will help to give a true and fair view of the Financial Statements of the organization because of the following two reasons:

- As these bonds are convertible to equity in the future, they offer a lower interest rate. Accounting the equity & debt portion separately will show the true financial cost of the organization.

- It is also important to show that the debt might be converted to equity, and financial statements should demonstrate this.

Video Explanations of Accounting for Convertible Bonds

Accounting for Convertible Bond Video Explanation

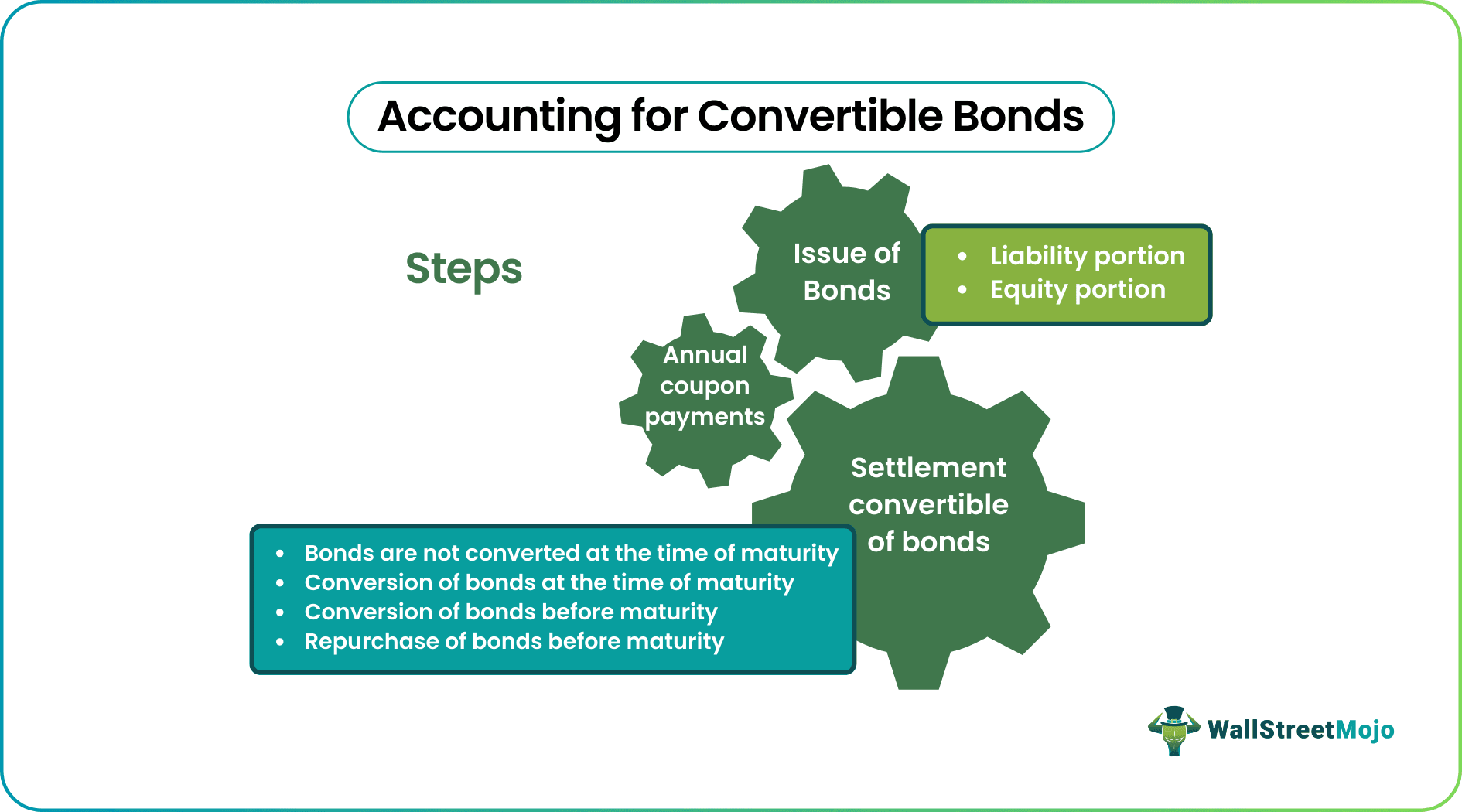

Step by Step Accounting for Convertible Bond (Debt)

An accounting will be split up into three different parts:

- Issue of Bonds

- Annual Coupon Payments

- Settlement of Bonds

Let us go through each one of them in detail to understand the entire flow of accounting for convertible bonds.

If you are new to bonds, do have a look at Bond Pricing

#1 – Issue of Convertible Bonds

The equity & liability portion for the convertible bonds can be calculated using the Residual Approach. This approach assumes that the value of the equity portion is equal to the difference between the total amount received from the proceeds of the bonds and the present value of future cash flows from the bonds. The split between the equity and liability portion needs to be accounted for at the time of the issue of bonds itself.

a) Liability Portion:

The liability portion of the convertible bonds is the present value of the future cash flows, calculated by discounting the future cash flows of the bonds (interest and principal) at the market interest rate with the assumption that no conversion option is available.

Using the above example, the present value will be calculated as follows:

| Year | Date | Type of Cashflow | Cashflow | Present Value Factor Calculation | Present Value Factor | Present Value |

|---|---|---|---|---|---|---|

| 1 | 31-Dec-16 | Coupon | 50,000 | (1/1.15^1) | 0.869565 | 43,478.26 |

| 2 | 31-Dec-17 | Coupon | 50,000 | (1/1.15^2) | 0.756144 | 37,807.18 |

| 3 | 31-Dec-18 | Coupon | 50,000 | (1/1.15^3) | 0.657516 | 32,875.81 |

| 4 | 31-Dec-19 | Coupon | 50,000 | (1/1.15^4) | 0.571753 | 28,587.66 |

| 5 | 31-Dec-20 | Coupon | 50,000 | (1/1.15^5) | 0.497177 | 24,858.84 |

| 5 | 31-Dec-20 | Principal Repayment | 5,00,000 | (1/1.15^5) | 0.497177 | 248,588.40 |

| Present Value | 4,16,196.1 |

(Cash flow per year for Coupon Payments = 500 bonds * $1000 * 10% = $50,000)

b) Equity Portion:

The value of the equity portion will be the difference between the total proceeds received from the bonds and the present value (liability portion).

Calculating the equity portion for the above example:

Total Proceeds = $1000 * 500 bonds = $5,00,000

Present Value of Bond = $4,16,196.12

Equity Portion = Total Proceeds – Present Value of Bond = $5,00,000 – $4,16,196.12 = $83,803.88

So the very first Journal Entry in the books for the issue of Convertible Bonds will be as follows:

| Date | Account | Debit | Credit |

|---|---|---|---|

| 01-Jan-2016 | Bank A/c | 5,00,000 | |

| 10% Convertible Bonds Series I A/c | 4,16,196.12 | ||

| Share Premium – Equity Conversion A/c | 83,803.88 |

(Being 500 convertible bonds issued at 10% coupon rate and maturity 5 years)

Here, 10% Convertible Bonds Series I A/c is the liability account specifically created to represent this particular issue of bonds.

Share Premium – Equity Conversion A/c is the equity portion that will be reported under the Equity Section in the balance sheet.

#2 – Annual Coupon Payments

Every year, coupon payments will be made to the bondholders. As mentioned earlier, convertible bonds are issued at a lower interest rate. For taking the actual financial cost into the picture, interest will be charged to the Profit & Loss Account on the effective rate of interest, which will be higher than the nominal interest. The difference between the effective interest and nominal interest will be added to the value of the liability at the time of interest payment.

The calculation of the same will be as follows:

Effective Interest = Present Value of Liability * Market Rate of Interest.

Actual Interest Payment = Face Value of Bond * No. of Bonds Issued * Coupon Rate.

Value of Liability (end of the year) = Value of Liability at the start of the year + Effective Interest – Actual Interest Payment

| Year | Date | The present value of the liability | Interest Calculation | Effective Interest | Actual Interest Payment | Value of Liability at the end of Year |

|---|---|---|---|---|---|---|

| 1 | 31-Dec-16 | 4,16,196.12 | 4,16,196.12 * 15% | 62,429.42 | 50,000.00 | 4,28,625.54 |

| 2 | 31-Dec-17 | 4,28,625.54 | 4,28,625.54 * 15% | 64,293.83 | 50,000.00 | 4,42,919.37 |

| 3 | 31-Dec-18 | 4,42,919.37 | 4,42,919.37 * 15% | 66,437.91 | 50,000.00 | 4,59,357.28 |

| 4 | 31-Dec-19 | 4,59,357.28 | 4,59,357.28 * 15% | 68,903.59 | 50,000.00 | 4,78,260.87 |

| 5 | 31-Dec-20 | 4,78,260.87 | 4,78,260.87 * 15% | 71,739.13 | 50,000.00 | 5,00,000.00 |

Journal Entry for Interest will be as follows:

| Date | Account | Debit | Credit |

|---|---|---|---|

| 31-Dec-2016 | Interest Expense A/c | 62,429.42 | |

| 10% Convertible Bonds Series I A/c | 12,429.42 | ||

| Bank A/c | 50,000.00 | ||

| (Being coupon payments made for year 1 and interest expense accounted for) | |||

| 31-Dec-2017 | Interest Expense A/c | 64,293.83 | |

| 10% Convertible Bonds Series I A/c | 14,293.83 | ||

| Bank A/c | 50,000.00 | ||

| (Being coupon payments made for year 2 and interest expense accounted for) | |||

| 31-Dec-2018 | Interest Expense A/c | 66,437.91 | |

| 10% Convertible Bonds Series I A/c | 16,437.91 | ||

| Bank A/c | 50,000.00 | ||

| (Being coupon payments made for year 3 and interest expense accounted for) | |||

| 31-Dec-2019 | Interest Expense A/c | 68,903.59 | |

| 10% Convertible Bonds Series I A/c | 18,903.59 | ||

| Bank A/c | 50,000.00 | ||

| (Being coupon payments made for year 4 and interest expense accounted for) | |||

| 31-Dec-2019 | Interest Expense A/c | 71,739.13 | |

| 10% Convertible Bonds Series I A/c | 21,739.13 | ||

| Bank A/c | 50,000.00 | ||

| (Being coupon payments made for year 5 and interest expense accounted for) |

Food for thought: As you must have noticed, the liability value keeps increasing year after year, and at the end of year 5, it is equal to the face value of the bond. The total amount added to the Liability each year will be equal to the Equity Options amount we arrived at at the time of the issue of these Convertible Bonds.

Total Amount added to liability= 12,429.42 + 14,293.83 + 16,437.91 + 18,903.59 + 21,739.13 = 83,808.88

Also, note that the equity section of the Convertible Bonds will not change during the life of the bonds. This will change only at the time of conversion or payout, as the case may be.

#3 – Settlement of Convertible Bonds

There can be four different situations for settlement of bonds depending on conversion / non-conversion and the time on which this takes place, i.e., before or at the time of maturity:

a) Bonds are not converted at the time of maturity

This is also known as the repurchase of bonds. In this case, the bondholders are paid the maturity amount, and only the liability portion accounted for earlier will have to be derecognized. The maturity amount will be paid to the bondholders.

Journal entry for the same will be as follows:

| Date | Account | Debit | Credit |

|---|---|---|---|

| 31-Dec-2020 | 10% Convertible Bonds Series I A/c | 5,00,000.00 | |

| Bank A/c | 5,00,000.00 |

(Being maturity proceeds paid to convertible bondholders at the time of maturity)

Now, the equity portion we had accounted for under Share Premium – Equity Conversion A/c can remain as it is, or the company can transfer it to normal Share Premium A/c if any.

b) Conversion of bonds at the time of maturity

Bondholders may exercise the conversion option; in this case, shares will have to be issued to the bondholders per the conversion ratio. In this case, the equity and liability portion will be derecognized, and equity share capital & reserves will have to be accounted for.

No. of shares issued = 5 shares per bond * 500 bonds = 2500 shares of face value $20 each

Journal entry for the same will be as follows:

| Date | Account | Debit | Credit |

|---|---|---|---|

| 31-Dec-2020 | 10% Convertible Bonds Series I A/c | 5,00,000.00 | |

| Share Premium – Equity Conversion A/c | 83,803.88 | ||

| Equity Share Capital A/c | 5,00,000.00 | ||

| Share Premium A/c | 83,803.88 |

(Being 2500 shares of face value $20 issued against convertible bonds)

c) Conversion of bonds before maturity

Let us say that the conversion takes place on 31st December 2018. The value of liability on this date is $4,59,357.28. Further, the Share Premium – Equity Conversion A/c will need to be reversed.

Journal entry for the same will be as follows:

| Date | Account | Debit | Credit |

|---|---|---|---|

| 31-Dec-2018 | 10% Convertible Bonds Series I A/c | 4,59,357.28 | |

| Share Premium – Equity Conversion A/c | 83,803.88 | ||

| Equity Share Capital A/c | 5,00,000.00 | ||

| Share Premium A/c | 43,161.16 |

(Being 2500 shares of face value Rs. 20 issued against convertible bonds)

Here, Share Premium A/c will be the balancing figure arrived as follows: 4,59,357.28 + 83,803.88 – 5,00,000.00 = 43,161.16

d) Repurchase of bonds before maturity

An organization may decide to repurchase its bonds before maturity. In the given example, let us say that the bonds were repurchased on 31st December 2018.

On this date, different values which need to be considered are as follows:

| Carrying Value of Liability | Calculated earlier (Refer section annual coupon payments) | $4,59,357.28 |

| Market Value of Bonds | Assumed value – Selling Price | $5,25,000.00 |

| Fair Value of Liability | This amount needs to be calculated as the present value of the non-convertible bond with a three-year maturity (which basically corresponds to the shortened time to maturity of the repurchased bonds – Refer next table for calculation) | $4,42,919.37 |

| Gain on repurchase | Fair Value of Liability – Carrying Value of Liability | $16,437.91 |

| Equity Adjustment | Fair Value of equity component | $82,080.63 |

Journal entries for the above will be as follows:

| Date | Account | Debit | Credit |

|---|---|---|---|

| 31-Dec-2018 | 10% Convertible Bonds Series I A/c | 4,59,357.28 | |

| Share Premium – Equity Conversion A/c | 82,080.63 | ||

| Gain on Repurchase of Bonds A/c | 16,437.91 | ||

| Bank A/c | 5,25,000.00 |

(Being 2500 shares of face value $20 issued against convertible bonds)

There will be a balance of $1,723.25 (83,803.88 – $82,080.63) in Share Premium – Equity Conversion A/c. This can remain as it is, or the company can transfer it to normal Share Premium A/c if any.

Recommended Articles

For more on Accounting Concepts, explore these related articles from our Accounting Concepts guide.