Part of our Types of Shares guide

What Is Shares Premium?

Share Premium is the difference between the issue price and the par value of the stock and is also known as securities premium. The shares are said to be issued at a premium when the issue price of the share is greater than its face value or par value. This premium is then credited to the share premium account of the company.

It arises when the company issues its shares for the first time to the public above its face value, not when the investors sell them in the open market. For example, if the company sells its shares, having a face value of $3 per share at the price of $5 per share, then the share premium reserve is $2 per share. Still, if the investors sell the same further $8 per share, then the company’s securities premium of $3 is not gained. Simply it is the gain to the investor.

Share Premium Explained

Share premium is the amount which any company gets after issuing shares to investors and that is over and above the face value of the issued share capital. It is received when the shares are issued for the first time.

The par value is the lowest price at which the shares can be issued to the general public. But premium is the amount of money that the investors are ready to pay willingly pay to the company beyond the nominal value of the issued shares.

No premium is received by the company when shares are further sold in the secondary market. The use of it is restricted to the purpose as specified in the corporate bylaws. It is a part of the company’sretained earnings but cannot be treated as the free reserve. Thus the amount of share premium reserve must be utilized as per the conditions of the law.

The business can use this premium for various purposes, financing day-to-day operations, investing in growth and expansion, or new projects.

However, decision on how the share premium account will be used depends of the rules and by laws followed by the company’s management. It may have some restrictions and regulations which should be followed.

Also, note that the Share Premium account is also known as Additional Paid-in Capital in US GAAP.

Components

Let us not understand the components of share premium account.

#1 – Issue price of Share Capital

The price at which the company offers its shares to the public for sale is called an issued price. The shares can be issued at, above, or below its face value. Therefore, the face value and the issue price of the share don’t need to be the same.

#2 – The Face value of Share Capital

The initial value or the original value of the share decided when the capital was raised is known as the face value of shares. All the benefits given to the shareholders are decided to consider the face value of shares. For example, if the rate of dividend declared by the company is 10%. Then the 10% will be calculated using the face value of shares issued.

Formula

Let us look at the share premium formula that is used to calculate the premium on shares issued.

(Issue price per share – Face value/par value per share) * No of shares

OR

Total amount received on issue of shares – Total par value of shares issued

Using this formula it is possible to calculate the premium on the shares that are issued to the investors.

Example

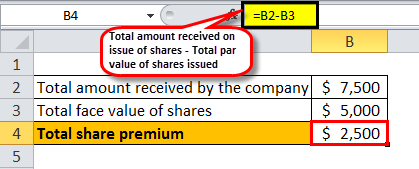

For example, XYZ Company issued 500 shares at $15 per share having a par value of $10 per share.

- Now the total amount received by the company is 500*$15 = $7500

- Total face value of shares = 500*$10 = $5000

Total reserve = $2,500

Another way to calculate the premium using the share premium formula can be:

- The share premium per share = $15 – $10 = $5

- So total share premium is $5*500 = $2500.

The above amount of $2500 will be credited to the securities premium account and reported under the head reserves and surplus of equity and liabilities.

Uses

The share premium account or the share premium capital cannot be distributed as dividends but can be used for the following reasons:

- To issue the bonus shares to the existing shareholders of the company.

- To write off the company’s preliminary expenses or underwriting cost.

- To write off the equity-related expenses like discount allowed or commission paid on the issue of shares.

- To provide for the premium payable at the time of redemption of debentures or preference shares of the company.

- To purchase its shares and other type of securities.

Advantages

Let us go through the advantages of share premium in accounting.

#1 – No Dilution in Rights

Raising funds additionally using a share premium account does not lead to the dilution of the rights of the shareholders as the same number of shares are issued with the additional amount in the form of premium.

#2 – Tax Neutral

The company does not issue shares in exchange for any goods or services, so there will be no profit or gain by this. Also, it is not the income for the company; rather, they are reflected in the equity head of the company’s balance sheet. Thus there will be no tax consequences by raising additional funds in the form of a share premium account for the reason that it does not have any taxable base or tax burden. Also, at the time of distribution of dividends to the shareholders, it is not considered, so they are also not subject to the dividend withholding tax.

#3 – Timing of distribution

These premiums are eligible for the distribution to shareholders at any time. In contrast, the profits are not as profits can be distributed after the approval of financial statements by shareholders in the general assembly.

#4 – Financial consideration

For the company, like reserves, This premium also represents an element of equity. For shareholders of the company, It provides extra value for their participation in the company.

#5 – Reduction in Cost

When the shares are issued at the premium, then the incidental advantage is the reduction in the cost of capital. It does not require any additional administrative work and no additional fees for the authorized capital and registrar of companies as the fees are paid on the authorized share capital amount.

#6 -Higher Dividend Rate

As the dividend is declared on the paid-up share capital and not on the premium account, the rate of dividends to the shareholder will be high.

Disadvantages

There are some disadvantages of share premium in accounting. The securities premium account is considered the restricted account as the amount received as the premium is not a part of free reserves. The amount of share premium account can only be utilized for the purpose as allowed in the corporate bylaws. For example, the company cannot pay dividends from the premium account. This account can be mainly used to offset the share issue expenses and not the operating losses.

Recommended Articles

This article has been a guide to what is Shares Premium. We explain its formula along with examples, uses, components, advantages and disadvantages.. You may learn more about accounting from the following articles –